#23 Google: the modern 5th Avenue Real Estate

#23 Google: the modern 5th Avenue Real Estate

Google was launched in 1998 by Larry Page and Sergey Brin, at the time, Ph.D. students at Stanford. Thanks to Google, we were all able to make the internet something accessible, useful, and productive. Google leveraged the internet revolution

Nowadays, everyone realizes Alphabet is one of the best businesses out there. There is no doubt about it. However, the multiples at which the shares are priced in the last months are assigning one of the lowest valuation multiples ever.

Welcome to Edelweiss Capital Research! If you are new here, join us to receive investment analyses in 10 slides, economic pills, and investing frameworks by subscribing below:

The brand became verb

Ads business is Alphabet’s crown jewel. If digital ads companies are equivalent to commercial real estate in the digital world, Google is the 5th avenue. When a product becomes a generic name, it shows a nice brand moat. But there is a special place in moat Olympus reserved for products that became verbs.

Google has shown good resistance to the current macroeconomic uncertainty environment with steady growth, while others have struggled. Meta reported in Q2 a revenue decrease and a 14% lower price per ad. It shows that Google has a predominant role thanks to its position in the customer journey and has been less affected by the regulatory and privacy changes and by the competition from TikTok.

The Digital Ads market is expected to continue growing at 11% CAGR over the next 5 years (Cramer-Flood, 2022a). Google has shown to be well positioned to continue as the market leader in a likely oligopolistic scenario with wide moats and strong margins (Cramer-Flood, 2022b). This gives Alphabet an incredible cash-generating machine and makes it one of the best businesses in the world. However, and despite some price increases, this is far from the growth in the past decade. Also, Google has suffered in the last years a continuous erosion of its market share (Cramer-Flood, 2022c). This year seems to be an exception to the decline, which is good news. But the competition grows strong (Amazon, TikTok) and we consider that maintaining the current market share shall be considered in an optimistic scenario. Alphabet needs to find a new growth tractor to become less dependent on the search engine.

An unfair advantage

Youtube could be a stand-alone business worth billions (Mann, 2022). Premium subscribers reached 50 million (YouTube, 2021) by the end of 2021. Even if this figure is still small compared to the 220m of Netflix or the 150 of Disney+, we consider YouTube's business model superior to other traditional video-on-demand services. Applying our economic framework (Edelweiss Capital, 2022), in the long term, we believe thousands of independent creators experimenting with content have a much higher capability of determining the right content for each consumer. Furthermore, the micro-segmentation achieved by Youtube (any niche you can think of has professional YouTubers making content for a living) is never going to be possible by a central organization deciding content with the high costs and risks associated with traditional productions. YouTube’s remuneration policy (55% of revenue for creators) might make the aggregated content more expensive than Netflix. But almost 100% of the risk is transferred to the creators and leaves the company in a mere platform position with the consequent low capital requirements and high margins.

Despite the recent deceleration in growth, we do believe YouTube has enormous potential yet. But this is just half the story. YouTube decided to enter the intense competition of the short-video format and compete for face to face with TikTok, which is expected to have explosive growth in 2022 (Cramer-Flood, 2022b). TikTok, not Netflix, is the current real threat to YouTube’s business as a growth machine.

Scale, scale, scale

The global cloud market growth is still strong and the potential future size could be unbounded. The competitive advantages provided by the economies of scale and the monumental investments in infrastructure necessary to the reach the required size will probably limit the number of competitors to a handful. Furthermore, the high switching costs associated with platform migration make it more difficult to increase market share as it matures. In the mid-term, we will likely reach an oligopolistic status. Not the Airbus-Boeing kind, where even having granted duopoly and full backlogs for the next decade, they still struggle to be profitable. We talk about the good kind of oligopoly where participants understand that they will be competing against each other for decades to come. That understanding leads to healthy competitive behavior rather than mutual destructive maneuvering. Google knows this. Even though it arrived a little bit late, and erratically, to the cloud party, it has been gaining market share consistently. Not as strongly as Azure, but it is a merit of Microsoft corporate network rather than a miss execution from Alphabet.

