#5 Inflation and the inevitable hangover

#5 Inflation and the inevitable hangover

Limiting market prices has always failed. Why should it be different with money?

The basics

The price of any given good or service is determined by its supply and demand. If something is cheap, that means it is rather abundant, whereas expensive things tend to be scarce. We offer less of something if it is cheap, and more of that same thing if it is expensive. Conversely, we demand more of something if it is cheap, and less of it if it is expensive. Where these two curves meet, we have a market price for that particular good. The same happens with money. Abundant money means cheap money. Scarce money means expensive money. The price of money has a somewhat special name: interest rate.

Inflation is usually described as a persistent increase in the level of consumer prices, or a persistent decline in the purchasing power of money. The rate of inflation is the rate at which this increase occurs, expressed as a percentage over a period of time, usually a year. As Nobel laureates Hayek (1974), Friedman (1976) and Lucas (1995) explained, inflation is always a monetary phenomenon caused by an increase in the quantity of money. There are a few exceptions to this rule, such as natural disasters that act as exogenous shocks and alter supply chains, but in modern economies it does almost invariably have a monetary origin.

These two elements have a stronger connection than it might seem at first sight. Intervention in the price of money to make it artificially cheap invariably produces negative consequences for the economy in the form of high inflation. If authorities refuse to acknowledge their responsibility and insist on their intervention, consequences can reach devastating levels in the form of hyperinflation.

For the better part of the 21st century, the world has had historically low interest rates. This situation has fostered a steep increase in the valuation of virtually every asset and company throughout the market, granting investors juicy profits, at least on paper. However, there is a downside.

This unprecedented access to inexpensive money was the perfect breeding ground for the inflation we are currently suffering, unseen in over four decades. The party is over, although our leaders might try to keep the music running and pour more booze into our throats. The hangover is inevitable.

In this article we will try to explain how it happened and what should be learnt to prevent it from happening again. Spoiler alert: we won’t.

Inception

After 9/11, the Federal Reserve lowered interest rates from 6.5% to less than 2%. Other central banks around the world followed, and the abundance of cheap money generated several investment bubbles throughout the world. Especially famous were the housing bubbles that altered urban landscapes in Europe and the USA. After a slight hike in the period 2006-2008, the Great Recession began and interest rates were cut to less than 1%. From that moment until 2022, they have been around 0% most of the time, even with some incursions into negative field. This has brought about high inflation, much higher than the 2% limit established by many central banks. Not only that, but it is very likely that we see double digits in the upcoming months.

In a free market, the price of a product expresses three types of information: relative scarcity, cost of production, and subjective preferences from consumers. On the one hand, prices inform consumers about what can be purchased in smaller quantities and what should be purchased in larger ones. On the other hand, prices also indicate producers where they should invest in order to maximize revenue, i.e., wherever other sellers are reaping extraordinary profits. If prices are artificially fixed by the government, the information distributed to the rest of economical agents is faulty, and so will be their consumption and investment. This is applicable to the price of money as much as it is to the price of any given product.

In a fiat-money system, this price is intervened by definition, since the currency is not linked to any real good (traditionally, gold) and therefore can be created out of thin air. Authorities react raising or lowering interest rates depending on inflation (ECB, Fed) and unemployment (Fed). The opposite of fiat money is commodity money. In such a system, interest rates change automatically depending on savings, with no central authority managing them.

The consequences of government intervention

Let us picture a society whose members save much and spend little. Whenever an entrepreneur looks for investors for a project, they will find a lot of money available, therefore offered at a low interest rate. On the contrary, a consumerist society will only be able to offer high interest rates to whomever wants to start a company or buy a house, since most of the wealth they generate is immediately consumed and, consequently, not available for other goals. It is important to understand that low interest rates do not merely represent a lot of money in stock, ready to be used. Without government intervention, the availability of money is linked to the availability of other resources, both physical and human, and to the temporal preference of agents in the economy, a concept first described by Martín de Azpilcueta (Álvarez, 2017) and later explained by Böhm-Bawerk, with his Robinson Crusoe analogy (Böhm-Bawerk, 1890).

Keeping interest rates artificially low for a prolonged period of time conveys the wrong message that savings are abundant. As a result, more investors will borrow more money for more projects than they would in an intervention-free system. This gives the false impression of a healthy economy, one with new businesses being opened and new housing developments being started every day. However, there are no real resources to back it all up. These resources are not just savings, but also idle workers and capital goods.

