#44 Mergers & Acquisitions III

#44 Mergers & Acquisitions III

The acquisition of Tiffany’s & Co. by LVMH

Corporate acquisitions success often hinges on a complex mix of financial analysis, strategic planning, and operational execution. The recent acquisition of Tiffany & Co. by luxury conglomerate LVMH is a case in point. The deal, which closed in early 2021 after months of legal wrangling, is the largest ever in the luxury sector. It has generated much interest and debate among industry insiders, investors, and analysts. In this article, we take a closer look at the LVMH-Tiffany deal, from its origins and rationale to its financial implications and impact on shareholders.

"We prefer to buy companies that can acquire other companies for a simple reason: If you have the skill and the talent to acquire other companies and do it well, that means you have a durable competitive advantage."

"If you're buying a company for the long term, you're buying it because of the people who run it. You're not buying it because of the numbers you're looking at today”

Welcome to Edelweiss Capital Research! If you are new here, join us to receive investment analyses, economic pills, and investing frameworks by subscribing below:

In the previous post, we mentioned that today we would be examining various cases of acquisitions in different companies. The truth is that as we began writing about the first one, the content got out of hand, and it is not realistic to analyze many of them in a single post. Therefore, we have decided to make the series an ongoing feature and analyze different acquisitions in separate installments. We hope you enjoy them.