But let's not be condescending, the operating margins have been disappointing at their best. Google Cloud has not been able to be profitable after many years in the market and it is burning cash at a substantial rate. However, at this point, we believe this is a necessary strategy to earn its place on the winner's podium and Google should be able to switch on the profit machine eventually. However, the management needs to show that it is capable of doing so. And we, as long-term investors, need to monitor them carefully as one of the key points in the next few years.

The productivity revolution

Other Bets include some of the more risky ventures from Alphabet, such as Waymo or DeepMind. This segment is the black sheep of the Alphabet family due to the high level of cash invested without returns over the last years. In our opinion, the optionality given by these investments in different key future technologies is worth the risk. More importantly, some of these technologies developed have clear synergies with Google's core business. For instance, DeepMind AI technology is applied mostly to Alphabet products, and the latest annual report (Deepmind, 2020) available showed a 212% growth in revenue (£826 million in 2020) and the first profits in its history.

AI is bringing a new productivity revolution comparable in magnitude to the computer or internet ones. That is the reason why technology companies have been investing heavily for years. If Other Bets allows Alphabet to be well positioned to have a leading role in it, we think it was a good investment. Most of the bets will fail, but if only a few of them are the right moonshot, they will make for the others. Valuing this part of Alphabet with a reasonable level of certainty is an impossible task, but as long as cash spent is within a reasonable level and distributed in different areas we are happy as shareholders. No doubt it is a more antifragile approach than Zuck’s multiverse all-in.

It is remarkable to see how huge companies such as Google, Amazon, or Meta are definitely committed to avoiding falling into the innovator's dilemma (Christensen, 1997). They might be the first companies in history to cannibalize their own products to seek long-term survival. The innovation spirit is well engraved in these companies and they keep maintaining small, nimble divisions that attempt to serve low-value customers with poorly developed technologies. By doing that, they can improve the technology incrementally until it is good enough to quickly take market share from old established businesses or just create new markets. This, together with the talent attraction of the brand, makes it possible to create and sustain a long-term competitive advantage.

Mixed feelings about Sundar

Google is not a conventional company, nor is its CEO. Sundar Pichai became CEO of Alphabet in 2019. Even if he was Google’s since 2015, it seems fair to hold him accountable since becoming the big boss. And looking at the numbers, he has done an outstanding job. After many years with the ROIC cruising around 12%, in 2021 and 2022, the values have spiked above 20%. This has been supported by the exceptionally good year 2021, “thanks” to the COVID pandemic. It has still to be proven whether they can maintain these superb numbers in the long run, or it was only a mirage. But credit where credit is due as of today.

