#29 Adobe: creativity at scale

#29 Adobe: creativity at scale

The rise, and current fall, of an undoubtedly great business with a questionable capital allocation

Adobe has grown to become one of the largest software companies in the world. It leads the industry in many markets where its product names are etched in the collective imagination. Acrobat, Photoshop, Premiere Pro, Illustrator, or After Effects to name a few. It is a leader in many of the main creation software in a more and more multimedia society. Recently, however, the stock price has taken a big dip following the announcement of the acquisition of Figma for a whopping $20 billion (more on that later). But this is almost the bright side of the story, as the total drop is about 60% from last year's high. Is the market discounting something we don't know about, or is it just too irrational to lose sight of the long term?

Welcome to Edelweiss Capital Research! If you are new here, join us to receive investment analyses, economic pills, and investing frameworks by subscribing below:

The golden goose

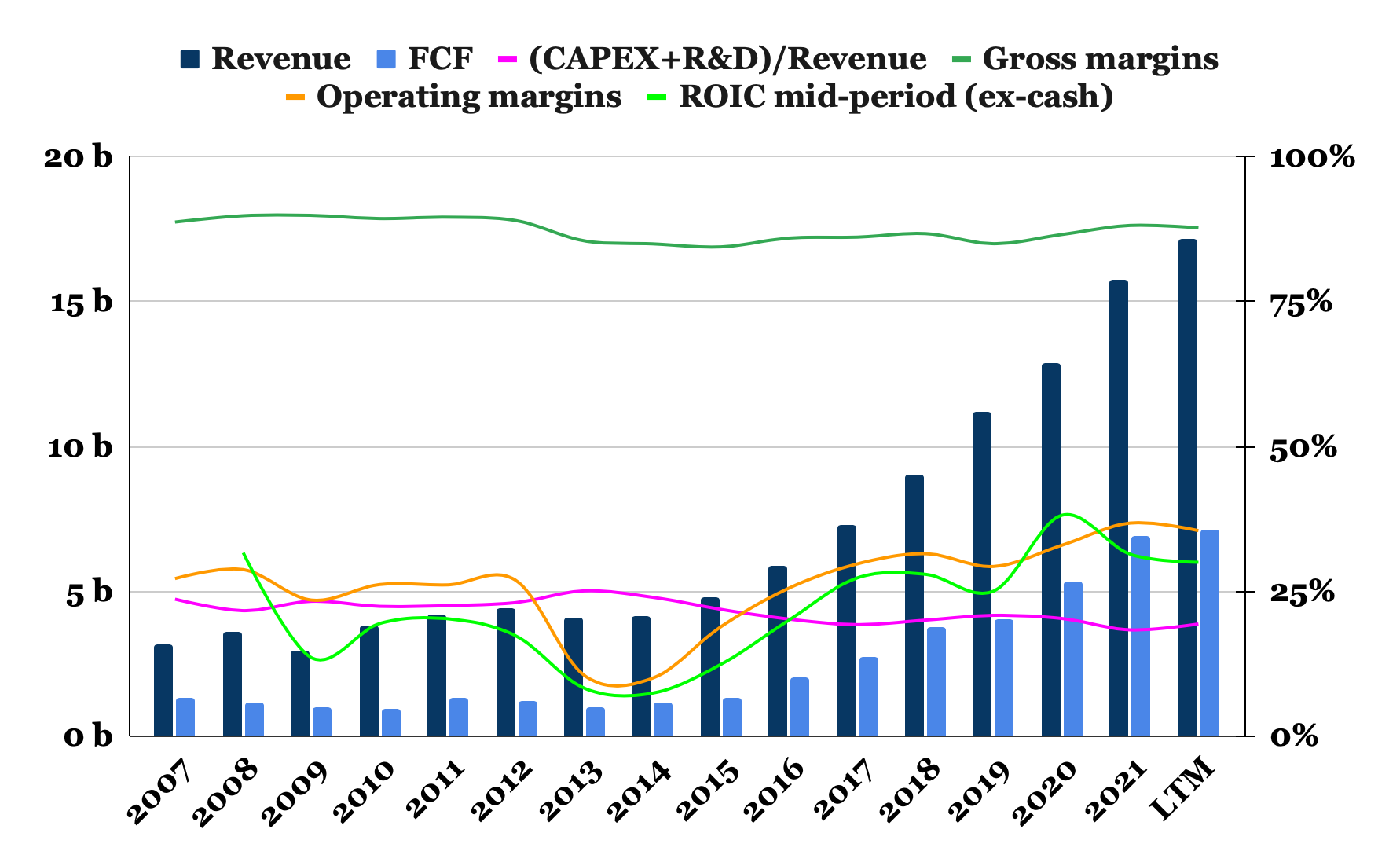

In 2012 Adobe shifted its business model from selling products to a cloud-centric SaaS model. The numbers don't lie, after a couple of tough years, as of 2014 revenue and FCF generations have shown that they made one of the most successful business model pivots in history. Today, with an impressive 22% 5-year CAGR revenue growth, subscriptions account for 92% of total revenue versus 4% coming from products. It also enabled Adobe to improve its ROIC to 30% today and expand operating margins to over 35%.

Adobe's management was able to adequately predict and lead the global trend that was beginning. Initially, there was some resistance as many complained that they were "ripping off" small businesses and creators by charging more with the subscription model (Change.org, 2013). Today this anecdote may be seen as pointless as we get used to the SaaS model, but it wasn't that long ago, and it was a long battle. They argued that this model allowed it to deliver continuous improvement and innovation (McKinsey, 2015). The reality is that the old licensing business model was not able to capture as much of the value generated by customers. They were generating it, they just weren't able to charge more for the one-time payment licenses. The SaaS subscription system was clearly better.

