#55 Building blocks of corporate accounting: operating leases and stock based compensation

#55 Building blocks of corporate accounting: operating leases and stock based compensation

How overlooking key aspects of Alphabet's and Wickes Group's financials can skew company valuations

Numbers tell compelling stories. “Company X at a mere 6x P/E”, “Company Y boasting a 15% FCF yield” – so simple, so captivating. However, the true narrative often lies beneath the surface, hidden within the complex accounting practices that shape these numbers. Most of these low PE companies come along heavy debt burdens than most people forget to mention. Remember, not all that glitters is gold.

This is a new series where we intend to enter in some accounting topics that escape from the day to day simplistic analyses that we face out there. We delve today into two simple, yet frequently overlooked, aspects of accounting: operating leases and stock-based compensation.

Welcome to Edelweiss Capital Research! If you are new here, join us to receive investment analyses, economic pills, and investing frameworks by subscribing below:

Operating leases and stock base compensation (SBC), although seemingly innocuous, can have profound effects on a company's reported financials and, consequently, its valuation. The changes brought about by the International Financial Reporting Standard 16 (IFRS 16) transformed the way companies account for operating leases, while stock-based compensation, though not a direct cash cost, is a real expense borne by shareholders through dilution.

Through the lens of two case studies - Wickes Group's operating leases and Alphabet's stock-based compensation - we will explore how these accounting practices impact financial statements and the potential valuation errors that can arise if they are not considered.

Operating Leases

Operating leases are contractual agreements allowing the use of an asset for a certain period without the responsibilities of ownership. For the lessee, these leases are akin to a rental agreement. Payments were typically classified as operating expenses on the income statement rather than being represented on the balance sheet, making the company's long-term obligations less apparent.

However, the landscape of lease accounting experienced a significant shift with the introduction of the International Financial Reporting Standard 16 (IFRS 16) in January 2019. Under this new standard, companies are required to recognize most leases on their balance sheets, bringing a greater level of transparency to their financial commitments. This means that assets and liabilities related to operating leases now appear on the balance sheet, which can substantially impact a company's financial ratios and overall financial health.

Case Study: Wickes Group's Operating Leases

Let's consider the case of Wickes Group, a British home improvement retailer. Like many companies in the retail sector, Wickes Group leases most of its store locations. Before the adoption of IFRS 16, these leases would not have been directly visible on the balance sheet, and they would only represent an operating expense in the Income Statement. However, with the implementation of IFRS 16, Wickes Group had to incorporate these leases into its balance sheet accounting, leading to a significant increase in reported assets and corresponding liabilities. The entry in the Income Statement is no longer an operating expense, but a depreciation expense. The cash flow statements have also been affected. Previously, operating leases didn't appear anywhere, but what happens now is that this depreciation expense is added to calculate the operating cash flow, and then it is deducted in the cash flow from financing.

This shift has profound implications for how we understand and evaluate Wickes Group's financial performance. For instance, the increase in recorded assets and liabilities may initially alarm investors due to the perceived increase in financial risk. Additionally, it might seem the company needs additional capital to drive returns, decreasing the return on invested capital.

Moreover, certain financial ratios that investors use to assess a company's current valuation could be significantly altered, and a superficial evaluation might lead to misinterpretation.