In this scenario, people have not sacrificed present consumption. Instead, they have engaged in ever-growing spending taking advantage of the cheap money available, unconsciously assuming that someone else has previously saved. After a while, the consequences of this misguided policy begin to be noticed. Consumers want waiters to serve them dinner, concrete for their houses and steel for their cutlery. Investors, on the other hand, need miners to extract ore and furnace workers to transform it; they need concrete for their factories and steel for their tools. Since consumers and investors are competing for a limited pool of resources, prices invariably go up. More has to be paid for a ton of iron, more has to be paid for a kW*h of energy, and more has to be paid to a worker to shift them from one sector to another. To keep margins positive, businesses bring prices up. Now everyone can buy less with the same amount of money, so workers start demanding higher salaries to retain their purchasing power. Indeed, nominal wages must go up if real wages are to be stable. If these demands are met, prices of goods and services will have to go up again to keep margins positive. This process is known as wage-price spiral, and we can see how it contributes to increase inflation even further. Let us realize that even if salaries and prices were to grow at the same rate, savings in checking accounts would not, so savers would see their real wealth diminished.

The way out

We should not lose sight of the original source of the problem: central banks establishing artificially low interest rates. At the end of the day, this action devalues their currency, not only with respect to other fiat currencies whose central banks apply higher interest rates, but also with respect to real goods and services produced in the economy. As we pointed out, this has been happening almost non-stop in the Western Hemisphere for the past twenty years. What can be done to solve the problem? Raise interest rates, often dramatically. Only by doing so can the economy cool down: investors will embark in fewer enterprises, people will buy fewer consumer goods and resources will be less demanded. Some businesses will shut down, freeing their resources for other more valuable purposes. In the short term, this means unemployment will soar and stock markets will plummet. Accordingly, some workers in consumption-related sectors will lose their jobs, which will send the signal that society does not demand as many consumer goods and services as before, and that investors should focus on what Menger called higher order goods (Menger, 1871). This process is described in detail in Money, Bank Credit, and Economic Cycles (Huerta de Soto, 1998), as well as by other authors of the Austrian School of Economics, such as Wicksell, Böhm-Bawerk, Mises, and Hayek.

After the rise in interest rates, only those projects where high returns are expected will be undertaken. If the bank offers loans at 1%, pretty much every investor will take the risk, since their expected return will almost always be above that level. However, if the demanded interest is 10%, only those who expect a higher yield will go for it. This means that resources will only be allocated to enterprises capable of creating the highest value for society.

The reallocation of the factors of production takes some time, and this temporary cooling of the economy brings with it a reduction of the inflation. Without government intervention, it even produces a reduction in prices, i.e., deflation. However, if the government tries to rescue declining sectors by pouring taxpayer’s money into them, they will only prolong and increase the pain while keeping demand artificially high and not freeing those resources.

What History can teach us

There are many examples throughout History where central bankers have altered interest rates trying to boost their economies, defying the logic behind and expecting a different result. As we can imagine, they did not succeed.

