#4 Incentives, innovation & management

#4 Incentives, innovation & management

Traces to identify "outsider" CEOs and why some companies perform better than others in the long term

In this article, we explore the relationship between innovation, incentives, and management teams, and why some companies are destined to have better long-term returns than others.

Innovation is the internal engine to deliver organic and sustainable growth in companies, but there are several problems in aligning top management with shareholder’s interests, specially if shareholders differ in their time-preferences.

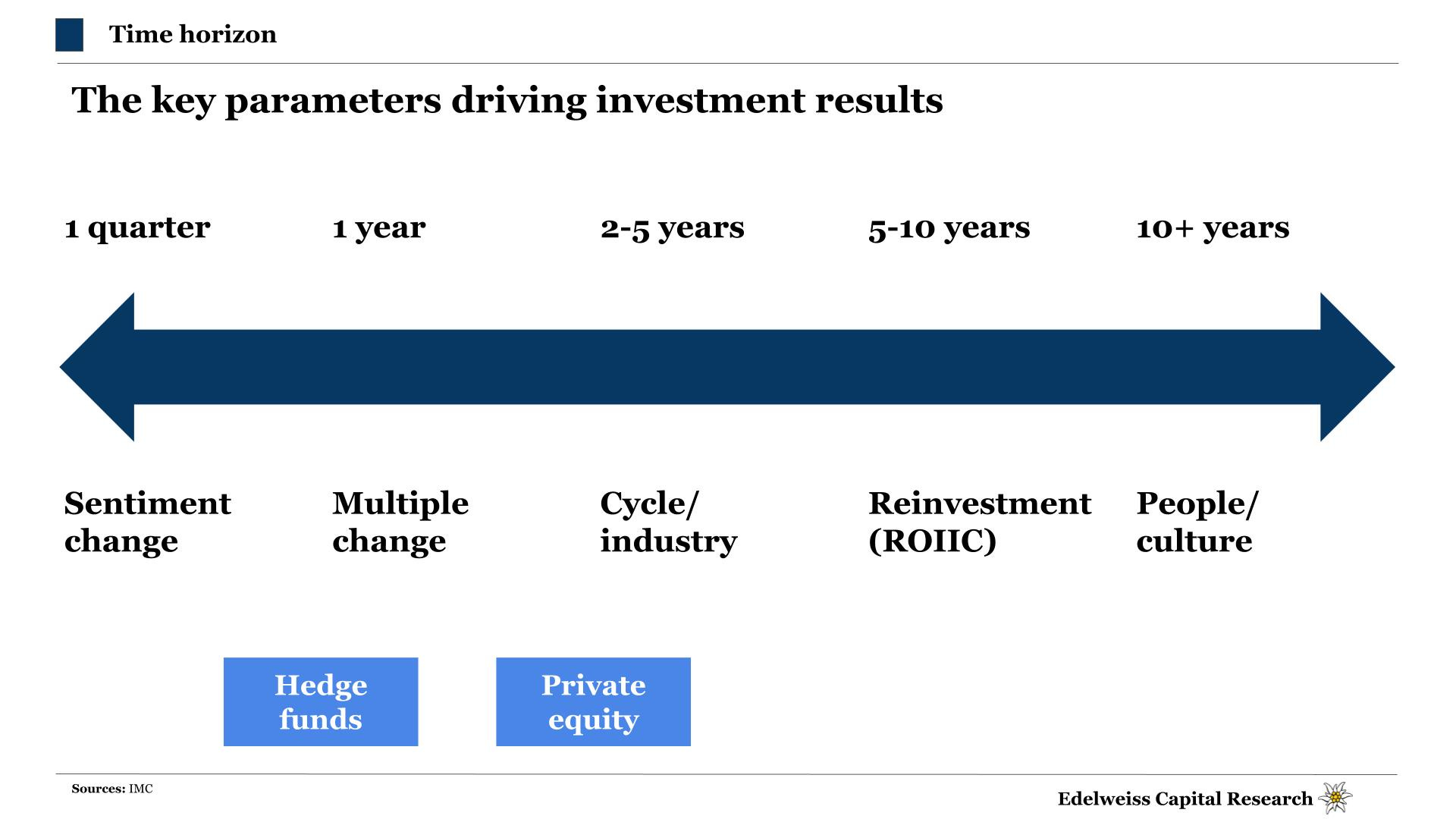

CEOs are key in the future of their company and mainly because they must carry the most important mission, which is to allocate the cash flow generated by the company's operations. CEOs have five essential choices for deploying capital and three alternatives for raising it.

Finally, we review why Mark Leonard and Constellation Software are the best paradigm of how a company's culture leads the way and leave traces for outstanding long-term results.

