#20 Portfolio management I: portfolio size

#20 Portfolio management I: portfolio size

A framework for decision-making and capital allocation: improving the quality while reducing the number of decisions.

Portfolio management is a topic of the greatest importance. Investor’s performance over the years is going to be closely related to the proficiency of this management rather than in the stock picking skills. However, and for some inexplicable reason, it is an area completely forgotten in the literature. Investors tend to prefer discovering new hidden gems rather than spending time making better decisions. It is understandable. It is the same psychological factors that make companies focus on increasing revenues rather than focusing on achieving better returns on capital.

However, as anything important in life, portfolio management is not a trivial task. It requires time, patience, methodology and constant process improvement. Therefore, during the next 3 articles we will focus on establishing actionable guidelines and a transparent framework for portfolio management. This first piece will discuss about the number of companies in a portfolio. Next week, we will discuss the position sizing criteria, translating qualitative aspects into quantifiable parameters. Finally, a third one where we will analyze real live situations and how to allocate capital with a clear process behind.

Welcome to Edelweiss Capital Research! If you are new here, join us to receive company analyses, economic pills, and investing frameworks by subscribing below:

While the literature on investing extensively documents how to evaluate and value a company, bizarrely there is very little literature on how to size investments within a portfolio or how to deal with the day to day operative. However, these decisions will have a long term impact on our performance. The literature on this subject is mostly based on managing short term volatility of stock prices and based on efficient market theories, rather than managing long term risk of permanent impairment of capital (Ensemble Capital, 2019) and setting a framework for rational capital allocation decisions.

Suppose you have a portfolio of X companies and you receive new capital (income, investor’s new funds, liquidity, etc). What do you do? How do you take the decision to allocate this new cash among the X companies in your portfolio? Evenly split? All to the most undervalued? It is definitely not easy.

Simple models thrive when the problem is ill-structured, complex and the information is incomplete, ambiguous, and changing. Therefore, it is all about methods and processes to take the best capital allocation decisions based on the current available information. But how do we know what is the best decision to take? That’s what we are going to explore here.

Note: everything we are going to see in these articles is the methodology I have developed based on my experience and my investment philosophy: invest in good businesses run by good managers, bought at fair prices and enjoy the bumpy ride with patience. It doesn’t have to fit everyone and at the same time, I am sure there are several different approaches that might generate better returns. Always make your own rational decisions.

The general approach to portfolio management

The main literature on portfolio management theory that can be found is solely based on the Modern Portfolio Theory (MPT). In fact, certificates such as the CFA have a big part of the curriculum focused on it. The economist Markowitz introduced his MPT in a 1952 essay, for which he was later awarded a Nobel prize in economic sciences. Economist and Nobel prize winner, double red flag. Jokes aside, it is a mathematical framework for assembling a portfolio of assets such that the expected return is maximized for a given level of risk. Its key insight is that an asset's risk and return should not be assessed by itself, but by how it contributes to a portfolio's overall risk and return. The main problem: it uses the variance of asset prices as a proxy for risk.

If a theory is based on considering volatility as risk, instead of as an opportunity, the results of it can hardly bring any value. Buffett criticized it wonderfully using his experience when he invested in The Washington Post:

"We bought The Washington Post Company at a valuation of $80 million back in 1974. If you'd asked any one of 100 analysts how much the company was worth when we were buying it, no one would have argued about the fact it was worth $400 million. Now, under the whole theory of beta and modern portfolio theory, we would have been doing something riskier buying stock for $40 million than we were buying it for $80 million, even though it's worth $400 million-because it would have had more volatility. With that, they've lost me."

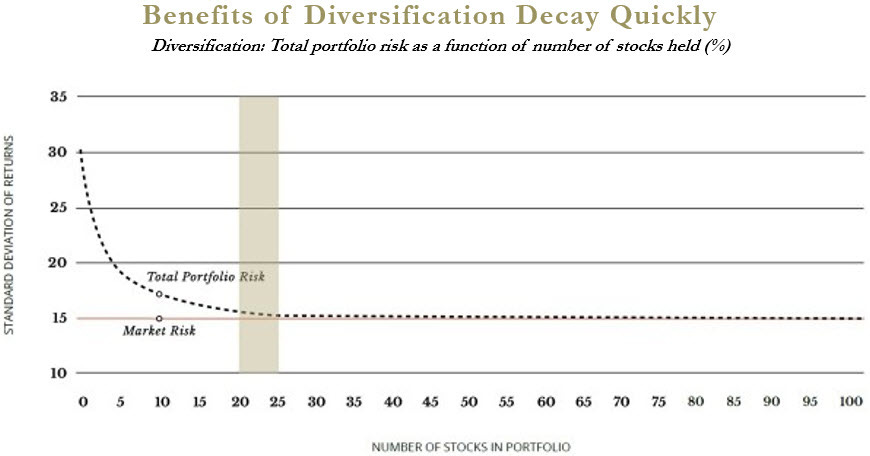

However, one of the applications of MPT that have still been adopted by the financial community is the "belief" that a portfolio with between 20-30 positions combines the benefits of diversification and still maintains the right concentration to outperform the market.

