#10 The Big Long

#10 The Big Long

How the manipulation in the money supply has inextricably affected market valuations during the last decade. That which is seen, and that which is not seen.

Welcome to Edelweiss Capital Research! If you’re new here, join us to receive investment analyses in 10 slides, economic pills and investing frameworks by subscribing below:

By A. Valverde:

Two friends met after many years.

“So what do you do for a living?”

“I am a geologist”

“That means you put loads of time and effort into studying how inside Earth mechanisms work, and yet you can´t even accurately prevent when a volcano is going to erupt?”

“Correct. And what do you do?”

“I am an economist”

In this article we shed some light on how manipulating the money supply inextricably affects market valuations, and why central banks should be (or rather should have been) very careful when applying non-conventional monetary policies. In Bastiat´s words, every policy decision will provoque “That Which is Seen, and That Which is Not Seen”.

Economists cannot anticipate the future. Since they cannot, it is often preferable to remain within mainstream consensus. “It is better for reputation to fail conventionally than to succeed unconventionally”, said Keynes.

Over the past few years, there has been a great deal of publications that tried to explain why there was no inflation, and why non-conventional, expansionary policies, both fiscal and monetary, could, and indeed should, remain in place permanently. This time it was different. Or was it?

Economics is a social science in which answers are not always immediate, since causes are sometimes hard to spot. However, we will try to explain some dynamics that tend to happen in the long term, time and again:

As Nobel laureates Hayek (1974), Friedman (1976) and Lucas (1995) explained: in the long term, structural inflation is always a monetary phenomenon.

There will always be expert alchemists claiming: “this time it is different”.

The balloon analogy

Say you have a balloon. It is a simple, round balloon. You blow air into it. What happens then? It gets inflated, right? Moreover, it gets inflated approximately uniformly. If the balloon surface represents the prices of all things available in an economy, you will see the general level of prices increasing at the same rate as you blow air into the balloon. In fact, you will see how all prices increase at the same rate, meaning there will be no change in the relative prices: apples and bicycles will both be more expensive, but the amount of apples that can be exchanged for one bike in the market will remain the same.

Father Juan de Mariana observed that in regions where piles of precious metals circulated, the general level of prices tended to be higher, while in other regions with a smaller amount of gold and silver circulating, prices were lower (de Mariana, 1609). Centuries later, authors like Fisher, Marshall and Pigou called this the quantitative theory of money:

M * V = P * Y

The money supply (M) multiplied by its velocity of circulation (V) must equal the total amount of goods and services produced in an economy (Y) multiplied by their prices (P). In other words, the total value of purchases equals the total value of sales.

Let us get back to our balloon analogy, and let us assume that the balloon is the economy at a certain moment, where the amount of things produced is given (“Y” in the equation does not change in the short term).

“Money supply” is the air in the balloon, blown into it both by central banks and by the rest of the banking system. “Money velocity” (how many times each monetary unit changes hands) is the temperature of this air: if the air inside the balloon warms up, its molecules move more, and the same amount of air occupies more volume in the balloon. So the balloon inflates either by blowing more molecules into it, or by warming the air already inside. If the balloon inflates, its surface expands: the “price level” of all things increases.

“But this is not happening now. I am looking at consumer prices, and they are not increasing”, said the alchemists in 2015, 2016, 2017, 2018, 2019, 2020…

Why asset prices were increasing while consumer prices remained stable: a different balloon

Let us picture a different type of balloon, one with the shape of an elephant. When you blow up this balloon, some parts of its body surface may not inflate (say the ears), while other parts will expand a lot (the trunk and the legs). Continuing with the analogy, if the surface of the elephant represents all the prices of an economy, the surface of the ears depicts the prices of final consumption goods and services; while the surfaces of trunk and legs represent various asset prices (real estate, financial, capital goods, etc).

The central bank has a price stability mandate (2% yearly average increase in the consumer price index in most developed countries), but in order to fulfil its mandate, it is only looking at the ears of the elephant. For many years now, while money supply was being inflated, the trunk and legs grew exponentially, but the ears barely changed. “Inflation is over”, we were told. Nevertheless, asset prices kept increasing. Real estate and financial markets kept reaching all-time records.

After a long time, even the ears are finally growing, and CPI yearly growth rates are close to 10% in many developed countries. What will happen if/when central banks eventually react in order to deflate the ears? Remember, that is all they focus on. What will happen with the trunk and the legs? What if one of them has become so inflated that it actually “bursts”?

Money is fiat, and it is printed out of nothing. Not even printed, since most of it consists of accounting entries on the balance sheets of those responsible for creating money. The money supply can be expanded (or reduced) by central banks, but also by commercial banks, and even by some other agents in the economy.