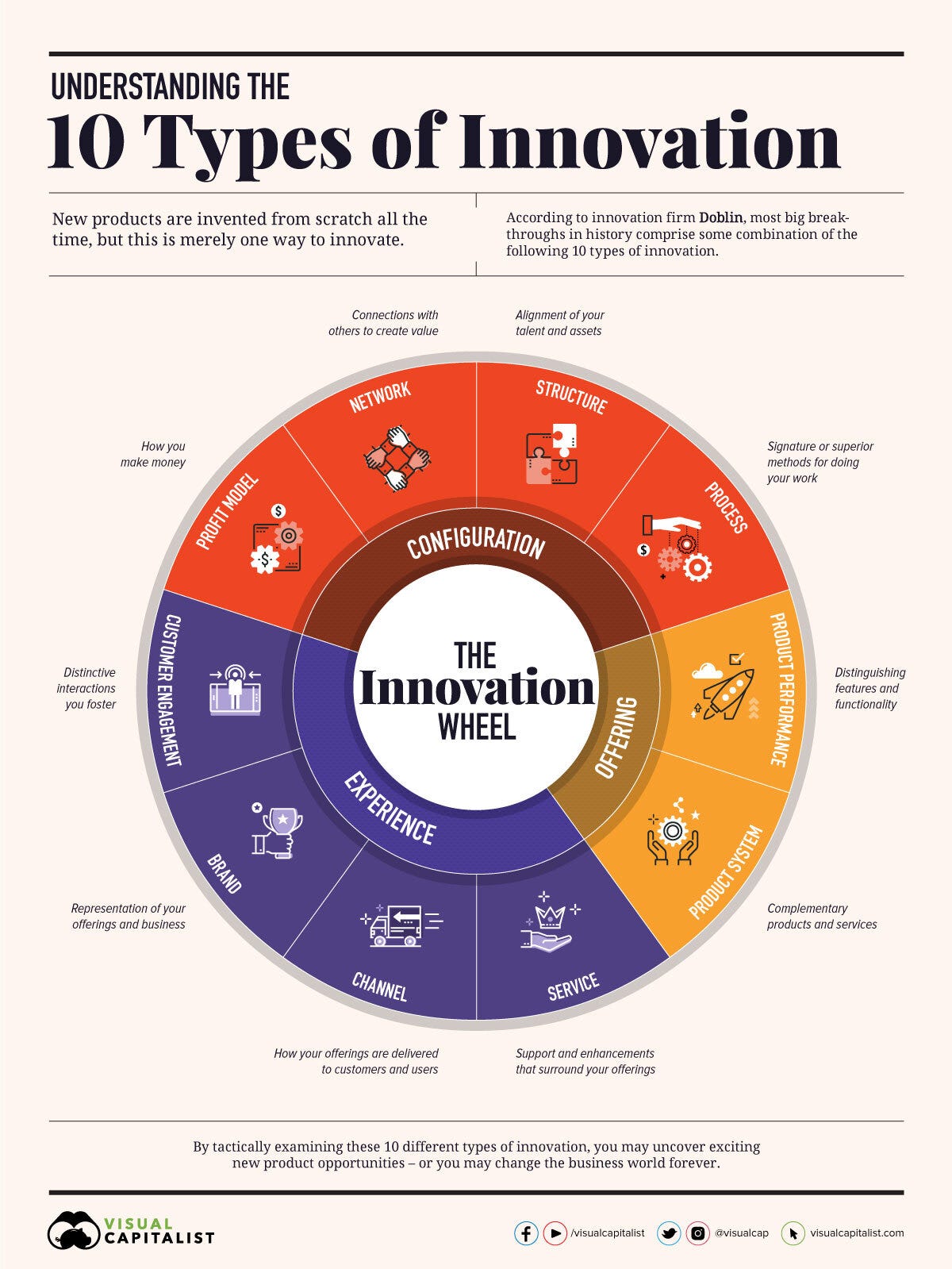

Innovation to obtain competitive advantages

Innovation is nothing more than the process by which companies seek to achieve competitive advantages in the long term (Greenwald and Kahn, 2007). In other words, innovation is necessary to "ensure" the future success of a company. However, it is harder to define how to innovate. When you ask this question in a general group, the answers you get most of the time are related to technological developments and new functionalities. This is a very limited view, a tiny part of the universe that makes up the wheel of innovation. Innovation reaches also the increase of brand perception Patagonia has achieved with its environmental activism or the ecosystem that Apple has created with the seamless integration between all its products. Zara’s supply chain and logistics network revolution ended with the industry standard of designing collections semesters in advance. They were capable to decrease the product development cycle to just 2 weeks (from design phase to having the clothes in the stores), and that has given them a competitive advantage that its competitors have not yet been able to match years later (D'Andrea and Arnold, 2003). That is the true ultimate goal of innovation. All these different types of innovation do nothing but seek organic and sustainable growth in companies (Keeley et al., 2013).

Different time preferences, different incentives

The conflict of interest between shareholders of a publicly owned corporation and the company’s chief executive officer (CEO) is a classic example of a principal-agent problem. Shareholders want CEOs to take particular actions—for example, deciding which issue to work on, which project to pursue, and which to drop—whenever the expected return on the action exceeds the expected costs (positive net present value). But the CEO compares only his private gain and cost from pursuing a particular activity. If one abstracts from the effects of CEO risk