As Ensemble (2019) stays in their series of articles, investment managers adjusted a study from 1970 to say "we pick the best 30 stocks achieving the same diversification of the market and optimizing the return”. What the study was actually proving was that a randomly created portfolio of 32 stocks could benefit from a 95% of the diversification, compared to a portfolio of the entire New York Stock.

What the chart shows is that as you add stocks to a portfolio, the volatility of the portfolio declines. Could make sense, but if I add 30 stocks, all dependent on the price of a commodity, volatility will probably still be higher than the market.

Furthermore, what is the problem with volatility? One of the main wonders of liquid markets such as the stock market is precisely the opportunities given by investors' irrationality, expressed in the form of volatility. Funds with “uneducated” investors or even most private investors might seek to avoid volatility, so they build portfolios with more than 20 stocks. This is one of the main reasons why so little funds outperform the market. It is very difficult to do it with large portfolios plus management fees. Many other times, regulations force funds to have over a certain number of positions in an attempt to “protect” investors.

The intelligent investor understands risk as it is: the possibility of a permanent capital loss. Embrace volatility as a friend offering bargains in the market.

The concentrated portfolio

"Diversification serves as protection against ignorance. If you are a know-something investor, able to understand business economics and to find five to ten sensibly priced companies that possess important long-term competitive advantages, conventional diversification makes no sense for you” (Hagstrom, 1999).

We have a strong bias towards action and over-diversification because we don't want to miss out on the next big thing. We do not want to stay away from the next new technology that will revolutionize the world, the new Google, etc. Other times, we want to capitalize all the time we have spent understanding a new company. We need to see a result on our time. That led us to invest. How is it possible that we find extraordinary value and quality in most of the companies we analyze in depth!?

Finally, managing a portfolio of >20 companies is only accessible for professional investors (and still difficult if it is done only by one person). Being invested in 20+ companies means you will probably have an universe of 100+ companies analyzed and identified. Are there so many outstanding companies? Maybe we could find such a number of good businesses out there. But there are not that many where an extraordinary business is combined with a revel capital allocator and superb culture. Think about it and act accordingly.

Nick Sleep shut down Nomad Investment Partnership in 2014. He told his investors that his recommendation was to merely hold Amazon, Costco, and Berkshire Hathaway for the next 10 years.

The lectures we can get from Buffett and Munger are infinite. We would never appraise them enough how easy and clear they explain things.

There is not a magical number of companies to have in an optimal portfolio. It is always going to be a trade off between our convictions/knowledge and the natural fear of the unknown future. However, and as a rule of thumb, try to look for 3 to 10 wonderful businesses with whom you feel safe and confident. Remember the Holy Trinity: great business, great culture-CEO and a good price. Afterwards, avoid the temporal noise of the market.

We have to improve the quality of our decisions, not increase the number of them.

But the work is not done. The role of the investor does not finish there. You have to keep looking for these little wonderful businesses and learn about them. And when Mr. Market will give us the opportunity, and it always comes, we have to be prepared to make the decision. But this is already a topic for next week.

In part II of this series of articles, we will discuss how to decide what is the right weight of our wonderful businesses in our portfolio.

If you enjoyed this piece, please give it a like and share!

Thanks for reading Edelweiss Capital Research! Subscribe for free to receive new posts and support our work.

If you want to stay in touch with more frequent economic/investing-related content, follow us on Twitter @Edelweiss_Cap. We are happy to receive suggestions on how we can improve our work.

References

Ensemble Capital, (2019). Position sizing series. https://intrinsicinvesting.com/2019/04/22/how-many-stocks-should-you-own-in-your-portfolio/

Hagstrom, R.G., (1999). The Warren Buffett portfolio: mastering the power of the focus investment strategy. Wiley

Turtle Creek, (2013). Investment Edge 3: Portfolio Construction https://www.turtlecreek.ca/wp-content/uploads/2020/09/TCAM-Thought-Piece-Edge-3-Portfolio-Construction-Apr-2013.pdf

Fantastic. I have also been struck by the lack of good texts on portfolio construction in the investing canon. And brilliant investors more often than not has not much to say about it?!! Even though from first principles it should be one of the most important aspects of investing?! Looking forward for the next parts!

Good write up. looking forward to the next one!