The acquisition of Tiffany’s & Co. by LVMH

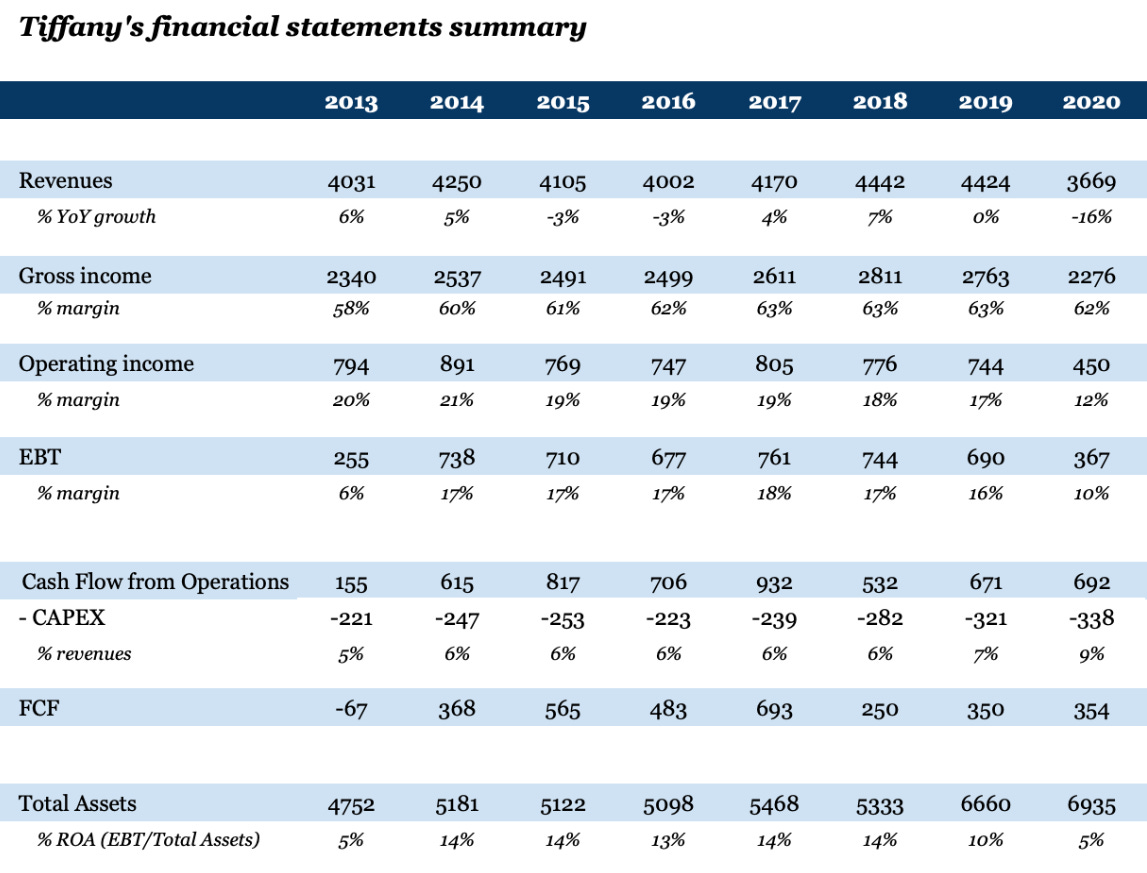

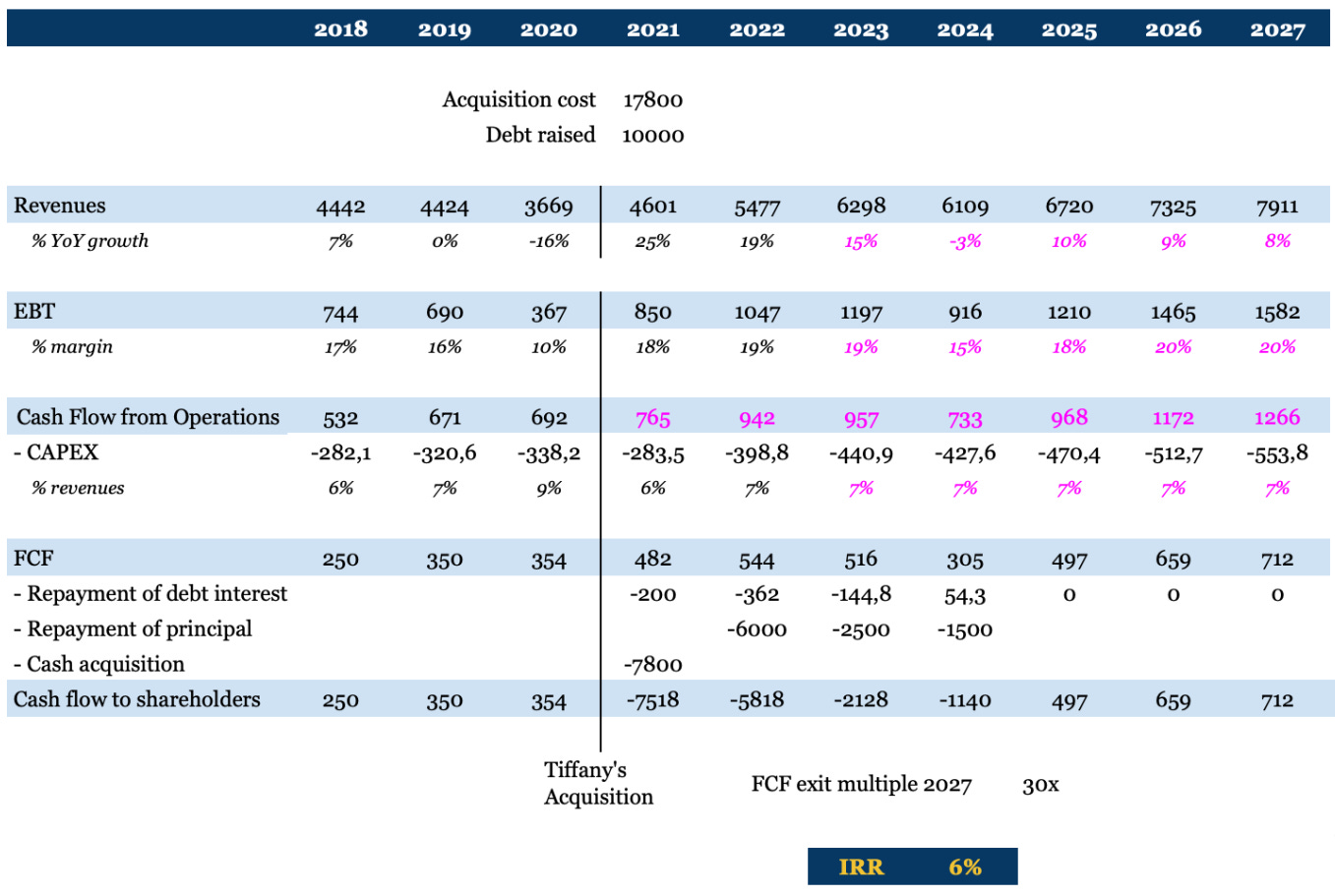

Bernard Arnault and LVMH have a spectacular track record that is entirely undeniable. However, when LVMH made the final decision in January 2021 to pay $17.8 billion (resulting in goodwill of $14.5 billion) for the acquisition of Tiffany & Co., many doubted the profitability of the transaction. After all, Bernard was paying a 37% premium on the market capitalization, which equated to almost 50 times the LTM earnings before taxes (or 26x earnings in a year like 2019).

He was paying 50 times the average FCF of the last few years for a business that, while possessing a very powerful heritage brand, had been stagnant for the past 8 years.

Watches & Jewelry

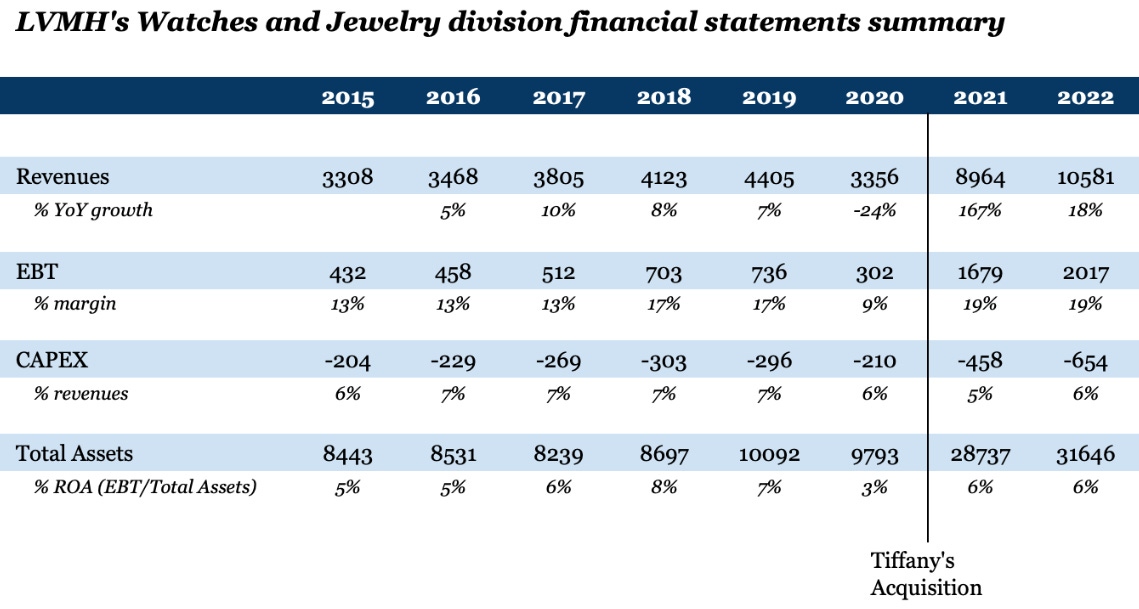

Thanks to its own organic growth and the acquisition of Tiffany & Co., the Watches & Jewelry division has become one of the most promising growth drivers of the French firm, with brands such as Bvlgari and TAG Heuer, among others.

There are three key aspects that would have caught our attention if we were looking at these numbers at the time of the acquisition. While Tiffany & Co. had been stagnant for years, LVMH had been successfully growing its sales in the category. This first factor alone provided a rationale for paying a premium over the market price, in the hopes to infect and achieve some of this growth to the new crown jewel. Additionally, Tiffany & Co.'s ROA was much higher (double) than that of the brands in LVMH's portfolio. While having stable sales reduces the need for working capital, the difference in ROA is substantial and suggests higher asset quality at Tiffany & Co., at least in this segment. However, the price was initially considered demanding.