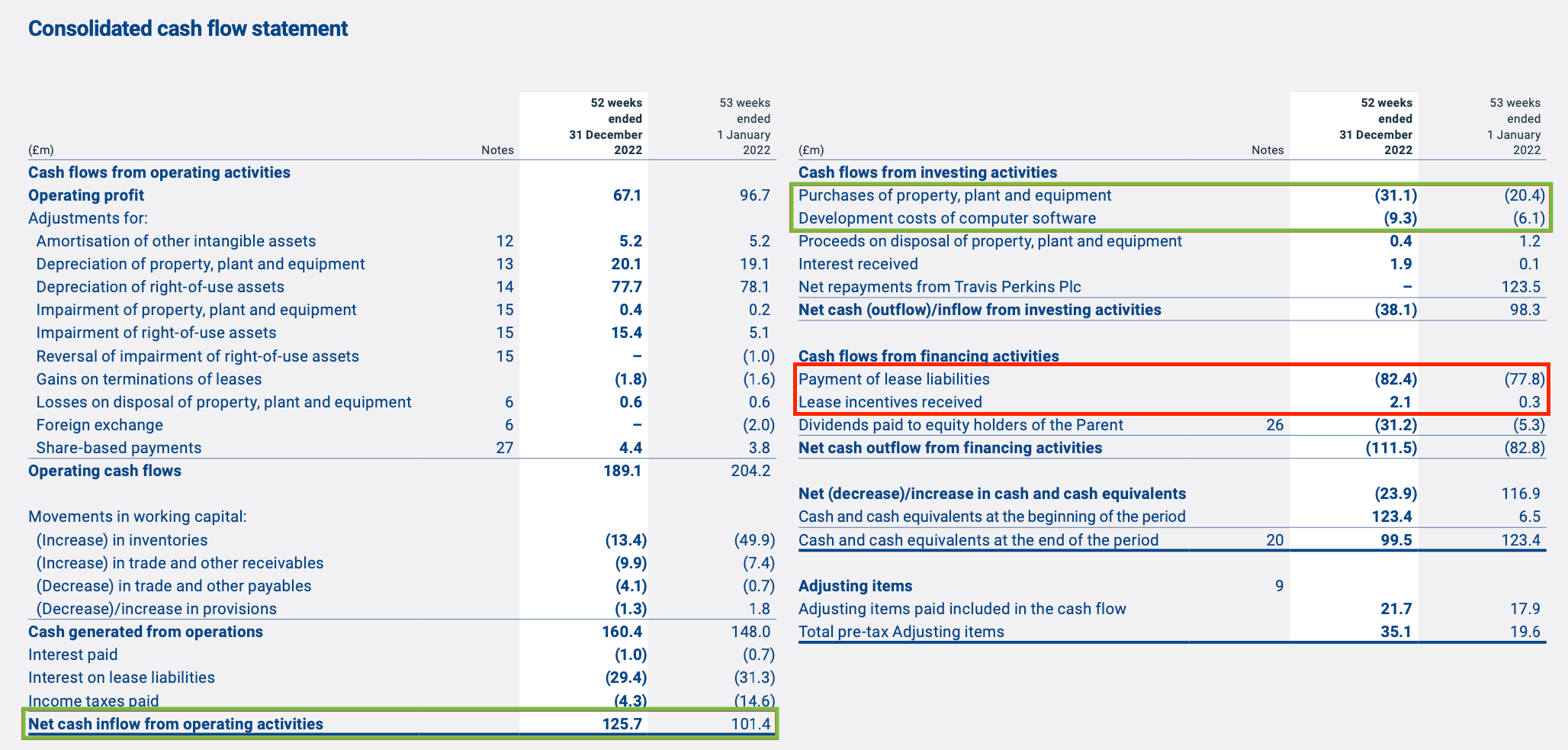

This week, we read a tweet from an investor showing the FCF yield of their portfolio. Wickes Group was in it with an FCF Yield of 17%. Wickes has a market capitalization of 333 million pounds with a net debt of about 150 million (not taking into account the lease liabilities), so the EV is around 483 million.

If we look at the Cash Flow Statement, a quick calculation of the FCF would give us 125.7-31.1-9.3=85.3 million, which would give us a 17% FCF yield. Seems pretty nice.

But know let’s look deeper. Let’s think about Wickes business model. They have all their stores leased! We can not forget to deduct theses expenses! They are operating costs!

If we do so, the FCF is reduced to 5m, which is equivalent to almost a 1% FCF….

The key takeaway here is that understanding the nuances of operating leases and the impact of IFRS 16 is essential for accurate valuation and financial analysis. Neglecting to account for this aspect can lead to a skewed perception of a company's financial standing. It underscores the importance of thorough and informed analysis when evaluating company valuations.

Stock-Based Compensation

Stock-based compensation is a way for companies to reward employees with a portion of the business instead of using cash. These rewards can be in the form of stock options, restricted stock units (RSUs), or other equity-based instruments. In essence, stock-based compensation is a form of non-cash expense that shows up on the income statement, impacting the company's reported earnings.

While it's not a direct cash cost for the company, stock-based compensation has a real impact as it dilutes the ownership of existing shareholders. When new shares are issued for stock-based compensation, the percentage of the company that each existing share represents decreases, which can affect the value of each share. Therefore, even though it doesn't drain cash from the business, it's a cost borne by the shareholders in the form of dilution.

Case Study: Alphabet's Stock-Based Compensation

Alphabet Inc., the parent company of Google, is well known for its generous use of stock-based compensation. It's a key part of their “strategy” to attract and retain top talent. While this approach has been effective in incentivizing employees and aligning their interests with those of the company, it also means that Alphabet's earnings are consistently reduced by the stock-based compensation expense reported on its income statement.

