#59 Building blocks of corporate accounting: goodwill

#59 Building blocks of corporate accounting: goodwill

Goodwill in business: more than just benevolence (Nagarro, ICON and JTC)

In the tapestry of financial reporting, there's something akin to a magic word that gets tossed around, yet often escapes our day-to-day scrutiny: goodwill. It's not about friendly gestures or benevolent acts in business. No, it's an accounting concept that can be as elusive as it is pivotal. "Company A's massive goodwill from recent acquisitions", "Company B's surprising goodwill impairment" – such statements may flash across financial news, but what's the story behind them? Sometimes, it's the hidden figures that hold the key.

Embarking on a new journey in our series, we're rolling up our sleeves to delve into the heart of goodwill. It's more than just numbers on a balance sheet; it's about the essence of acquisitions, the subtleties of value, and the very character of corporate management. Not everything wrapped in a balance sheet is as it appears.

Welcome to Edelweiss Capital Research! If you are new here, join us to receive investment analyses, economic pills, and investing frameworks by subscribing below:

Goodwill is an intangible asset that arises when one company acquires another for a price higher than the fair market value of its net identifiable assets. This premium represents the value of a company's brand reputation, customer relationships, intellectual property, and other intangible factors that do not have a specific monetary value on the books. It's a reflection of the value that the buying company sees in the target's future earnings potential, synergies, or strategic positioning.

When Facebook acquired Instagram for $1 billion in 2012, the tangible and identifiable intangible assets were valued far below the purchase price. The difference was recorded as goodwill, reflecting the perceived value of Instagram's user base and growth potential.

In financial reporting, goodwill serves as a vital indicator of a company's strategic decisions and how those decisions are playing out over time. It offers insights into the management's ability to leverage acquisitions for growth, the success (or failure) of merger integrations, and the sustainability of the company's competitive advantages. Goodwill, being subject to potential impairment, can also signal underlying problems with an acquisition or with the broader business landscape, reflecting changes in market conditions, competition, or other factors that reduce the perceived value of the acquired assets.

Changes in Accounting Standards

Historically, goodwill was treated as an asset that needed to be amortized over a period, often 40 years. This amortization would reduce the value of goodwill on the balance sheet gradually, reflecting the idea that the value of intangible assets diminishes over time.

Before the adoption of FASB Statement No. 142 in the U.S., companies like IBM and General Electric would amortize goodwill over a fixed period. This had significant tax implications and affected net income reporting.

With the introduction of new accounting standards like IFRS 3 and ASC 350 in the U.S., the practice of amortizing goodwill has largely been replaced with annual impairment testing. This means that instead of automatically reducing the value of goodwill over time, companies must assess whether the value of the intangible assets associated with goodwill has been diminished. If so, an impairment charge is recorded to write down the value.

This shift in how goodwill is accounted for represents a more nuanced and realistic view of how intangible assets retain or lose value over time. Note, however, that they never increase. Instagram is now far more valuable than when Facebook acquire it, but the goodwill valuation in the balance sheet remains the same.

The move from amortizing to impairment testing reflected an understanding that the value of goodwill doesn't necessarily diminish in a linear fashion and that market conditions, management decisions, and other factors can cause sudden changes in value.

A counterpart to this change is that goodwill impairment is no longer deductible from the taxable base for taxes. In other words, no impairment will reduce your taxes because your accounting profit is lower.

Impairment of Goodwill

Goodwill impairment occurs when the carrying value of goodwill exceeds its fair value, meaning that the intangible assets associated with goodwill have lost value. This necessitates a write-down of the goodwill's value on the company's balance sheet.

Several conditions might lead to goodwill impairment, such as changes in market conditions, new competition, regulatory changes, or negative changes in the use of underlying assets.

In 2012, Microsoft recorded a $6.2 billion impairment charge related to the goodwill of its Online Services Division, largely attributed to the underperformance of the aQuantive acquisition.

Sprint's 2008 goodwill impairment of $29.7 billion was a result of fierce competition and regulatory challenges that led to a reevaluation of its brand and customer relationships' worth.

When impairing goodwill, companies must recognize a non-cash charge on their income statement, reducing net income. On the balance sheet, the carrying value of goodwill is reduced by the impairment amount.

Impairing goodwill has its benefits and drawbacks.

Pros:

Transparency: Reflects the actual value of intangible assets, providing more accurate information to investors.

Cons:

Earnings Impact: The impairment charge can significantly reduce reported earnings, leading to a potential drop in stock price.

Perception of Failure: Large impairments may signal mismanagement or overpayment for acquisitions, affecting investor and market confidence.