Note: I exclusively employ ROA as capital efficiency metric, as it is the only disclosed metric available for this purpose.

Finally, not all brands were created equal. The resilience of Tiffany's brand, even during the pandemic, was far superior to that of the other LVMH brands.

The integration in LVMH

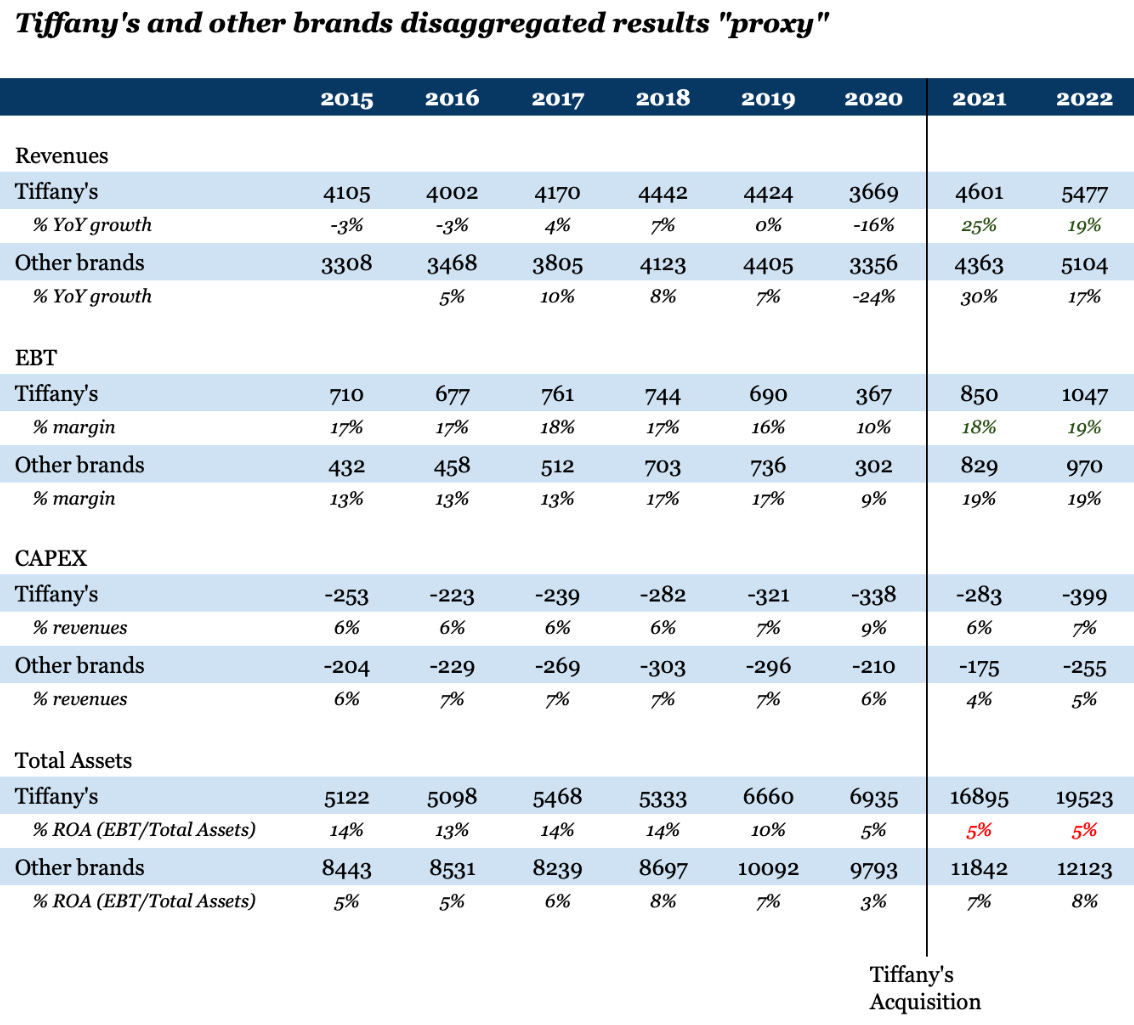

Looking at the disaggregated results of Tiffany's nowadays is not an immediate task, as the group does not directly publish them. However, public information is sufficient to give us an idea of how the integration has worked.