Adobe has matured its business model. For example, Creative Cloud offers $10 to $20 per month for individual software and around $55 per month for the entire suite. Subscription packages could become a de facto standard for creative professionals similar to what Microsoft has achieved with Office.

The insides

Adobe's portfolio includes dozens of businesses in one of the most diversified software companies in the world. They divide their business into 3 segments: Digital Media, Digital Experience and Publishing & Advertising. Although the latter is declining and we can consider it insignificant.

Digital Media is the main one and it includes:

Creative Cloud contains all their creative apps such as Photoshop, Illustrator, Premiere Pro, etc. It is also the main branch of the business, accounting for 60% of total revenues, and has grown at a year-on-year rate of 26%. However, FY22 shows a slowdown in growth (across the board in all segments). However, due to the current macro environment, this is not a major concern in the long term.

Adobe Document Cloud includes the infamous Acrobat and the suite of products that allow you to edit and digitally sign pdf. It's probably not the sexiest product in the world, but it's still the market leader and a standard for businesses around the world. It accounts for 13% of revenues and is growing at a healthy five-year CAGR of 27%.

The digital media segment has a gross margin of 96%, and only a few companies in the world are able to achieve these figures. The extraordinary margins and growth demonstrate the quality of the products and their leadership in many of the markets they serve. Of course, this status is not guaranteed as new and better competitors may appear as has happened with Figma or Canva. The company has to keep performing to keep the crown. Buying out all competitors is not a viable long-term strategy.

On the other hand, Digital Experience provides an integrated platform with a wide variety of applications and services that enable companies to create, manage, execute, measure, monetize and optimize customer experiences, from analytics to commerce. 25% of revenue is created by this segment and it is growing at a 5-year 18% CAGR. However, here Adobe only has a "mere" 66% gross margin. Clearly, this segment is more resource-intensive and they do not have such a strong brand moat. In addition, it competes with strong and well-established competitors such as Salesforce and Oracle. Although gross margins are below those of the competition, a good sign is a consistent increase over them in recent years.