What management would want to acknowledge a mistake in an acquisition or a loss (even if it's non-cash) in front of their investors in the name of transparency? Sounds like a joke, right?

Well, they are supposed to have auditors checking their impairment checks to provide a fair valuation, but sadly, as we will see below, they are not very effective…

Impact on Financial Metrics

Effects on Profitability

This is a very clear one: impairing goodwill has a direct impact on a company's reported profits. And we all know how much Wall Street loves earnings…

Impact on Return Ratios

The impairment of goodwill may paradoxically improve certain financial ratios like Return on Equity (ROE) and Return on Invested Capital (ROIC). Despite leading to reported losses, the reduction in assets (due to the impairment) may increase these return ratios, making the company appear more efficient in its use of capital.

HP's $8.8 billion impairment related to its acquisition of Autonomy led to a significant loss in 2012. However, the impairment also improved ROE, as the equity base was reduced.

Goodwill and Management Reporting

Management might strategically use goodwill impairment to their advantage. Impairing goodwill at a particular time might align with other business strategies, such as restructuring or during a period of broader market downturn. Imagine a CEO having his stock options awards tied to a certain ROE and cash flow generation. An impairment in goodwill, even if not a great PR, will get him closer to his financial targets!

In 2016, ConocoPhillips strategically impaired $9.3 billion of goodwill during a period of low oil prices. This allowed the company to recognize the loss during a time when the industry as a whole was struggling, potentially masking underlying performance issues.

Counter-example: Some companies might delay goodwill impairment to avoid the appearance of weakness, potentially leading to questions about the accuracy and integrity of their financial reporting.

The way goodwill is treated on financial statements can offer a window into management's decisions, assumptions, and strategic planning. Accounting for goodwill involves significant judgment and assumptions, and the way it is managed can indicate the management's perspective on the long-term value of acquired assets.

The presence or absence of goodwill impairment might indicate potential issues or discrepancies within management's actions. A failure to impair goodwill when conditions warrant can be a sign of over-optimism or even an attempt to artificially inflate the company's financial position.

Examining Goodwill Through Annual Reports

There's no clear structure for how companies must present their impairment tests in the annual report, so each one does as it pleases. Most don't provide any information about the assumptions they make, and those that do probably expect no one to read it. Next, we will explore what three companies report and the insights we can glean from their comments.

Case Study 1 - Nagarro ($NA9)