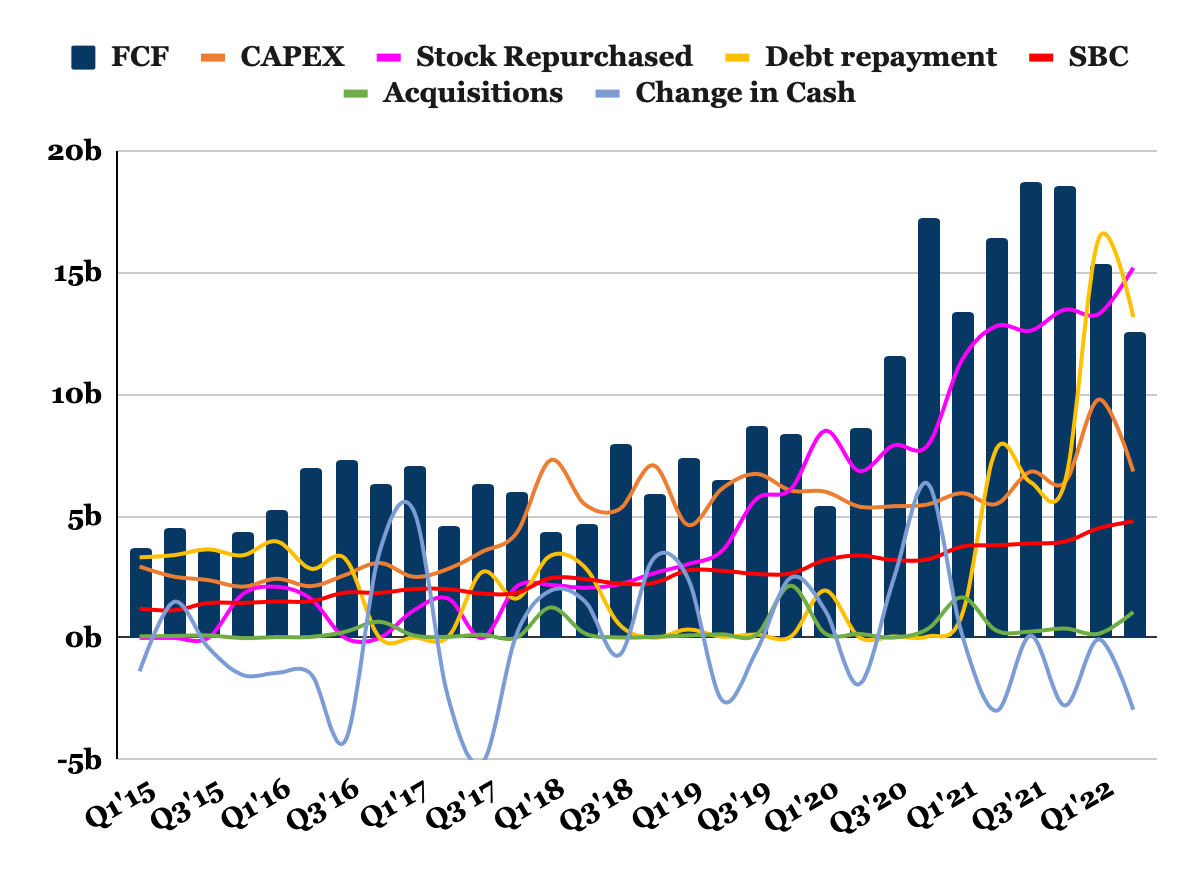

A detailed capital allocation analysis has been also impacted by the pandemic tailwind for Google. But there are a couple of considerations worth mentioning. We are normally quite critical of share buyback programs. Especially if they are done under the rationale of avoiding shareholder dilution from employees/executives’ stock-based compensation programs.

If you take a look at the graph below, you will see only 2 times where share repurchases have been higher than FCF: the pandemic sell-off and the last quarter. Both coincide with what we believe are heavily undervalued prices and hence, an appropriate long-term shareholder value creation, especially if we consider an incredibly healthy balance sheet with a negative net total debt. It is also remarkable to see how CAPEX has remained quite stable in the last 4 years despite FCF having almost doubled.

For all this, Sundar is paid a base salary of $2m. Quite surprising for one of the biggest companies in the world. Furthermore, Sundar has rejected any further stock award (although in the past he received large amounts of stocks and still has almost 300m in unearned unvested stock).

For the rest of the executives, performance stock awards are based on the total shareholder return to reward significant positive outperformance of Alphabet relative to the companies comprising the S&P100. But surprise surprise, they get 100% of the stock compensation just by achieving the percentile 50 and will get a 200% by achieving the 75th. This shareholder incentive misalignment is added to some others where executives’ values and beliefs are mixed with business performance and value creation for the shareholders (D’Onfro, 2018), (Lipton, 2018) and (Broole, 2022).

We have some concerns related to the increase in the number of employees (currently 174k) and its impact on the operating margins. The substantial growth in headcount (+21% YoY) in an already tense job market, implies a high growth in operating expenses (+24% YoY), with stock-based compensation growing to an unsustainable 6.9% of the revenues. We believe in the power of incentives and the inclusion of the employees in the long-term success of the company, but shares must be held as the most precious item and cannot become candy to give away easily. We hope Sundar’s recent words make an impact (Hostspot News, 2022).

Clouds on the horizon?

One of the biggest risks Alphabet is facing is the regulatory one. There have been rumors that the DOJ is preparing a second lawsuit due to its domination of the search market in violation of antitrust laws. There are 2 types of monopolies, those granted by the state via coercive actions, which are terrible, and the ones naturally occurring in a free market and conceded by the consumer. Since consumers always retain the capability of revoking the “privilege” of monopoly, they are fair. The market establishes the mechanisms (via good margins) for other companies to innovate and challenge the status quo. But of course, the states do not share this vision and we should not neglect the damage they could create to the shareholder.