This dilution effect, coupled with the expense recognition of stock-based compensation, can lead to a significant discrepancy between Alphabet's reported earnings and its actual cash flows. In other words, Alphabet's FCF is really overstated compared to the actual FCF for shareholders (we are ignoring bondholders in this case since the capital structure is mainly equity-based).

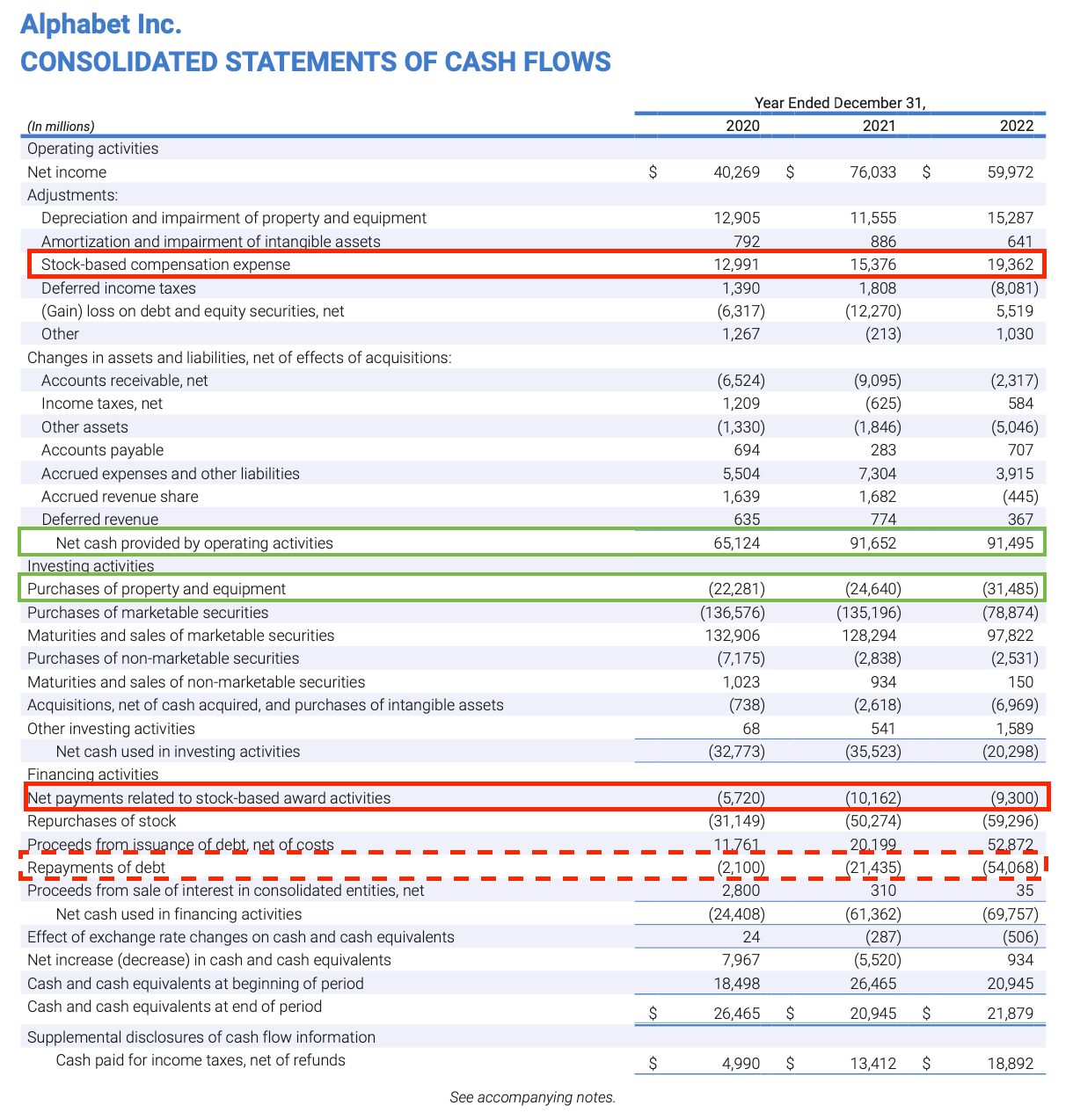

As before, a quick calculation would give us 91,495-31,485= 60 billion in FCF. With a current EV of 1.47 trillion, this would give us an EV/FCF multiple of 24.5x or a 4% FCF yield. Quite reasonable for a company of Google's quality and with plenty of room to grow.

Again, let's look at the cash flow statement in detail:

We all know that Google doesn't hold back when it comes to distributing SBC, so those whopping 19.3 billion don't scare anyone anymore.