aversion, compensation policy that ties the CEO’s welfare to shareholder wealth helps align the private and social costs and benefits of alternative actions and thus provides incentives for CEOs to take appropriate actions. Shareholder wealth is affected by many factors in addition to the CEO, including actions of other executives and employees, demand and supply conditions, and public policy (Jensen and Murphy, 1990). It is appropriate, however, to pay CEOs on the basis of shareholder wealth since that is the objective of shareholders.

Despite the need of raising capital in public markets acts as the correct incentive for publicly traded companies to offer more transparent accounting results (Burgstahler et al., 2004), management executives are often focused on immediate results, especially when the incentives under which they are evaluated and remunerated are not the correct ones. Firms where the CEO’s compensation is closely tied to the value of stock and therefore, the earning line, will incentivize him to legally manipulate the numbers so he achieves his bottom-line goals, even if for that he has to reduce operational cost this year, maximizing the earnings this year, but patronizing the future growth potential of the company in the future (Bergstresser and Philippon, 2006). Similar incentives apply when managers strategically choose the precision of their earnings forecasts for self-serving purposes with insider purchases or sales (Cheng et al., 2013).

The problem of aligning top management with shareholders arises, first of all, if shareholders differ in their time-preferences. It is impossible to find a contract that fully aligns manager interests with those of both long-term and short-term shareholders. This misalignment of interests makes it very difficult to align the incentives correctly, and makes the managers' contracts cover both short and long aspects and, therefore, have repercussions in poor results and destruction of value (Chidambaran et al., 2019).

