#34 Management & incentive schemes I: the ugly

#34 Management & incentive schemes I: the ugly

“Never, ever, think about something else when you should be thinking about the power of incentives. Show me the incentive, and I will show you the outcome”

Incentives are not a guarantee of anything. A company with a terrible incentive system can have an incredible performance. In the same way, a good incentive system does not ensure success. Incentives are just one more leg in the study of a company and its management. But it is a fundamental one.

In the next 3 posts, we are going to look at an array of incentive systems that we have classified into 3 categories: the good, the bad, and the ugly. We start today with the ugly ones.

Welcome to Edelweiss Capital Research! If you are new here, join us to receive investment analyses, economic pills, and investing frameworks by subscribing below:

When it comes to evaluating the quality of management, the incentive system is just one more of the ticks to check. We consider it very important to see the management has real ownership in the business. We want partners running our businesses. Ideally, we find that in the figure of a founder, but not necessarily only there. In the end, something important for us is that the stake of the management in the company is many times higher than the total annual salary they receive.

Another fundamental part of the analysis would be the capital allocation decisions. Does management even talk about returns on capital? Most don't. Do they explain capital allocation decisions in a reasoned way? Or do they just assign FCF randomly? A few dividends, a few buybacks, ... Do we have new strategic plans every two years? Do they use grandiloquent words? Do they meet the objectives they set 3 years ago and comment on them?

In the end, there are infinite qualitative aspects to take into account, but in this series of 3 posts, we are going to focus on how we think about incentive systems.

Rather than go and talk about "theory", we're going to focus on specific examples because here there are no absolutes. We want to emphasize this very much. Just because we don't like an incentive system, it doesn't mean that management is dishonest. It doesn’t mean either that they are not aligned with shareholders, let alone that future performance will not be good. It is simply the way we approach investment decisions.

Finally, and before getting down to business, it should be noted that the incentive system is determined by the board of directors, elected by the shareholders. In other words, it is the responsibility of the shareholders to impose an appropriate incentive system.

Kimberly Clark de México (KCDMY)

In some jurisdictions, regulators do not require companies to report the management compensation system. This is the case with Kimberly Clark de México, which is otherwise a pretty decent business.

Just because something is not mandatory, it does not mean a transparent company could not share willingly this information. That is why we contacted the company to ask for this information. This was their response:

"Unfortunately we do not disclose the compensation of the executive team, nor their incentive schemes, targets, or shareholding position. Regards"

There are no further questions your honor.

Allfunds Group (ALLFG)

