#15 Standing on the shoulders of giants

#15 Standing on the shoulders of giants

Investment principles for a happier and wealthier life

Inflation turmoil and interest rates hike are hitting markets badly in the last months. It might hurt. But now it is the time to have a clear mind and stick to your investment principles. In this post I am sharing mine. There is nothing fancy about them. Simple models thrive when problems are complex and the information is incomplete, ambiguous, and changing. They are the reflection and the result of a rational process, continuous learning and time. It was the process of ordering the set of anarchic thoughts into a simple and ordered rational model. Never forget your long term goals. Patience might be the ultimate competitive advantage of our time.

Welcome to Edelweiss Capital Research! If you’re new here, join us to receive investment analyses in 10 slides, economic pills, and investing frameworks by subscribing below:

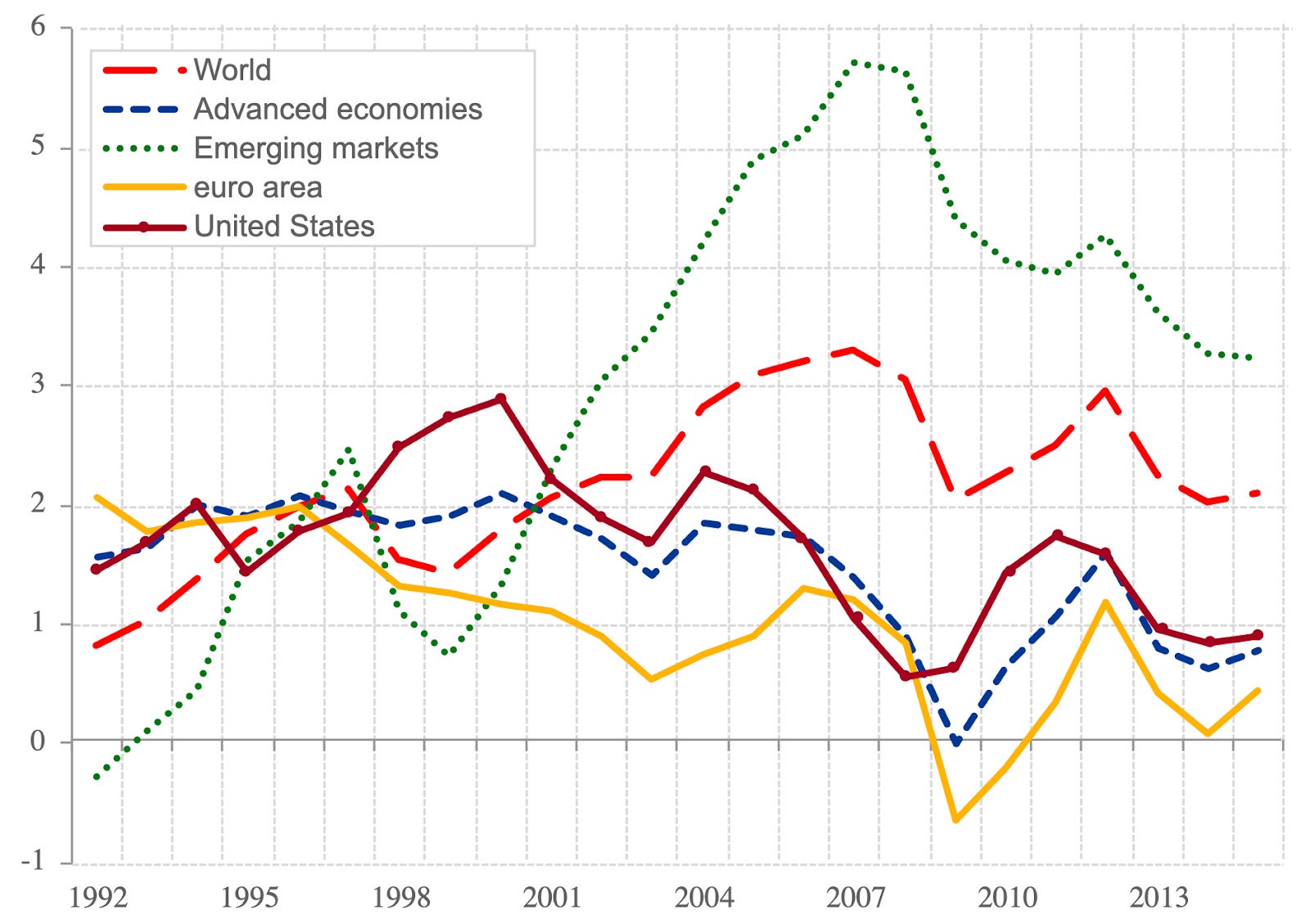

Challenges from the past, worsened

It is quite obvious for all of us that there is an overall lack of a basic financial culture worldwide. Education systems, and even universities, avoid any useful reference to these topics. Common understanding is that the stock market is a roulette and investing is equal to gambling. Only insiders with privileged information can benefit from the markets. Media does nothing else than foster this narrative.

