#22 Portfolio management III: capital allocation

#22 Portfolio management III: capital allocation

A framework for decision-making and capital allocation: reacting to market volatility.

In the last two weeks, we have been discussing portfolio and position sizing. We looked at a framework to translate our qualitative knowledge and conviction into numbers, helping us to decide the optimal position sizing for our portfolios.

But all of it was based on static knowledge and prices. Markets are dynamic, new information is being created continuously and prices are constantly changing. Knowing how to react and adopting processes to manage this volatility in our portfolio will be the scope of this last article of the series on portfolio management.

Welcome to Edelweiss Capital Research! If you are new here, join us to receive company analyses, economic pills, and investing frameworks by subscribing below:

We are long-term owners of companies and once we construct our optimal portfolio – the correct weighting for each of our holdings – we have no intention of making changes unless our relative view of our companies changes. However, the public market is constantly re-pricing our companies’ share prices and so to maintain our optimal portfolio we simply must react to the price changes by adjusting the size of each holding. This often results in significant changes to the size of each holding but it is all within the context of optimal portfolio construction (Turtle Creek, 2013).

This task is not trivial because it continuously challenges our discipline.

Concentrating the portfolio

You might have been waiting for a trigger to start concentrating your portfolio. We all tend to have a larger number of companies than we should. As we mentioned in the first part of the series, we have a strong bias towards action and over-diversification because we don't want to miss out on the next big thing or we want to capitalize on all the time we have spent studying a new company.

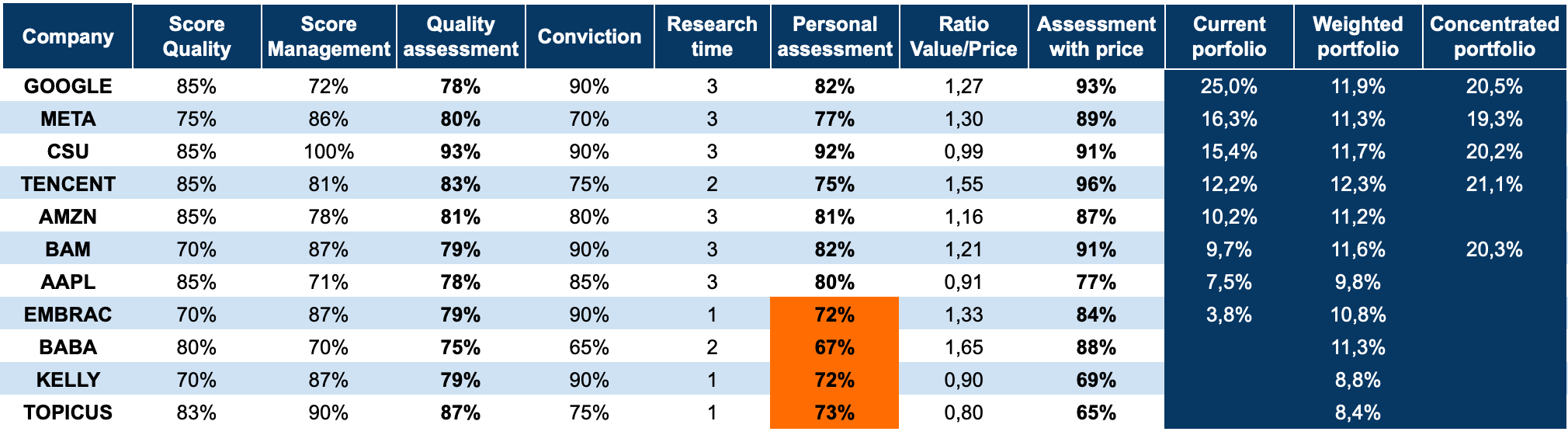

Let’s consider the following situation: imagine we actively follow 11 companies. Somehow we consider them all great businesses worth our time. From these 11 companies, we are invested in 8. However, we would like to concentrate our portfolio on 5 companies. We will still feel comfortable with the concentration risk assumed and we can expect a better return.

The result would be something like this:

I would never suggest such a drastic immediate change in a portfolio. May it serve as a goal to be achieved in the time you consider prudent. I have 85% of my portfolio in 7 positions. This is a never-ending process but I am committed to reducing it even further. The exercise for a portfolio of 30 companies willing to reduce it to 10 would be the same. The important thing is to find a framework that matches your style and stick with it.

An important rule I have set for myself is never to invest in a company if your assessment score is worse than 75%. You should set your own limit. Below this score, I don’t feel comfortable even if the price doesn’t make sense at all. See that these scores can be increased by studying a company further, increasing (or decreasing) our conviction with time.

A more concentrated portfolio will bring volatility along. It will test our conviction more often and our analytical analysis might suggest we rotate positions. Let’s discuss how to face these situations with examples.

Reacting to market volatility

Imagine we decided to reduce our portfolio to the 5 positions we selected, and with time, we get to assign each one of them our “ideal” weight. Naturally, volatility and market narratives will make the prices change. Our qualitative assessment and conviction, however, will remain stable most of the time. We should avoid get influenced by temporary market sentiments. Companies remain the same QoQ.

Let’s imagine the following events happen in our portfolio companies and we decide to re-evaluate our portfolio:

Google: macro headwinds continue. Our qualitative and long term expectations of the company remains the same, but the market lowers the price of the share even more.

Meta: presents unexpected positive quaterly results and the price rises to what we consider is the fair value.