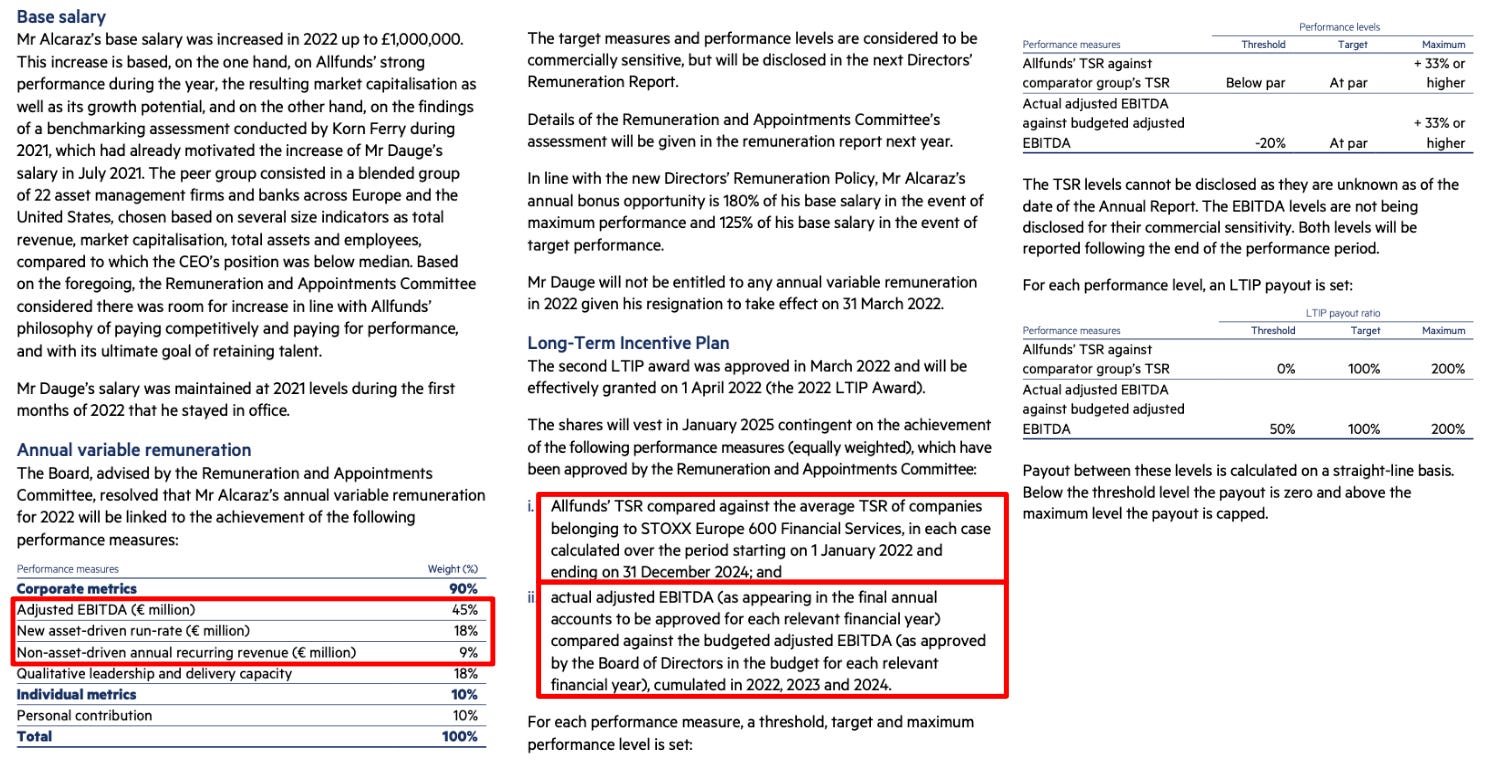

Allfunds Group provides a B2B WealthTech platform connecting fund houses and distributors (banks). Allfunds monetizes these services by charging fees to fund managers that are ~75% based on Assets under Administration (AuA) and ~25% based on transaction volumes. In a business with obvious network effects and scale benefits, Allfunds has more distributors, more fund managers, and more AuA on its platform than its competitors in Europe.

Great business and solution. Asset light and with very high barriers to entry, in a highly regulated environment. They have been focusing on growth via acquisitions to become number 1 in Europe. As a principle, we are reluctant to companies growing inorganically. Most of the time, they pay too much for synergies that never occur, leading to unsatisfactory ROIs, and serving only to make the company larger for the ego of its managers. Bigger is not synonymous of more profitable for an investor. That is why in these situations of inorganic growth, our eyes go straight to the multiples paid on these acquisitions. We want to understand the rationale behind them, and above all, to check the incentives plans to see if management is incentivized to grow for growth's sake, or if they have to grow in a wise way.

Allfunds, to be fair, presents the remuneration of the management in a transparent and clear way. For that, kudos. However, we don't like what we see.