CEO: the key role

It is surprising how many people buy stocks without checking and analyzing the executive suite. Many things have been written on how the management shall be evaluated when investing in a company. Compensation, character and performance have been considered for many great investors as 3 important areas to evaluate (Dorsey, 2004). The scope of the CEO, however, should be more constrained to be successful than it is normally. The key role of a CEO, the area where he should be expending most of the time, is to deploy the cash generated by the company operations (Thorndike, 2012). Most management books focus on managing operations, which is undeniably important, but then, why do you have a COO?

Basically, CEOs have five essential choices for deploying capital—investing in existing operations, acquiring other businesses, issuing dividends, paying down debt, or repurchasing stock—and three alternatives for raising it—tapping internal cash flow, issuing debt, or raising equity. Over the long term, returns for shareholders will be determined largely by the decisions a CEO makes in choosing which tools to use (and which to avoid) among these various options. Stated simply, two companies with identical operating results and different approaches to allocating capital will derive two very different long-term outcomes for shareholders (Pecaut and Wrenn, 2017). Essentially, capital allocation is investment and as result, all CEOs are both capital allocators and investors. This, and no other, is the key role of a CEO.

Skin in the game

Taking a look on some of the best performance companies/stocks of the last half-century, we often find an owner-operator behind it: Steve Jobs at Apple, Sam Walton at Walmart, Bill Gates at Microsoft, Warren Buffett at Berkshire Hathaway. The people running these companies were in control. When there was a drawdown like 2008, that’s precisely when they took on more debt and deployed cash. That was the moment to invest. This behavior could be compared to the agent-operated companies. They loathe spending cash or taking on debt in a highly volatile environment, because an agent-operator is so fearful about how that will be perceived by the public, the board and how it may impact his or her career prospects. They just sit frightened on mountains of cash (Mayer, 2015).

Great long-term investors such as Warren Buffet or Terry Smith have always considered the return on capital employed (ROCE) as one of the key aspects to measure the performance of the executive team. As soon as the capital returns are higher than the cost of capital, the CEO is creating value for the shareholders (Smith, 2020). Many times, the CEO decides to grow a business increasing the revenue -because it sounds better to be the CEO of a company with $10B revenue than with $500k – even if in the process the margins have been eroded and the shareholder wealth destroyed. Then, what are the commonalities among many long-term managers?

To answer the question, I am bringing here the example of the Canadian company Constellation Software. Constellation manages and builds vertical market software (“VMS”) businesses. Generally, these businesses provide mission critical software solutions that address the specific needs of customers in particular markets. Their focus on acquiring businesses with growth potential and managing them efficiently, has allowed them to generate significant cash flows and revenue growth during the past several years. It is a "Buy & Build" business model where the main engine of growth is the acquisitions they do (300 since 1995). The company has maintained a ROCE between 30-40% annualized in the last 10 years. A key aspect in the Constellation Software analysis is the management team. 2% of the company's shareholding corresponds to Mark Leonard, founder, president and chairman. His salary is $1. Besides, the remuneration policy is remarkable, being the bonus received linked to factors such as ROCE and sales growth (Constellation Software Inc, 2020). The management team must invest 75% of the bonus in Constellation shares on the open market. If they trade at high multiples, they are buying overvalued stocks. Additionally, they have to keep their shares for at least 4 years. This is the real "skin in the game" which has become fashionable and misunderstood after N.N. Taleb published his book with the same name: “We propose a global and morally mandatory heuristic that anyone involved in an action which can possibly generate harm for others, even probabilistically, should be required to be exposed to some damage, regardless of context” (Taleb and Sandis, 2014).

Mastering management incentives

As defined at the very beginning, the main goal for innovation is achieving sustainable competitive advantages, where the responsibility to drive the process to get these advantages lies on the management team. Therefore, incentives and incentivizing proper and relevant innovation is mandatory for the management team. Literature shows how the principal-agent problem has been identified by the industry for more than a century, finding examples at the beginning of the 20th century with the researchers employed by German chemical and electrical engineering firms. The firms were offering performance-related compensation schemes to their scientists and studies show how past bonuses correlate positively with current patenting (Burhop and Lübbers, 2010).