This problems are even more pronounced in Europe, where despite the wealth accumulated over the last two centuries, it has traditionally been invested in the form of real estate and other non-productive assets. This is one of the great differences that has made the number of rich people increase at higher rates in North America than in Europe.

Additionally, Europe has forgotten the secret sauce for wealth creation and hence, citizens will be impacted in the near future. Wealthfare states have modified the capitalist values of hard work and saving, transforming our society towards the constant recognition of consumerism, new rights and a non-sustainable social protection from the state.

Rights financed by others are not rights, but privileges.

Not surprisingly, all these transformations have resulted in a ralentización of productivity growth, even despite the huge technological (and productive) advances we have experienced in the last decades.

Many citizens rely on future national pensions for their retirement, which eventually will not be enough to cover their life standards. But what is worse again, the inversion of demographic pyramid is making pension Ponzi schemes a bomb about to explode, together with unsustainable public debt levels. Guess who is already paying the bills.

We have started to suffer an intergenerational wealth step. It is already happening and it is even more noticeable in some southern European countries. Now, let’s add inflation to the equation. Inflation is a scourge that will impoverish all who don't own productive assets.

Capital is sacred. It represents the savings from a lifework. The postponement of immediate satisfaction and pleasures to the future. I despise inflation as a despotic robbery. Capital is scarce. It is the foundation to increase productivity, increase life standards and reduce poverty.

Intervention, governments and central banks have tried to make us believe otherwise. Investing in outstanding productive assets is the only way to preserve and increase our wealth, solve productivity issues and break the links and dependencies to the always insatiable voraciousness of the states.

My 10 investing principles

Many times we forget we are standing on the shoulders of giants. We don't need to reinvent anything, just replicate what the best did before us. My 10 principles are divided in 3 areas: the playground, the assets and the behavioural approach.

You can find a powerpoint version of the principles in the link:

Playground: a view to the markets

1 - There has never been a better time to invest in good business, letting compounding work to obtain outstanding results in the long term.

I believe humankind is living the biggest technological revolution ever: new companies are now more capital efficient, with better asset-light business models. Information is accessible to all, offering superior portfolio performances in the long term.

The new economy born with the internet has brought us the biggest revolution in the history of humankind. Free information is now available to the vast majority of the world population. This will create a manantial of future talent that will impact our evolution to higher levels. Productivity will keep increasing leading to an improvement on capital returns and a reduction of poverty worldwide. However, disruption and asset-light business models bring along weaker competitive advantages and barriers to entry.

2 - I do not take a position in the value-growth-quality fragmentation of investing strategies.

I am not dogmatic and I don’t believe in the unnecessary and unproductive fights. I seek the best companies, with great optionality to grow, at reasonable prices.

“Time is the friend of the wonderful business, the enemy of the mediocre.” Buffett

Only intelligent individuals have the rational mindset to be convinced, accepting they were previously mistaken. There are some great investors following each one of the different methodologies. Value can be found anywhere, but the skills needed in each one of them are different. I try to adapt my philosophy to my strengths, not otherwise.

3 - Markets are not efficient in the short-medium term, leading to opportunities for patient investors.

The stock market liquidity makes the market volatile and, many times, irrational.

“The stock market is a device for transferring money from the impatient to the patient.” Buffett

Index’ ETFs are great, indeed one of the best allocations most investors might do. But don't fool yourself. When investing in an ETF you will: buy a larger chunk of overvalued companies, underweight undervalued businesses and add to your portfolio “mediocre” businesses. Small performance differences in the annual returns compounded over years will make a huge difference in the long term. Our brain is set to think always linearly, but compounding is an exponential function

Returns of an initial investment of 10.000 € compounded at 8, 12 and 16% over 30 years

Assets: outstanding companies

4 - Look for aligned management incentives and long term thinking leaders, with outstanding and proven capital allocation skills.

This is in my view one of the most underrated principles out there. I don’t want to bother with the principal-agent problem, hence I look for “outsider” CEOs with incentives aligned with those of the investors. These CEOs will be willing to sacrifice short term results to drive long-term strategies building competitive advantages.

I seek extremely good capital allocators, using the cash flows from the business to drive shareholder value: reinvesting in the business, making bold M&A or buying back shares at correct prices. Some of the new outsiders that, in our opinion, reflect those qualities are Mark Zuckerberg (Meta), Lars Wingefors (Embracer), Jeff Bezos (Amazon), Mark Leonard (Constellation Software) or Bruce Flatt (Brookfield Asset Management).

More about them in my series of rebel capital allocators.

5 - There are two basic sources for shareholder value creation: growth and ROIC

Growth strategies based on organic new-products development frequently have the highest return because they don't require much new capital. Being in fast-growing markets is one of the largest drivers for growth. Acquisitions require the entire investment to be made up front and most of them destroy value. However, there are special companies breaking these mantras and achieving recurrent returns out of acquisitions.

Never forget sustaining high growth is much more difficult than sustaining a high ROIC.