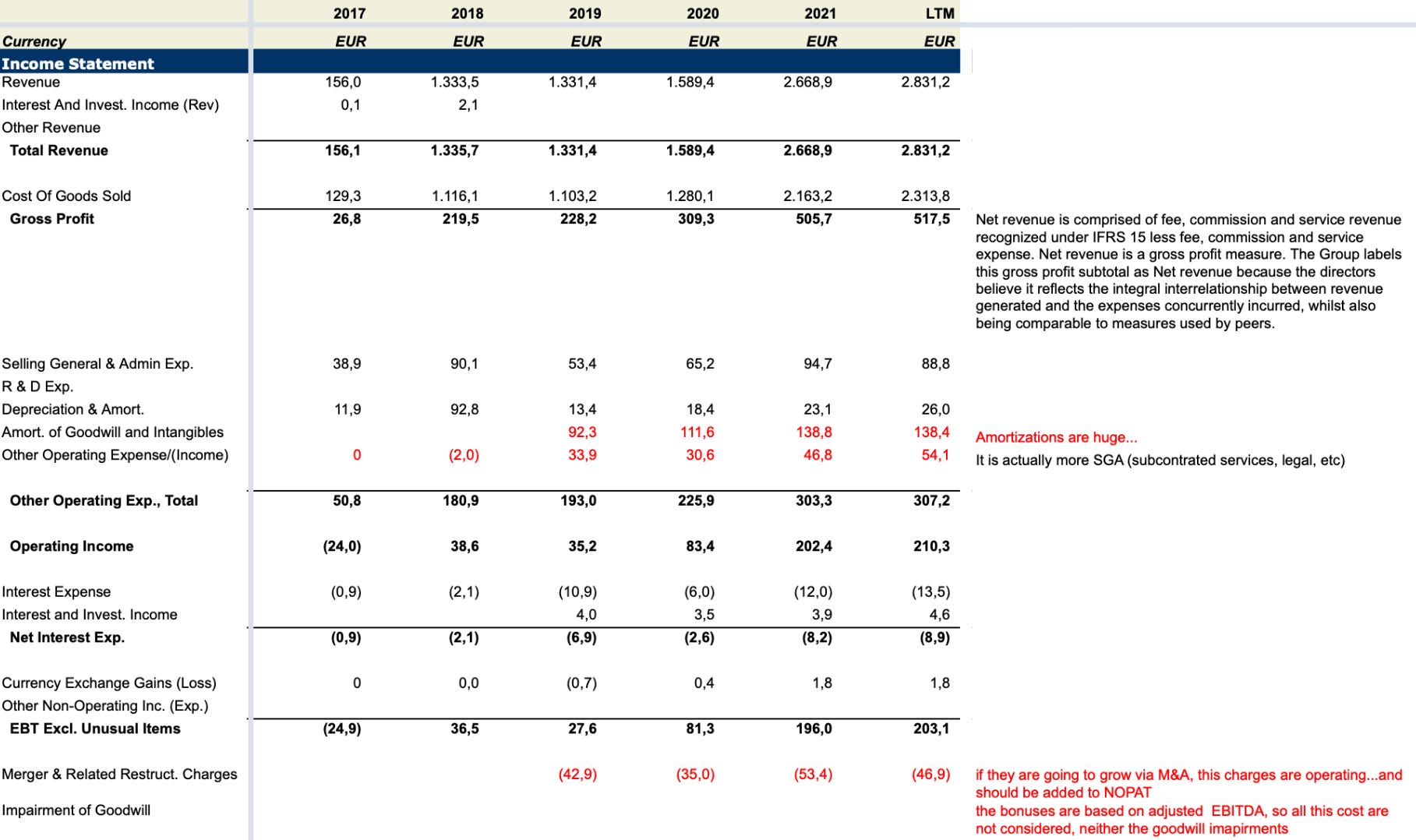

If a company has a strategy to grow via acquisitions, the management should be incentivized to do great acquisitions, a.k.a high ROI. If otherwise, it is incentivized to increase revenue and Adj. EBITDA, no matter the acquisition they do, any new acquisition would make them closer to their targets. Allfunds is remunerating the management team to achieve growth, not profitable growth.

We are always suspicious of EBITDA as KPI, and even more of Adj. EBITDA. Digging a bit into the financial statements, we can see how the management is not considering merger or restructuring charges as operating expenses, despite being something recurrent. Removing also amortizations, Adj. EBITDA figure is going to look always great, even if little of it is converted into FCF.

Finally, we can see how the long-term incentive plan is again based on Adj. EBITDA and Total Shareholder Return (TSR) versus a benchmark. In the next post we will see why TSR, although many investors find it a good proxy for remuneration, can incentivize misallocations of capital. Nevertheless, in this case, it is quite shocking that a financial services platform, with the characteristics and units economics of a platform, compares its return against companies belonging to STOXX Europe 600 Financial Services, where just UBS and Credit Suisse represent 20% of the Index. We consider it a low hurdle.