It is also important to note the strong brand moat that many the products have. This is especially interesting in applications that are industry standards. This creates network effects where there are hundreds of thousands of professionals proficient with their software, and thousands more joining the workforce each year from schools and universities. This creates a positive feedback loop, as companies tend to stick with the same applications as they can fish in a larger talent pool. This reinforces the switching cost moat that Adobe also enjoys. However, as we mentioned earlier, even the strongest moats such as these can be eroded by competition if the company is not able to continue to provide the best product in the market.

Leveraging the AI revolution

IDC predicts that the cloud market will grow at a 10% rate through 2025 (Villars et al, 2021). Adobe, for its part, claims that the TAM of its different segments will grow at 40-50% and that it is only capturing a portion. Of course, we have to take these figures with a grain of salt. In any case, we are confident that more and more of the multimedia world will continue to fuel the growth engine. In our baseline scenario, we consider a slight reduction on current revenue growth of 22% CAGR over 5 years.

In any case, we believe that AI is bringing a productivity revolution rarely seen in human history. The amazing technologies we are seeing these days like Dall-E, Stable Diffusion or GPT-3 are the gears and engines of this industry. But software from companies like Adobe is the car that gets you places. Many of their products are extraordinarily positioned to take advantage of the AI revolution. So we also see an optimistic scenario where they will be able to sustain the current level of growth over the medium term.

The captain of the sailboat

Shantanu Narayen joined Adobe in 1998 with a background in engineering. By 2007 he was CEO and president. What he has achieved in his long tenure is quite remarkable. The business is a printing machine and the balance sheet is extraordinarily healthy. The beauty of this business is the entry lines of unearned revenue and accrued expenses totaling $6.5 billion in liabilities, making it a business with negative working capital needs, which helps show a balance sheet with negative net debt. But even if he is primarily responsible for such success, it is only a small fraction of his responsibilities as CEO. The main driver of value creation in these splendid companies is actually the capital allocation. And we have something to say about that: “Show me the incentive, I'll show you the outcome”.

Mr. Narayen has a low base salary of only $1 million. Short-term incentives are tied mostly to ARR growth and can amount to an additional $2 million. But the real pot of gold comes with the long-term incentives that are tied to relative Nasdaq performance (Adobe, 2020). The latter pegs the real equivalent salary at $45 million in 2020. The overall count is that his equivalent salary over the past 10 years has been $260 million, 90% of which was in the form of shares. However, his total wealth in stocks adds up to "only" $124 million. Not perfect, but even so, most of his wealth is closely tied to the fortunes of his shareholders.

Playing devil's advocate, if my incentives compel me to increase both revenue and stock price, what's the shortcut to get there? Spend as much as possible on sales and "copy" the QE strategies of central banks by buying back shares to inflate my stock price. It just works. Adobe spends a not inconsiderable 30% of its revenue on sales and marketing and, surprisingly, includes amortization of old contract acquisition costs. This capitalization of sales expenses (Adobe, 2022) means that the company was “artificially”, although legally, boosting past and current profits.

Another fair criticism is the questionable value generated for shareholders with the share buyback program over the last decade. A quick calculation taking into account shares repurchased, issued and SBC over the past 10 years shows that Adobe has spent $12.6 billion to reduce the number of shares by 33.7 million. This leads to a price per share of $373 on average. This is above current prices and is surprisingly high when looking at the price over the past few years. An example of misallocation of capital, as the share repurchase program did not take into account the share price, and most of the cash was spent when multiples were well above average.

We've talked about it many times here, but massive share buybacks when valuation multiples are artificially inflated by monetary policies and a bubbly market sentiment lead to the destruction of long-term shareholder value. Something may backfire in the coming years as the IRR on these investments on behalf of shareholders may not exceed the opportunity cost of most of them. A good management team should be aware of this and act accordingly. Of course, those buyback programs resulted in Adobe outperforming the Nasdaq and the management team pocketing their hefty rewards.

Figma & other acquisitions

Despite the company’s current throne, innovation and competition are fiercer than ever. For example, in the creative cloud arena, new players, such as Figma and Canva, have emerged with compelling software. They tried to compete with its own product, Adobe XD. But it wasn't good enough and they lost the battle. So they decided to buy their most dangerous competitor, Figma. It was a damage control strategy. An expensive strategy. Adobe paid more than 50 times Figma's expected ARR for FY22, the equivalent of 3 years of Adobe's all-time high FCF.