"Over the long term, it's hard for a stock to earn a much better return than the business which underlies it earns. If the business earns 6% on capital over 40 years and you hold it for that 40 years, you're not going to make much difference than a 6% return—even if you originally buy it at a huge discount. Conversely, if a business earns 18% on capital over 20 or 30 years, even if you pay an expensive looking price, you'll end up with a fine result" Charlie Munger

6 - Real and sustainable competitive advantages are scarce.

I believe corporate strategies must be the path to build and preserve competitive advantages. Real moats are scarce and are reflected in higher ROIC values than competitors.

I believe there are 4, and only 4, sources of competitive advantages. If a company doesn’t have any of those, better they are on their way to build one of them or they are the lower cost option:

■ Innovative/superior product technology: 10x superior product than any competitor. They are normally a short-term source of advantage (e.g. Google search engine)

■ Network effects: customers unable or unwilling to replace a product/service because the benefit gained from switching is negative or small relative to the cost of switching (e.g. Microsoft office, AWS, Meta)

■ Economies of scale: efficient scale in the market, allowing to create barriers to entry and add customers/capacity at marginal negibible cost. Nick Sleep tweaked the concept to scale economics shared (e.g. Costco or Amazon)

■ Brand: creating perceived product differentiation through a trusted brand or reputation, where customers are willing to pay a premium for certain products/services (e.g. Apple or LVMH Louis Vuitton Moët Hennessy)

7 - Invest in businesses whose assets are intangible and difficult to replicate, natural monopolies or economic niches having scale, barriers to entry and pricing power. Never forget that valuation matters, so don’t overpay for any asset.

Some of the best companies I have found so far share some particular characteristics. History doesn't repeat itself, but it often rhymes.

■ Decentralized organisations: autonomy and responsibility attract the best managers

■ Entrepreneurial/serial acquirers: many of them have the founders still running the company. Others have a programmatic approach to M&A with frequent small acquisitions

■ Frugal companies: they know they are expending shareholders' money in their operations and therefore, treat it carefully. Mark Leonard rarely flights in business despite being almost 2m long and 150kg

■ Focus on FCF rather than earnings: Earnings is an accounting concept that increases the amount of taxes. John Malone grew TCI stock price at a compound annual rate of 30.3% over 25 years, hardly reporting any earnings

■ Management compensation: many times these companies pay extremely low/none salaries to their CEOs

Finally, price matters. When valuing a business, we are assessing future performance. We are just guessing the competitive situation of the company in the future and its capacity to generate FCF attributable to shareholders. My approach here is simply to assess which is the performance priced by the market discounted at my desired minimum IRR. If I consider the projected FCF reasonable or conservative, I found an investment.

Behaviour: embrace a long term mindset

8 - Avoid taxes and market timing. Never interrupt compounding

I understand there are some mature businesses where the best capital allocation possible is to return the cash flows back to the owners via dividends. I avoid such businesses as I intend, ideally, never to interrupt compounding. If tax rates were 0, I would change my view towards dividends. As I don’t foresee they will, I try to avoid high dividend yield companies.

9 - Volatility is just part of the process and bring opportunities. Volatility is not risk.

Public market volatility is nothing else than an uncoerced human psychology game. I consider volatility creates some little opportunities where to buy great business at discounted prices. However, we must remain cautious. Markets are not necessarily always right, nor are they always wrong.

Many times volatility and risk are used interchangeably. They are not. Risk is the possibility of a permanent capital loss. Volatility is the price change of an asset. Market volatility increases the possibility to buy assets cheaper, hence reducing the risk.

"The riskiness of an investment is not measured by beta but rather by the probability of that investment causing its owner a loss of purchasing power over his contemplated holding period. Assets can fluctuate greatly in price and not be risky as long as they are reasonably certain to deliver increased purchasing power over their holding period." Buffett

10 - The right temperament for investing is scarce. Patience might be the ultimate competitive advantage.

I embrace infinite patience as I intend to be owner of the best businesses on the planet, benefiting from the beauty of compounding. I do not believe I have the right knowledge to predict what the markets are going to do in the short or medium term. Over the long term, markets tend to be efficient and price assets the correct way.

Therefore, my focus is only in companies delivering value to its customers, and eventually, to its shareholders. This approach to investing, even being shared by many, is applied only by little. Our current lives are programmed to achieve short term results. If not, you have failed. Investing and compounding work differently.

Future is uncertain. I can not guarantee success or to outperform the market following these simple principles. I “only” promise a happier and wealthier life if you embrace, believe and trust on your principles.

If you enjoyed this piece, please give it a like, subscribe, and share!

Thanks for reading Edelweiss Capital Research! Subscribe for free to receive new posts and support our work.

If you want to stay in touch with more frequent economic/investing-related content, give us a follow on Twitter @Edelweiss_Cap. We are happy to receive suggestions on how we can improve our work.

hi, loved this piece but have one quick question. Why did you think lars was a good capital allocator?