What many people don't take into account is that line that says "Net payments related to stock-based award activities", accompanied by another nearly 10 billion. What is this??

Well, it's not disclosed but it could be:

Exercise of stock options: When employees or executives exercise their stock options, they pay the company the strike price of the options. This results in a cash inflow for the company, which would be included here.

Tax withholdings: When stock awards vest, it often results in a tax liability for the recipient, as the value of the vested awards is usually considered taxable income. Companies often withhold shares to cover this tax liability. This is known as "net share settlement". The company pays the tax authority on behalf of the employee and deducts the number of shares used to cover this tax liability from the total number of shares that were supposed to vest. The cash paid to the tax authority would be part of the "net payments related to stock-based award activities".

Repurchase of stock: Sometimes, companies repurchase stock from employees. The cash paid to repurchase the stock would also be included here.

Payments for stock-based compensation awards that are liability-classified: Some stock-based awards are classified as liabilities rather than equity. For these awards, the company recognizes an expense over the vesting period and also records a liability. When the award is finally paid out (often in cash), it results in a cash outflow.

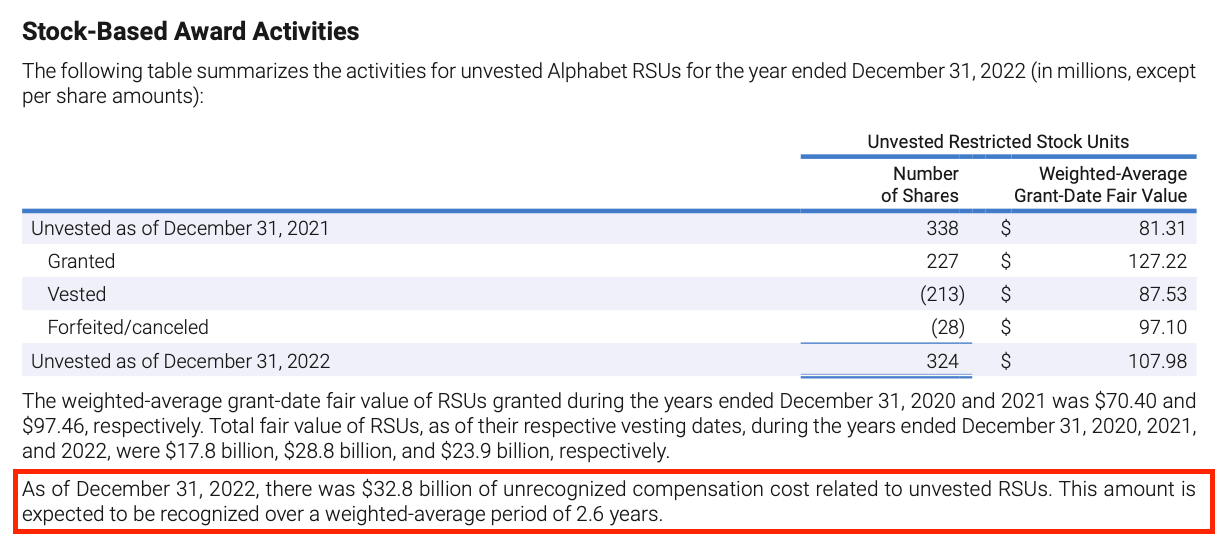

Also consider that there was $32.8 billion of unrecognized compensation cost related to unvested RSUs.