Salaries and other incentives should be adapted to the personality type. Research shows, performance-based salaries attract those employees (since the CEO is just an employee appointed by the board in name of the shareholders) who are primarily interested in their income and with tasks that are easy to evaluate and calculate. In those cases, such compensation produces good results (Frey and Osterloh, 2002). Again, we need to come back and establish the correct metrics to evaluate the performance.

Motivated management creates corporate resources that are difficult to replicate. Both extrinsic and intrinsic motivation are necessary for this development. Managing intrinsic motivation is much more demanding than managing extrinsic motivation. By its very nature, intrinsic motivation is always voluntary.

Studies show that intrinsic incentives and motivation, in the form of acknowledgement and actual implementation of the ideas of innovators, are the main factors that positively affect innovative propensity (Fontana et al., 2015). That’s like saying the CEO is or should be self-motivated to drive innovation, as the public acknowledgement and recognition will lately point at him. The main organisational characteristics that positively moderate the relation between incentives and innovative propensity are board support and stability. It becomes clearer now why CEO-founders (Jeff Bezos, Mark Zuckerberg, Elon Musk, …) never stop innovating.

Corporate leaders should create a culture that tolerates early failure and rewards long-term performance, and employees from the CEO down must be given incentives to innovate. If short- term results serve as measurements of performance, then the required reforms carry a cost. To generate good quarterly earnings, managers may avoid risk-taking and exploration—precisely the steps that can multiply long-term value. If innovation is a goal, then managers must be allowed to fail and must be given time for new methods to prove their worth. Thus, incentive plans should include options with long vesting periods and allow them to reprice if share prices fall while an innovation agenda is pursued. Managers should not lose their jobs if short-term results suffer.

It may not be easy to balance the competing demands of good governance and innovation. It increases the burden on corporate directors, who are now called on to carry out a two-pronged oversight agenda: they must make sure managers are acting in shareholders’ interests and, at the same time, create incentives for innovation. That requires them to be vigilant and patient at the same time. Nonetheless, if innovation is now the greatest challenge in the business world, then it only makes sense to give corporate managers the right incentives to break new ground (Manso, 2017).

Innovation involves more than the terms of compensation agreements and employment contracts. To encourage experimentation and risk-taking, managers must consider the culture of their organizations. Does their culture give people the time and space to carry out projects that may not produce immediate rewards?

Coming back to the previous example of Constellation Software, let me finish quoting Mark Leonard about how they set incentives for the management. After all, if a company has been so much ahead its competitors for such a long time, there has to be something to be learnt from them and their governance culture:

“Incentives need to be approximately right and perceived as fair. Once people think you are in the ballpark with incentives, it is a bunch of other things like corporate culture that keep the stars and their teams around. By culture, I'm referring to mutual respect, shared values and beliefs, trust, the joy of learning and mastering and sharing. You can't mandate that stuff. It slowly seeps into the coffee and becomes the accepted way that things are done. A bad boss can stamp out a good culture in no time.

For the 6 Operating Group ("OG") managers we have a formulaic incentive plan based on their respective OG revenues revenue growth (combined organic and acquired), and profitability (a return on capital measure). We tried to design the formula to align annual incentive compensation with the annual increase in each OG's intrinsic value. Bonuses are paid in cash, but the OG managers must then invest 75% of their after-tax incentive compensation in CSI shares that are purchased on the open market. These shares are held in trust and cannot be sold for between 3 and 10 years. We designed the hold periods and the trust to align the managers' capital appreciation with that of CSI's long-term shareholders.