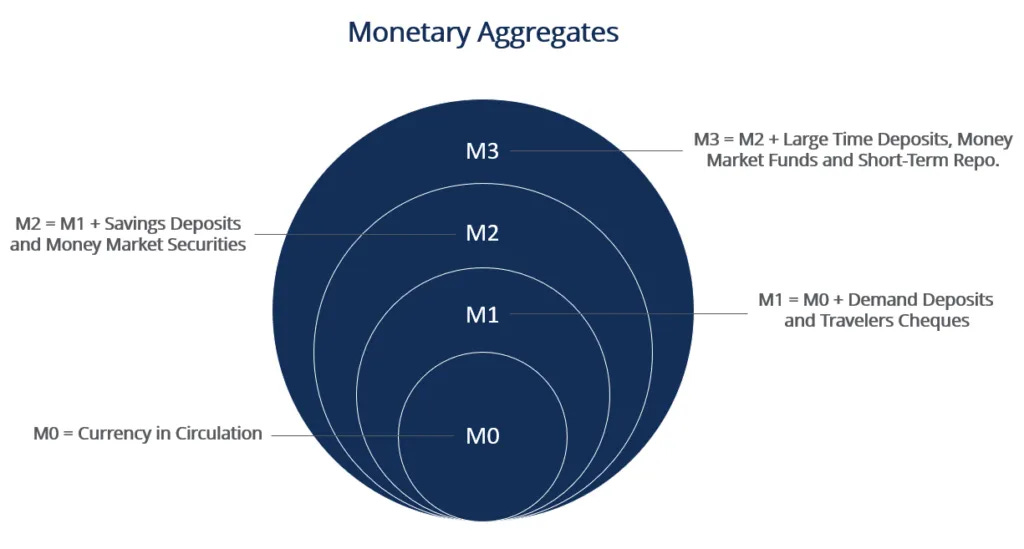

Monetary aggregates

What is money? As defined by Hicks, money must fulfill three main functions: it must be a unit of account, a means of payment, and a value deposit. Fiat money is what we have now. It has not been backed by gold since the 1970s, and thus not linked to the real economy. Today’s money is debt: what we use as money are the liabilities issued by the monetary system following the rules and regulation of the central bank, which has the legal monopoly on issued legal tender money: euros in the Eurozone, dollars in the US, etc. As long as it fulfils those three functions, an economist would say that it is “good” money. As long as inflation is low, in principle fiat money would fulfil the three functions.

Central banks decide on the monetary base M0 (money created by them directly), by injecting liquidity into the banking system via open market operations (buying bonds from commercial banks with the obligation for the latter to repurchase them at a later time). Also, central banks take regulatory decisions trying to influence banking institutions about how much money they create. From narrow to broad, the ECB defines different levels of the money supply: M1, M2, and M3.

What is the goal of regulation? Remember the elephant-shaped balloon? Imagine trying to blow in and suck out air at the same time. What would happen? Exactly.

On the one hand, central banks try to incentivize commercial banks to blow air into the balloon, to make sure markets have liquidity, and the economy can function properly. On the other hand, they expect the banks not to blow too much air into the balloon, and make sure they have enough reserves in order to resist shocks, should they come, without provoking a financial crisis.

“Credit must flow into the economy, let's create TLTROs I, II and III programmes (Targeted Long Term Refinancing Operations from the European Central Bank) and inject liquidity into the banking system on the condition that they must lend it to the real economy”, said the alchemists. “Let’s add some Quantitative Easing programmes, buying bonds and thus injecting even some more liquidity while keeping financing costs low”, they continued.

At the same time, they completed the previous: “let's increase the regulatory requirements with Basel III, to make sure the banks do not expand credit too much and they build different security buffers into their balance sheets”.

Take a balloon, for real, and try blowing into it and sucking from it simultaneously.

Are the ears getting bigger now? Then stop QE programmes at once and announce we will raise interest rates. Are the trunk and legs deflating? Then, let us delay the previous decision.

Limitations of simple analogies

Certainly, the balloon analogy is childish. Central bankers do not act like that, do they? Let me have this one. Let us instead borrow the analogy recently used by the Managing Director of the IMF:

“We act sometimes like eight years old playing soccer. Here is the ball, we are all at the ball. And we don't cover the rest of the field.“ (Georgieva, 2022)

Every analogy means a simplification with respect to reality, but certainly they help us emphasize some aspect of it. Whether we think of inflating a balloon, or we imagine 8 year-old children playing with a football, each example represents some limitation of monetary manipulation.

Market liquidity levels over the past few years have reached heights never seen before. Simultaneously, global debt and leverage have also reached all-time highs. Real estate prices, stocks, bonds, have all reached all-time record prices, breaking away from their fundamentals (real economy productivity, as well as companies’ earnings, have both increased much more slowly than asset prices). And now, finally, even consumer prices are increasing at rates unseen since the Stagflation in the 1970s.

No one can predict the future, but the risk of strong corrections in market prices exists, especially in financial markets, since these can be much more volatile than others such as real estate (people can buy and sell shares on the same day, but will rarely buy and sell a house within such a timeframe).

There is a high negative elasticity of financial assets prices to monetary policy decisions and even policy announcements, and a lot of volatility. Central banks will try now to deflate the ears without inducing big sharp corrections in the trunk and the legs. However, we should keep in mind the following: whenever playing with elephant-shaped balloons, we cannot inflate or deflate their ears without consequences on the trunk and the legs.

Let us hope central banks will focus on the entire elephant in the room.

If you enjoyed this piece, please give it a like, subscribe and share!

Thanks for reading Edelweiss Capital Research! Subscribe for free to receive new posts and support our work.

If you want to stay in touch with more frequent economic/investing related content, give us a follow on twitter @Edelweiss_Cap. We are happy to receive suggestions on how we can improve our work.

References:

Georgieva, K, 2022. CNBC Interview.

Mariana, J. d., 1609. De monetae mutatione: "Tratado y discurso sobre la moneda del vellón".