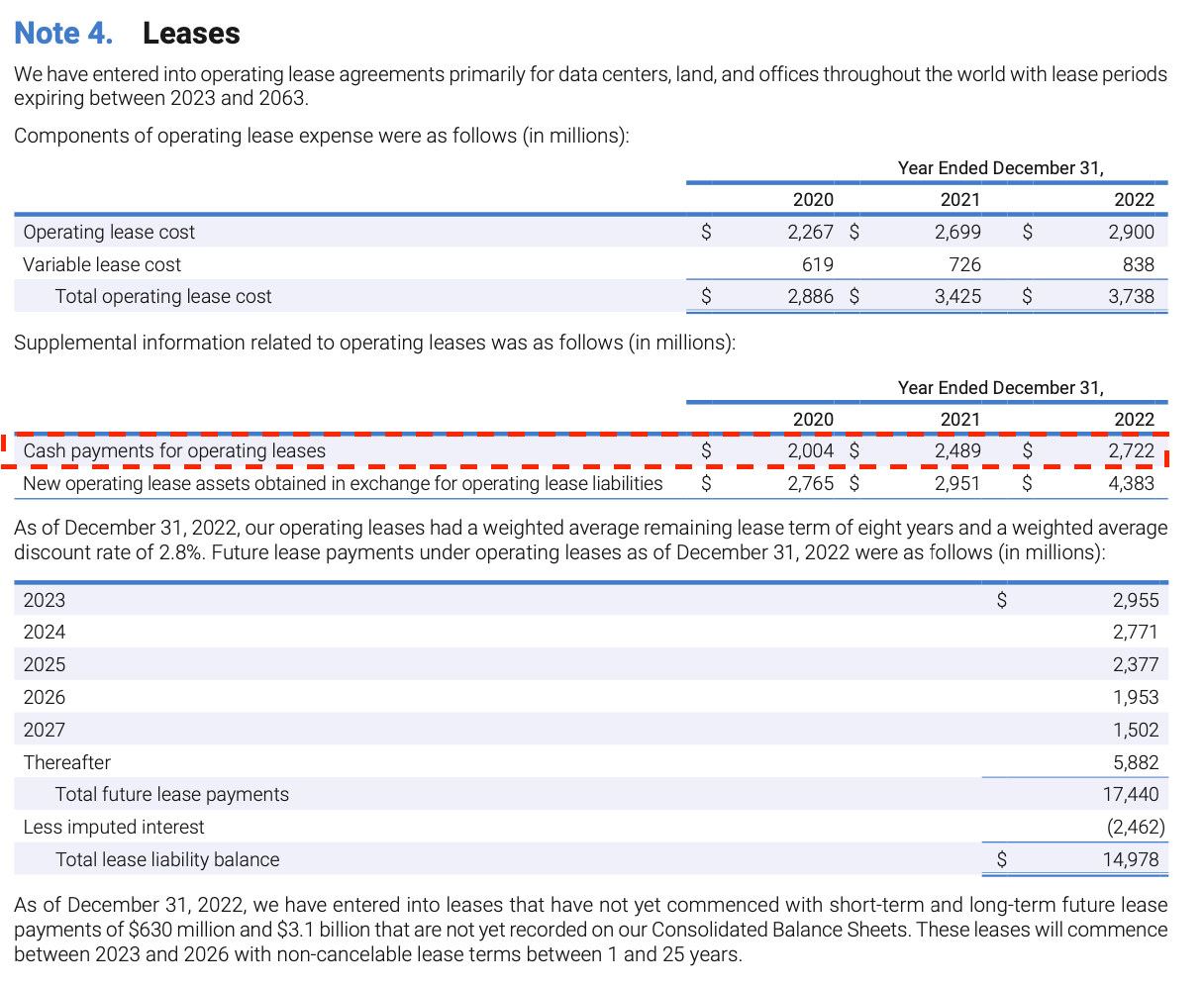

Finally, Alphabet has its operating leases that we have to deduct

All in all, we transition from an EV/FCF multiple of 24.5x to 51x, or basically halving the real FCF to shareholders… 28.6 billion FCF.

Concluding remarks

The devil is often in the details. The case studies of Alphabet and Wickes Group illustrate how seemingly nuanced accounting aspects like stock-based compensation and operating leases can have a profound impact on a company's reported financials and, consequently, its valuation.

As investors and financial analysts, it is incumbent upon us to delve beyond the surface-level numbers. A company's headline figures may tell one story, but a deeper understanding of the accounting practices behind them can often reveal a different narrative. By considering these elements in our analysis, we can derive a more accurate and comprehensive view of a company's financial standing and valuation.

Remember, in finance, as in life, a holistic perspective is often the key to understanding. Whether we're assessing the impact of stock-based compensation at Alphabet or the influence of operating lease accounting at Wickes Group, these cases reaffirm the importance of considering all facets of a company's financial landscape when making investment decisions.

If you enjoyed this piece, please give it a like and share!

Thanks for reading Edelweiss Capital Research! Subscribe for free to receive new posts and support our work.

If you want to stay in touch with more frequent economic/investing-related content, give us a follow on Twitter @Edelweiss_Cap. We are happy to receive suggestions on how we can improve our work.

SBC continues to be one of the most contentious points of conversation amongst the investment community - I don't see that changing. Something I've found helpful is to always approach evaluating companies both on a firm-level and equity-level. As far as I can tell, ensuring normalized numerators and denominators (FCFF/EV vs FCFE/MC, etc) and mapping out funding mechanics along with continued operations is the only way to tell what's what. Too often equity investors forget where they sit in the capital stack.

Great article, thank you