We reiterate that Allfunds has many ingredients to be a good deal. Moreover, despite what we consider to be poor incentives, management may execute well and shareholder returns may be very excellent in the future.

These kinds of incentives systems, uncorrelated with returns on capital, prioritizing growth for growth's sake, are the general trend. However, we would like to show further a couple of other examples to highlight some other important aspects to watch out.

Mitie Group (MTO)

Mitie Group provides outsourcing services mainly in the United Kingdom, operating in 7 different verticals. In 2017, after several years of misperformance, a new management came in to turn around the company. On the capital markets day in 2019, the management explained how these previous 2 years had been the base for a new Accelerated Value Creation phase, with the goal to grow organically at 2-4% and expand margins from 3,7% to a range between 4,5-5,5%. All these goals were set for 2022. There have been some improvements, especially in the working capital, but the company is still struggling with the margins, far away from the goals.

To compensate, the management has set a new strategy. The new Mitie with a new growth path. There is no longer a single mention of organic growth in the annual report. The same medium-term margin goals from 2019 for 2022 are repeated, but without any specific date now. After a big acquisition last year, it seems the company will focus now on inorganic growth. If one takes a look at the incentives, the new strategy seems to be self-explanatory to achieve the bonus targets.

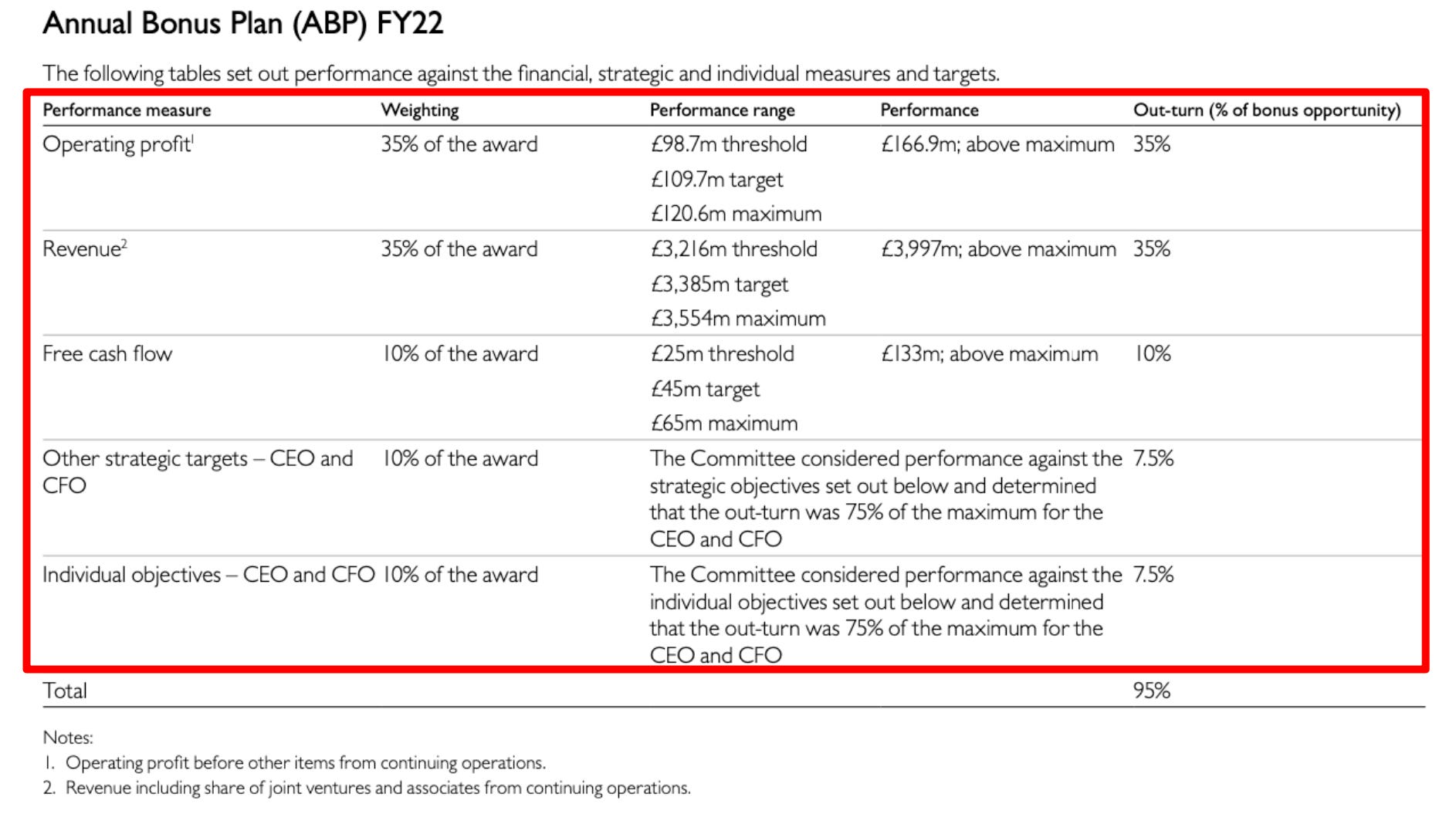

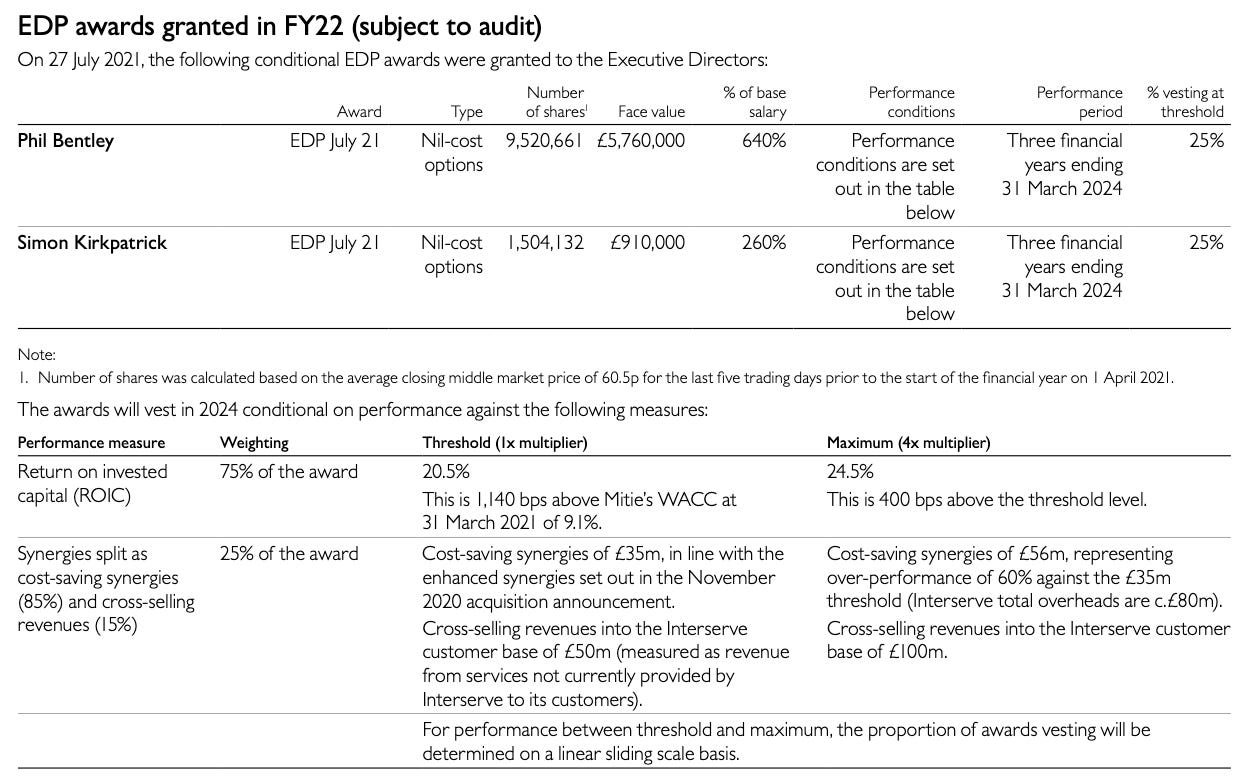

The company had also an Enhanced Delivery Plan for the CEO and CFO, which could amount to a non-negligible 640% of the base salary based on ROIC. And the target is a very nice 20%. Finally something we like.