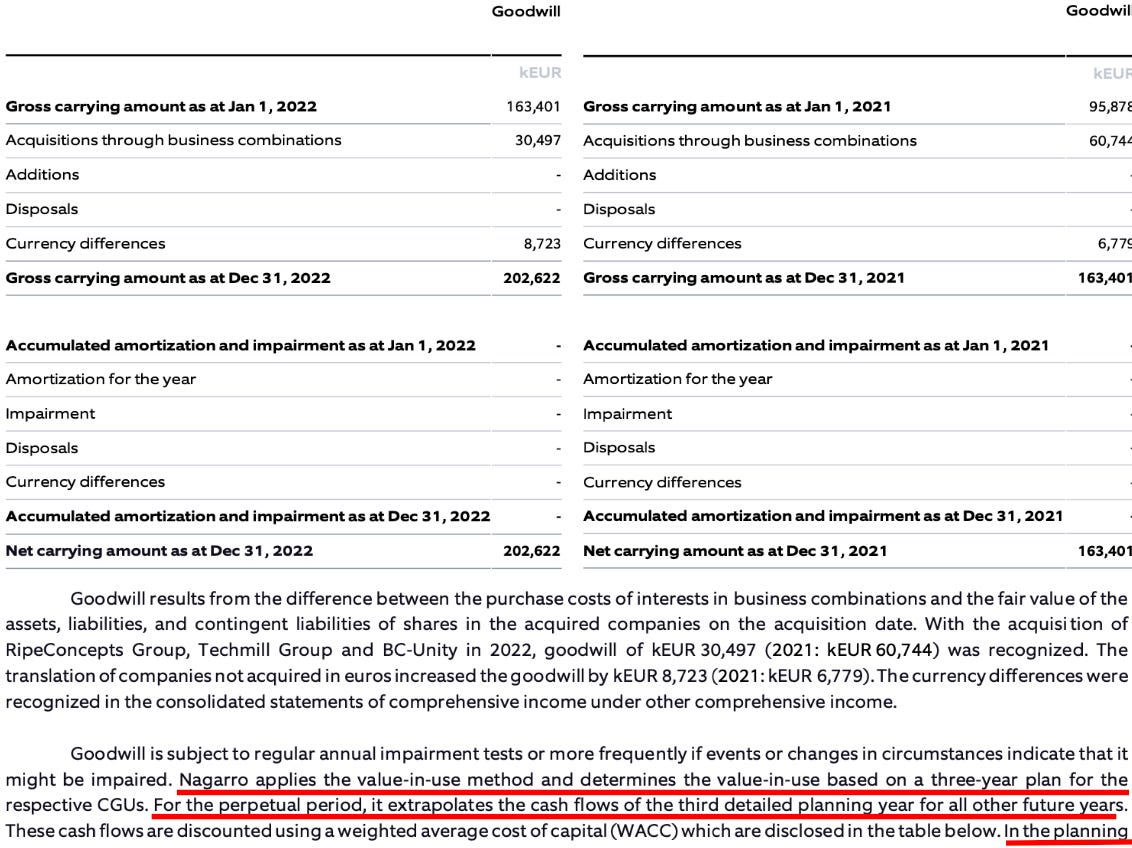

Nagarro is a German/Indian company providing digital engineering services. The company lived strong tail-winds after the pandemic, leading to high levels of organic growth, but also a series of not so cheap acquisitions. In its annual report, the company discloses its goodwill impairment test:

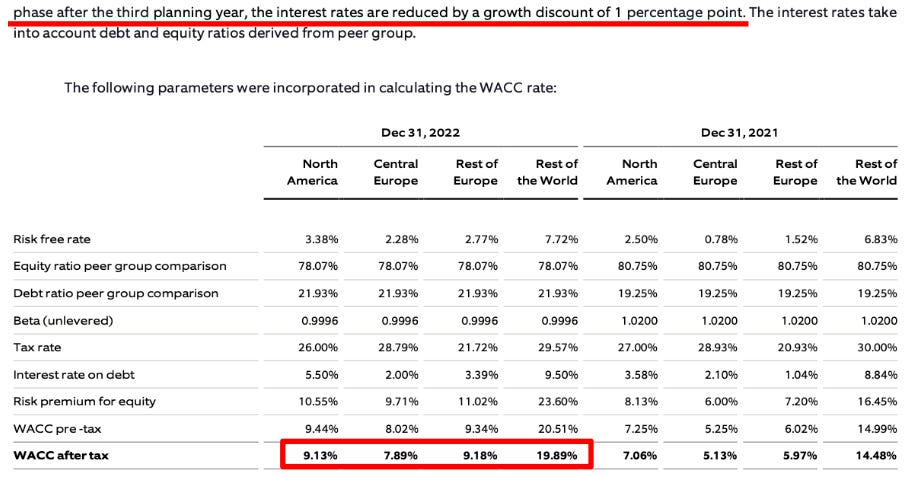

Never forget: the WACC is also the opportunity cost of your capital for these investments… Does it make sense to discount a European company at a lower discount rate than a similar one in the US, independently of the central banks’ interest rates? Food for thought.

With these assumptions, no wonder the value in use (the present value of future cash flows) is higher than their book value. I leave all of you to draw your own interpretation of the assumptions taken and if you would model the value of any of your companies the same way.

With the growth slowdown this year and the rise in interest rates, it will be very interesting to see what emerges from the new impairment test and whether management maintains their assumptions. This could give us a clear reflection of their transparency.

Case Study 2 - JTC plc ($JTC)

JTC plc is a company providing services to corporations, investment funds and family offices focused on the setup, administration, servicing, and winding up of legal structures.

In this case, the company has been acquiring smaller companies as part of its strategy to consolidate a fragmented industry. Management reports each of the company’s acquired business with the respective goodwill, and they detail quite specific the assumptions they do. Note one of the largest acquisitions, SALI, accounting for almost 40% of their goodwill:

As you can see, the carrying value of goodwill for SALI is justified by a 10 years expected CAGR of 17.2% and later, a terminal value growth rate of 4%…