Independently, the real threat is new players with access to massive data entering into the profitable ads business, such as Apple (O’Reilly, 2022), or a change in consumers’ habits if ever a better tool becomes available. According to a Google senior exec, almost 40% of young people search on TikTok or Instagram for stuff like restaurants (Perez, 2022). TikTok’s ad revenue tripled in 2022, and some forecasts predict that it will reach YouTube’s 2022 revenue levels as soon as 2024 (Lebow, 2022). Of course, this is a prediction and as such, the numbers have to be taken with a grain of salt. But it will definitely be one of the bigger (if not the biggest) challenges in the following years.

Show me the money

The market considers the growth Alphabet has shown in the past to be at risk for the next years due to the factors presented. This can partly explain the low current multiples for such an exceptional growing and quality company. We still believe the quality of the business overgrows the risks. We are also confident the management will be able to execute new revenue streams to foster future value creation. But that is not enough, so let's take a look at possible conservative future scenarios.

Valuing a company with the model below (or with any model forecasting the future) is a good measure to understand the ballpark we are playing in. But do not take the numbers as a holy figure. Correctly predicting our expenses 5 years from now would be a mere coincidence. That does not mean it is not a useful tool. It is, if used correctly.

We are quite confident investing in Google at the current prices. We believe in the long-term competitive advantages of the business. Even if we consider a conservative fair price at current levels, we keep all the associated optionality as a margin of safety.

If you enjoyed this piece, please give it a like and share!

Thanks for reading Edelweiss Capital Research! Subscribe for free to receive new posts and support our work.

If you want to stay in touch with more frequent economic/investing-related content, give us a follow on Twitter @Edelweiss_Cap. We are happy to receive suggestions on how we can improve our work.

Disclosure: We have and intend to add Google shares in the near future. Everything expressed here is only our opinion. Always do your own research.

Victor Peña & JPA

References

Alphabet (2022). Quarterly and annual reports. Link

Broole, C. (2022). Google goes woke! Search engine launches 'inclusive language' function to cut down on politically incorrect words. The Daily Mail. Apr 25, 2022. Link

Christensen, C. (1997). The Innovator's Dilemma: When New Technologies Cause Great Firms to Fail. Harvard Business Review Press

Cramer-Flood, E. (2022a). Worldwide Ad Spending 2022: A Surge in Latin America, a Stumble in China, a Milestone for Mobile, and a First for ByteDance. Insiders Intelligence. May 18, 2022. Link

Cramer-Flood, E. (2022b). ByteDance expands the ranks of duopoly challengers. Insiders Intelligence. May 19, 2022. Link

Cramer-Flood, E. (2022c). Duopoly still rules the global digital ad market, but Alibaba and Amazon are on the prowl. Insiders Intelligence. May 10, 2022. Link

Edelweiss Capital, (2022). #17 An economic framework for investing: the Austrian School. Link

Deepmind Technologies Limited, (2020). Directors’ report and financial statements. Dec 31, 2020. Link

D’Onfro, J. (2018). Google will not renew controversial Pentagon contract, cloud leader Diane Greene tells employees. CNBC. Jun 1, 2018. Link

Hostspot News, (2022). The CEO of Google issues a warning about low productivity and encourages employees to make up the difference. Aug 4, 2022. Link

Lebow, S. (2022) TikTok and Douyin will account for more than 5% of global digital ad spend this year. Insider Intelligence. Apr 13, 2022. Link

Lipton, J. (2018) Google won’t pursue $10 billion Pentagon cloud contract. CNBC. Oct 8, 2018. Link

Mann, H. (2022). How Much is YouTube Worth? Over US$180bn in 2022. Startup Strategy Jul 29, 2022. Link

O’Reilly, (2022). Apple is rolling out new ads that could grow its booming ad division by $1billion a year. Business Insider. Link

Perez, S. (2022). Google exec suggests Instagram and TikTok are eating into Google’s core products, Search and Maps. Tech Crunch. Jul 2, 2022. Link

YouTube, (2021). 50 million. Sep 2, 2021.YouTube Official Blog. Link

Very instructive, like all your work. Thanks!