This has been a common strategy at Adobe since its infancy (Wikipedia, 2022). And it can be argued that costly acquisitions like Macromedia in 2005, at 10x sales (Flynn, 2005), or Marketo, at 19x revenue (Adobe, 2018), helped build the position Adobe has today. Clearly, neither of these acquisitions would work in terms of ROI. However, this would be the wrong way to think about them. The exercise to do would be to assess the probabilities of the different scenarios. What are the odds that we let Figma grow and that in 5 years it will have taken 20% of our market share? How will this be reflected in our cash flows and competitive position? This is the right analysis and one that almost no one does.

But the Figma acquisition is, to say the least, questionable. Only time will tell. On the bright side, the transaction is more than just the purchase of the product. It is the purchase of the team that was able to win the battle against Adobe. The deal closed for about $10 billion in cash plus $10 billion in stock. In addition, 6 million shares will vest over the next 4 years to Figma's current CEO, who will continue to lead the project and its employees. If you are a regular reader of our reviews you already know that for us shares are sacred and should not be given away lightly, especially if what we receive is no better than what we give away.

Besides, something we haven't read anywhere so far is the fact that Adobe's $20b new goodwill will make invested capital go from $18b to about $38b. What's the problem with this? Well, the company, with just this one transaction, will double its total invested capital all at once, which means that next year the ROIC will drop from 30% to 15%.

Valuation

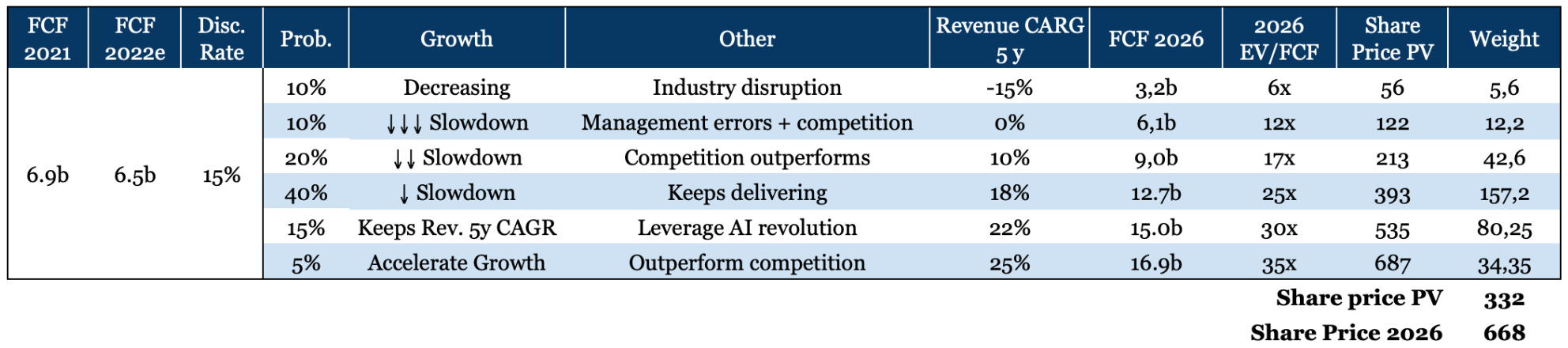

You know we are not very fond of valuation. For us, it is just a necessary checkpoint to understand the performance the market is expecting and think in terms of probabilities for different scenarios. In the end, we find a number that we are comfortable with. And this time there have been more internal discrepancies than usual.

We are not comfortable with Adobe's capital allocation, but the business is exceptional. Everyone must decide their relative confidence with the 3 metrics we consider fundamental to the decision process for adding a position in the portfolio: quality of the business, management, and price.

For us, the conviction is not yet there. Therefore, and for the time being, we will remain on the sidelines to see how events evolve.