All of our OG Managers have been responsible for deploying the majority of their capital to make acquisitions, and for building their teams. If they have built a portfolio of businesses where their investment is disproportionately high compared to the "difficulty" of those business, and their team is not what it should be, then we believe that their incentive should reflect that, irrespective of the effort they are expending to manage their portfolio. Similarly, if the manager has a portfolio of great businesses that "run themselves" and the manager has trained and promoted a competent and inspiring team, then I have no problem with them reaping the incentives provided by the bonus formula. However, if either manager is unethical, is not respected by their subordinates, or is trading off long-term success for short-term profits to optimise bonus at the expense of long-term shareholder value, then we will replace them” (Leonard, 2018).

Reference List

Bergstresser, D., Philippon, T. (2006) CEO incentives and earnings management. Journal of Financial Economics 80, 511–529.

Burgstahler, D., Hail, L., Leuz, C. (2004) The Importance of Reporting Incentives: Earnings Management in European Private and Public Firms. The Wharton Financial Institutions Center.

Burhop, C., Lübbers, T. (2010) Incentives and innovation? R&D management in Germany’s chemical and electrical engineering industries around 1900. Explorations in Economic History 47 (2010) 100–111 101.

Cheng, Q., Luo, T., Yue, H. (2013) Managerial incentives and management forecast precision. Research Collection School Of Accountancy. January, 1-46.

Chidambaran, N. K., Sarath, B., Zheng, L. (2019) Shareholder Investment Horizon, Management Incentive Horizon, and Real Earnings Management. New York University.

Constellation Software Inc. (2020) Financial Report: Fourth Quarter Fiscal Year 2020. Toronto, Canada. Constellation Software Inc.

https://www.csisoftware.com/docs/default-source/investor-relations/statutory-filings/q4-2020-shareholder-report.pdf

D’Andrea, G., Arnold, D. (2003) Zara. Harvard Business School Case 503-050, March 2003.

Dorsey, P. (2004) The five rules for successful stock investing: Morningstar’s guide to building wealth and winning in the market. Wiley.

Fontana, F., D'Alise, Ch., Azzurra Marzano, M. (2015) Incentives and Innovative Propensity. Review of Contemporary Business Research December 2015, Vol. 4, No. 2, pp. 39-56.

Frey, B., Osterloh, M. (2002) Successful Management by Motivation: Balancing Intrinsic

and Extrinsic Incentives. Zürich, Springer.

Greenwald, B. &. Kahn, J., (2007) Competition Demystified: A Radically Simplified Approach to Business Strategy. New York: Portfolio.

Keeley, L., Walters, H., Pikkel, R.,Quinn, B. (2013) Ten Types of Innovation: The Discipline of Building Breakthroughs. Wiley.

Jensen, M., Murphy, K. (1990) Performance pay and top-management incentives. Journal of Political Economy, April, vol. 98, no. 2, pp. 225 – 264.

Leonard, M. (2018) Constellation Software Inc: Selected Investor Questions Received Toronto, Canada. Constellation Software Inc.

https://www.csisoftware.com/docs/default-source/investor-relations/shareholder-q-a/qa-july-25-2018-final.pdf

Manso, G. (2017) Creating Incentives for Innovation. California Management Review, Vol. 60(1) 18–32.

Mayer, C. (2015) 100 baggers: stocks that return 100-to-1 and how to find them. Baltimore, Laissez Fair Books.

Pecaut, D., Wrenn, C. (2017) University of Berkshire Hathaway: 30+ years of lessons learned from Warren Buffett & Charlie Munger at the annual shareholders meeting. Pecaut and Company.

Smith, T. (2020) Investing for Growth: How to make money by only buying the best companies in the world. An anthology of investment writing, 2010–20. Harriman House

Taleb, N., Sandis, C. (2014) The Skin In The Game Heuristic for Protection Against Tail Events. Review of Behavioral Economics, 1: 1–21.

Thorndike, W. (2012) The Outsiders: Eight Unconventional CEOs and Their Radically Rational Blueprint for Success. Harvard Business Review Press.

Excellent!

Con Alphabet, de las posiciones que más tiempo llevo en cartera.