However, there is a but. Last year the management recognized the ROIC was 8,7%. But suddenly they claimed to have achieved a 29,9% ROIC this year. Magic? Well, the devil is in the details. Our numbers got us closer to a 15% ROIC. How is it possible? We are not going to discuss here how to calculate the ROIC. We have post already explaining it. But if they don’t account for restructuring or acquisition costs to get their operating income, when it is 1/4 of their operating expenses and they plan to continue acquiring businesses, we don’t have anything further to say.

Coherent Corporation (COHR)

Last but not least, another example we find interesting to review. II-VI merged recently with Coherent Corporation, in a kind of LBO led by Bain Capital. Sometimes, these kinds of operations come as great opportunities. In some others, everything simply smells rotten.

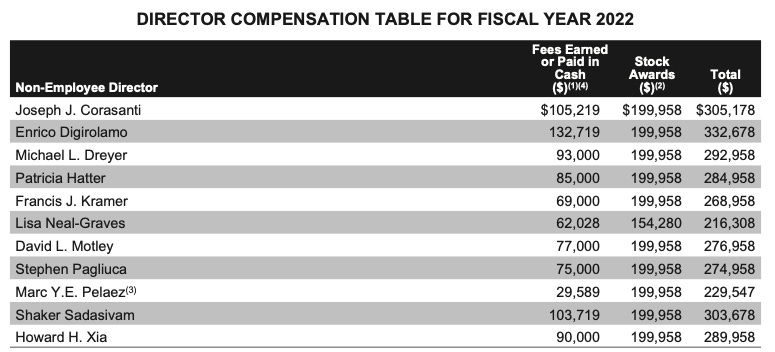

As a result of the merger, the new board of directors has been made up of 13 members, 11 of them being non-executive members. Large boards in which no one is responsible for anything. In addition, considerable fees plus stock awards totaling no less than $215,000 per year have been approved at the expense of the shareholders. And this is only for non-executive directors.

The executive management team is incentivized, in a similar way to the examples we have seen above, based on the achievement of certain revenues and profits, always in absolute terms and not relative to returns on capital or margins.

However, what has caught our attention is the following table for assessing the long-term incentives:

Note it includes the share performance compared to the S&P Composite 1500—Electronic Equipment, Instruments & Components. What we find surprising is, even if the stock would perform 40% below its reference index, the management would still be getting a 50% of the share payout!

This concludes today's post. Incentives aligned with shareholders do not ensure good performance. Nor do bad ones imply shareholder value destruction. But at the very least, we should be aware of what we are asking a management team to prioritize, because their performance may be influenced by it.

In the next post, we will look at examples of slightly better incentive systems. Incentives that many investors normally consider to be "aligned" with their interests. Increasing EPS, FCF per share, or TSR being better than the index may sound good at first glance, but it can also lead to misallocations of capital.

Finally, in the third part of this series, we will look at excellent incentive schemes. Systems with long-term shareholders in mind, and see how they tend to correlate with companies that have generated great value over time.

If you enjoyed this piece, please give it a like and share!

Thanks for reading Edelweiss Capital Research! Subscribe for free to receive new posts and support our work.

If you want to stay in touch with more frequent economic/investing-related content, give us a follow on Twitter @Edelweiss_Cap. We are happy to receive suggestions on how we can improve our work.

Loved this piece.

No number should be taken at face value. With that said, I actually quite like adjusted EBITDA and the like! I like looking at how companies report non-GAAP numbers in an effort to understand how they think about business. Not always malicious. Of course, it's imperative to make your own adjustments and compare to GAAP, non-GAAP, etc. It's one of the best ways to contextually understand all of the levers of value creation and identify what the company is most sensitive to.