Just as a final note, the current "depressed" price is discounting a 5-year CARG of ≈15%, maintaining profitability and an EV/FCF of 25x in 2026.

If you enjoyed this piece, please give it a like and share!

Thanks for reading Edelweiss Capital Research! Subscribe for free to receive new posts and support our work.

If you want to stay in touch with more frequent economic/investing-related content, give us a follow on Twitter @Edelweiss_Cap. We are happy to receive suggestions on how we can improve our work.

Disclosure: We don’t currently have any position at Adobe. Everything expressed here is only our opinion. Always do your own research.

Victor Peña & JPA

References:

Adobe (2018). Adobe to Acquire Marketo. Link

Adobe (2020). DEF 14A: Notice of 2020 Annual Meeting of Stockholders and Proxy Statement. p. 37. Link

Adobe (2022). SEC filings and financial documents. Link

Change.org (2013). Adobe Systems Incorporated: Eliminate the mandatory "creative cloud" subscription model. Link

Flynn, L.J. (2005). Adobe Buys Macromedia for $3.4 Billion. NY Times. Link

Hardman, T. (2019). Why Adobe Shifted to a Subscription Model. Link

McKinsey (2015). Reborn in the cloud. Link

Villars et al. (2021). Worldwide Whole Cloud Forecast, 2021–2025: The Path Ahead for Cloud in a Digital-First World. IDC. Link

Wikipedia (2022). List of acquisitions by Adobe. Link

Great comprehensive coverage of a great business, great for a Sunday read! Thank you!

Complementary, just 2 charts I shared on twitter with the Free Cash Flow & Share Buybacks overviews: https://twitter.com/Maverick_Equity/status/1579068575398387712

Hi Victor and JPA,

Thank you for your article on Adobe. I was particularly intrigued by your conclusion of Adobe's capital allocation policy. While I do appreciate that you have reached your own conclusion I would like to share some thoughts regarding this:

1) The conclusion on the capital allocation policy is based on past actions and the current share price performance. Playing the devil's advocate, if the share price instead increased by 30% since their last purchase, would your conclusion on capital allocation policy change? Mine would have, which made me rationalize and decide that it would be due to hindsight bias that looking at the current share price in determining a successful capital allocation policy is deemed unsatisfactory.

2) Carrying on from your comments regarding the capital allocation policy, I dug into the quarterly statements for Adobe over the past 5 years. An interesting conclusion can be drawn from doing this. The main feature of their share buyback policy is that they are in the market every month via a financial institution. My conclusion would thus be that their capital allocation policy is at best neutral and at worst unthoughtful.

3) As something that is c. 3x more capital intensive than acquisitions, I believe that management should deploy more management energy and thoughtfulness into their share buy backs. Some mechanical start and stop thresholds based on valuation (as you alluded to when you said they did not consider valuation) would be a prudent way to start and still be aloof.

4) Building on a wider framework to analyze their capital allocation policy, I thought of ways that management uses capital. The three chief ways capital can be utilized is via debt, shares, and operating cash in my opinion. On the front of debt capital usage, it appears they are not inclined to turbo charge debt to buy back shares. On the shares front, that capital has been used to reward management via SBC and to make acquisitions. On the operating cash front, the main use has been to buy back shares and make acquisitions. Thus, I personally concluded that a look at their capital allocation via their acquisitions would make better sense. On this front, over the past 10 years, they have spent north of 10bn in cash on acquisitions and probably issued many shares along the way to the founders/CEO of the acquired firms. However, over the same 10 years, their total write-down, impairments, and restructuring charges amounted to 50m dollars (From Capital IQ, correct me if I am wrong on this). From this angle, when management deploys capital to acquire companies, it does so in either an extremely shrewd way or there's some nefarious thing like non-reporting of impairments.

So when I look at Adobe and their capital allocation policy, what I see is that they appear to be soggy fried chickens with regard to when and how to buy back shares, something maybe they should work on but is not the end of the world if they continue with their current policy. However, that should not detract from the value they have created and their extreme success at acquisitions.