Assuming a set of criteria that we consider quite reasonable, the table below shows our estimate of Tiffany's disaggregated results.

There are several things that can be said about it. The first and most obvious is that growth has returned to Tiffany's after nearly a decade of flat performance. And it was not just due to the after pandemic effect. The incredible results of 2022 demonstrate that LVMH has given a facelift to the New York jewelry house. Additionally, there has also been a slight improvement in margins, possibly due to some operational leverage provided by the holding.

However, something that may seem negative at first glance is the decline in capital efficiency, as measured in this case by ROA. The use of goodwill, or not, to measure the return on capital of acquisitions is generally a debated aspect in the community, and often not well understood.

Ideally, to properly examine things in each area of analysis, we should have a balance sheet and profit and loss statement for the original company, and another for each of the acquired companies. This way, we could analyze the quality and capital efficiency of the original company on its own, and the acquisitions as what they are, investments. Having everything together makes things more complicated.

What does all this mean for the shareholders?

We like to look at acquisitions through two checks:

1st: Expected IRR

It is very easy to talk with hindsight knowing the results of the first two years in this case. To be honest, we never would have expected what LVMH has achieved with Tiffany's to date, but that's what happens when you're dealing with people who have consistently demonstrated that they know what they're doing. That's difficult to model.

Additionally, LVMH issued net debt of 10 billion at super low interest rates in 2020. At this point, we are not sure if they are very lucky or extremely good. Nevertheless, their average interest rate was 2% in 2021 and 3.6% in 2022. The debt is almost paid back at this moment.

To arrive at the final result, I make some fairly conservative assumptions, stressing the model: one year of declining sales and depressed margins (life is not linear), and I also assume only an 80% conversion from EBT to CFO (when in the last five years it has been 100%, but I assume certain working capital requirements to fuel growth).

Finally, I assume a 30x FCF multiple in 2027 (considering that they paid 50x).

There is no need to state that all of Tiffany's value is found in its terminal value (with a exit multiple of 50x the IRR would be 14%), but in the random event that the numbers presented here are met, we can see that the return is quite mediocre. One thing worth noting is the very early repayment of debt, which obviously limits the profitability of the transaction.

The fact is that acquisitions at high multiples, despite the wonderful competitive advantages, are very difficult to offer attractive returns.

2nd: Company’s ROIIC

Financial projections, models, and IRR seek to predict an uncertain future. However, past numbers never lie. That is why even though history never repeats itself, it tends to rhyme. Therefore, it is always crucial to analyze the ROIIC over an adequate period of time to understand whether a company is creating value with acquisitions or not.

It's worth noting that a company may also be destroying value with acquisitions, but this could be covered up by an exceptional core business. And this could be the case of LVMH here. Despite the increase in assets on the balance sheet, or even not so profitable acquisitions, the company has continued to improve its ROIC in recent years. The return on incremental invested capital average in the last five years has been around 18%.

How is it possible, then, that despite such a massive capital deployment in the acquisition of Tiffany's, the company has increased its returns on capital? Our answer is that it appears that LVMH's business in its main vertical, Fashion and Leather Goods, has made a huge leap forward. In the past few years, the average return on assets was around 25%, but now we are seeing a return of 45%. It's just mind-blowing.

Exceptional managers know to deal with all this complex information. The lesson to be learned here is that when someone has a track record of making good decisions in the past and with skin in the game, when faced with controversial situations, we should give them space. It is likely that person knows much better what they are doing. After all, what is investing if not entrusting our capital to people who know how to make it grow?

If you enjoyed this piece, please give it a like and share!

Thanks for reading Edelweiss Capital Research! Subscribe for free to receive new posts and support our work.

If you want to stay in touch with more frequent economic/investing-related content, give us a follow on Twitter @Edelweiss_Cap. We are happy to receive suggestions on how we can improve our work.

great take, thank you!

Nice work!