Constellation: keeps delivering similar to the last 15 years but the price raises even more (we were considering already that under conservative considerations the price was already quite demanding).

Tencent: Pony Ma leaves Tencent. The State takes a major stake in the company. The quarter results are good but the share price drops due to the recent news. We believe the price is extremely undervalued.

Brookfield: share price goes down inexplicably. Results are in line with the expectations and the business keeps running as always.

Almost all the companies haven’t changed at all. Still, the market is “forcing” us to act.

Due to price changes, our suggested portfolio weights have changed considerably. What should we do?

Tencent: the Chinese government interfering directly in the company is a game changer. I reevaluate my thesis and my overall assessment drop below 75% (even if the valuation offers more potential). In a situation where I lose my confidence, I would sell the company.

Note: it is very important to differentiate between a thesis change and transitory problems/market narrative. In this case, we would have the State taking over a company, which is not the same as the State enforcing gaming regulations or fining the company for the “common good”. Even if we don’t like these kinds of “coercions”, we must be aware that even established “democracies” impose similar regulations.

Constellation: valuation becomes more demanding for this excellent company. Shall I reduce my positions as suggested by the tool? Maybe. In these cases where my conviction is intact, I apply 2 rules: let your winners run and when in doubt, do nothing. Therefore, I wouldn’t touch anything here.

Meta: one could think the same would apply here, but there is a huge difference in my personal assessment. Meta is close to the 75% limit, hence I would trim the position to the suggested one (especially because there are better opportunities to allocate the capital).

Google and Brookfield: both suffer from irrational market volatility. We should celebrate it, and actually we do. Our score has skyrocketed to 97 and 99%. We have some funds from Tencent and Meta, and we directly invest them in these two companies to reach the suggested weight.

Amazon: with the Tencent sell-off, we have reduced our portfolio to 4 positions, hence we have two ways forward:

We keep a 4 position portfolio: In this case, a question might arise. Why don’t we sell Meta and add Amazon? Our assessment and tool will suggest it. Another rule here to prevent portfolio turnover: we need >10% difference in our overall assessment to swap positions.

We start building a position in Amazon (as the next best score): Realize how we wouldn't get to the optimal weight because we prefer to reach the optimal positions for Google and Brookfield, since they have a better rate.

Note these kinds of dramatic changes are not that usual. As an example, I haven’t sold/trimmed any of my positions in the last year (despite all the volatility). Does it mean I leave my position weights to change with the market oscillation? To answer this question, let’s explore the last common situation we normally face.

Allocating new capital

Thanks to our personal income we normally have new funds to invest regularly. Luckily, we can “manipulate” our portfolio to make it tend to our “optimal” weights without trimming/selling any of our positions.

Imagine in the previous situation we decided to keep a 5 position portfolio and we added Amazon. However, we preferred to use the funds from Meta and Tencent to increase our stakes at BAM and GOOG to the optimal rather than in Amazon.

Easily, in this situation, new funds will go directly to close the gap we had in Amazon. Note that allocating new funds to our underrepresented positions allows us to avoid, most of the time, selling anything and hence, paying taxes. If possible, never stop compounding.

General rules

I think it is worth finishing summing up the last 3 posts in a clear rule-set of principles:

1. Concentrated portfolio

Decide the number of companies you want to have and stick to it. The lesser, the better. If you decide on 7, never go below/beyond 6 or 8.

2. Build a model to manage your portfolio

It will provide you with quantitative data from your qualitative knowledge. It is most useful to be able to compare different companies and make rational decisions. Establish your own parameters to make it fit your investment style.

3. When in doubt, do nothing

Avoid riding narratives with market glasses. Sleepover decisions and try to get data from your model to justify any decision you take.

4. Let your winners run

“To suggest that this investor should sell off portions of his most successful investments simply because they have come to dominate his portfolio is akin to suggesting that the Bulls trade Michael Jordan because he has become so important to the team” (Hagstrom, 1999)

5. Conviction > undervaluation

In case of doubt, remember you invest for the long term. Prices might be attractive at a particular point in time, but over the long term quality and management will be the main driver for value creation. Price can change immediately, conviction takes time to build. Set a minimum score to invest in a company independently of the price (i.e. 75%)

6. Reduce portfolio turnover

Price volatility might change your top scored positions, leading the model to suggest selling a company and adding another. To avoid constant turnover, set a hurdle rate below which you won’t rotate. I need a >10% difference in my overall score to swap positions.

This is a summary of my thoughts regarding portfolio management. A topic utterly forgotten in the investment literature despite its great importance. I hope it has opened up some thoughts and might help you to develop your own processes.

If you enjoyed this piece, please give it a like and share!

Tanks for reading Edelweiss Capital Research! Subscribe for free to receive new posts and support our work.

If you want to stay in touch with more frequent economic/investing-related content, follow us on Twitter @Edelweiss_Cap. We are happy to receive suggestions on how we can improve our work.

References

Edelweiss Capital, (2022). Rebel Capital Allocators: a trilogy discovering the 10 basic principles for finding outstanding CEOs. Part I, Part II & Part III

Ensemble Capital, (2019). Position sizing series. Link

Flatt, B., (2022). Brookfield AM: Q2 2022 Letter to shareholders. Link

Hagstrom, R.G., (1999). The Warren Buffett portfolio: mastering the power of the focus investment strategy. Wiley

Turtle Creek, (2013). Investment Edge 3: Portfolio Construction. Link