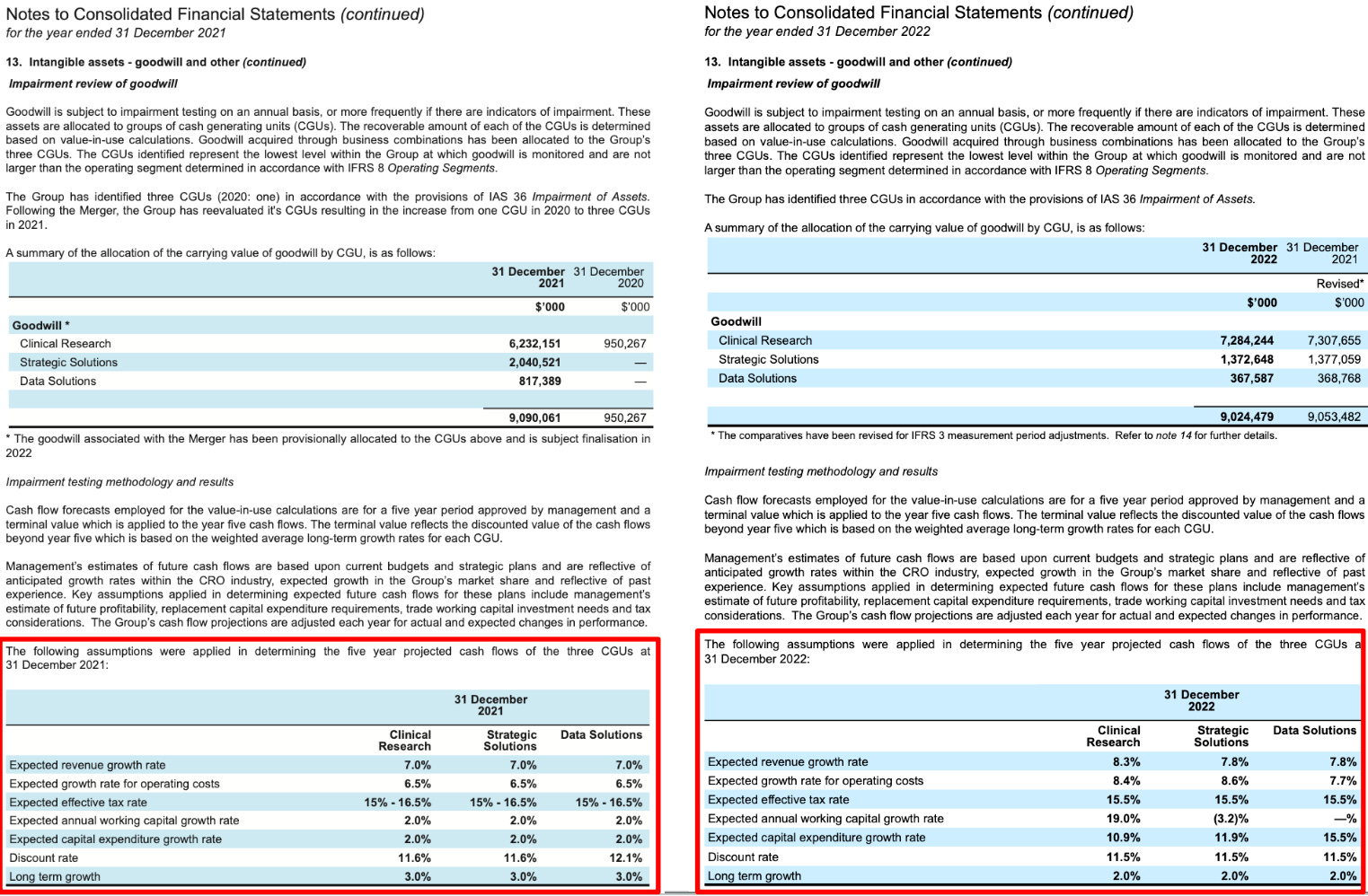

Case Study 3 - ICON plc (ICLR 0.00%↑)

ICON plc is one of the largest clinical research organization (CRO). What I found interesting about this case was comparing the assumptions they did at the end of 2021 and the ones in 2022:

There could be many things to comment on here because there are some astonishing changes in the estimations, but note: one might think it makes sense for companies to use a higher discount rate in the current interest rate environment. However, in this goodwill impairment test, it has surprisingly decreased.

Goodwill is like the hidden narrative in a company's financial story. It may seem abstract or complex, but its proper examination can lead to profound insights. Whether it's a clue to management's confidence or a warning sign of underlying problems, goodwill is a key player in the complex game of business valuation and analysis.

Remember, in finance, as in life, a holistic perspective is often the key to understanding. Goodwill is just another arrow in our quiver, highlighting the importance of considering all facets of a company's financial landscape when making investment decisions.

If you enjoyed this piece, please give it a like and share!

Thanks for reading Edelweiss Capital Research! Subscribe for free to receive new posts and support our work.

Subscribed

If you want to stay in touch with more frequent economic/investing-related content, give us a follow on Twitter @Edelweiss_Cap. We are happy to receive suggestions on how we can improve our work.

Very good insight into the concept of goodwill and accounting practices. I wonder if you integrate goodwill analysis for a quantitative estimate of intrinsic value or simply as a matter of evaluating the quality of the management team over time. I look forward to your next post already :)