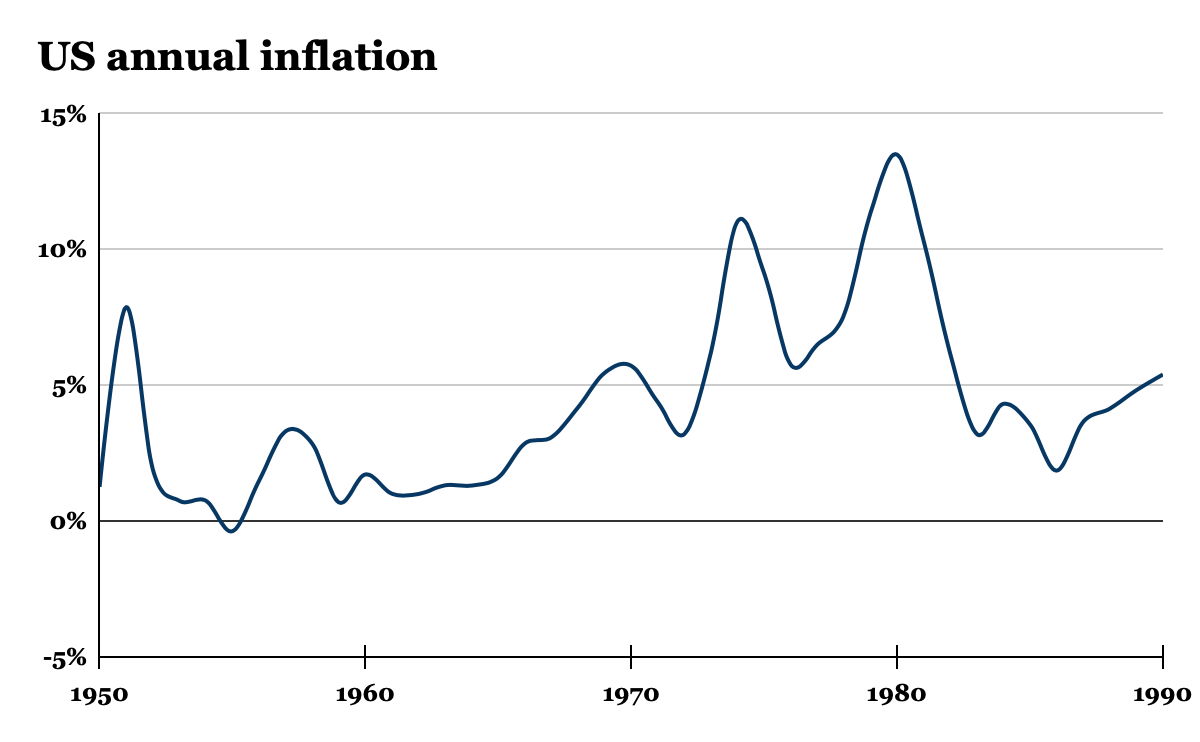

The USA increased their expenses during the late 1950s and all of the 1960s as a consequence of the Vietnam War, Johnson’s Great Society, and the Space Race with the USSR. They all entailed enormous expenditures for the federal government. Interest rates during this period were below 6%, while inflation was kept at bay below 4%. After the first oil crisis (1973), inflation rose above 10%. After the second one (1979), it almost reached 15%. Shortly after being appointed Chairman of the Federal Reserve, Paul Volcker raised the short-term interest rate to 20%, effectively bringing inflation down to 3.5%. It was a heavy blow on the economy, one that sent unemployment soaring to nearly 11%, but it would have been heavier had it not been taken at that point.

After a decade of little economic growth in the 1990s, Spanish GDP rose at an astonishing rate during the period 2002-2008. The reason, as we have seen, was the abnormally low interest rate established by the first two presidents of the ECB, Duisenberg and Trichet.

Unemployment rate hit a record low of 8.2% in 2007. For a country like Spain, with an average unemployment level of 17% since 1980, this was completely unprecedented. Spain created more jobs than Germany and France combined, with less than a third of the population. And most of these jobs were created in the housing sector. Public income was so high that the government could not spend it quickly enough, and (unintentionally) repaid part of the national debt.

When the bubble burst, the government tried to keep unemployment from skyrocketing by increasing expenses in public works, which effectively doubled Spanish national debt in just four years.

Final thoughts on the matter

Now we have a better understanding of how we got here. We are inevitably approaching a crisis. If central bankers decide to change course and raise interest rates, a recession will take place. Stock markets, employment levels, consumption... they will all be severely affected. However, if bankers try to avoid it and insist on keeping interest rates low, inflation will only get higher and the future recession will get bigger. Inflation is a poison, and the only medicine is a high interest rate. It will hurt, but it sure is the right thing to do.

Political use of interest rates is no more than government intervention in market prices, something as old as the world. Every time it has been tried, inflation has eventually climbed and people have suffered. Let us learn from the past and make our leaders accountable for their decisions.

We have reviewed what is happening and why we are heading for a credit crisis. Short-term economic and financial events will be highly dependent on policies enacted by central banks.

In an upcoming post, we will explore if investors have any tools to defend themselves against inflation.

A. Valverde

References:

Álvarez, F., 2017. La escuela española de economía. Madrid. Unión Editorial.

Böhm-Bawerk, E. (1890) Capital and Interest: A Critical History of Economic Theory. London. MacMillan and Co. https://cdn.mises.org/Capital%20and%20Interest_0.pdf

Huerta de Soto, J. (1998) Money, Bank credit and Economic Cycles. Madrid. Unión Editorial. https://cdn.mises.org/money_bank_credit_and_economic_cycles_4th_edition.pdf

Menger, C. (1871) Principles of Economics. Ludwig von Mises Institute. https://cdn.mises.org/principles_of_economics.pdf