#32 Reinvesting beyond limits

#32 Reinvesting beyond limits

Amazon has only generated an aggregated 61b of FCF in 25 years, yet its market value is over 1T. What makes Amazon so special?

Over the last two years, and especially after the latest results, the markets seem to have fallen out of love with Amazon's business model. Three years of the biggest CAPEX investment cycle ever seen, coupled with two years of burning cash have completely changed the prevailing narrative.

We believe nothing has changed. We actually consider Amazon's model is poorly understood by investors. How daring of us. At this point, who would not get it?! Here below our reasoning.

Welcome to Edelweiss Capital Research! If you are new here, join us to receive investment analyses, economic pills, and investing frameworks by subscribing below:

It has been almost a year since Terry Smith decided, after many years, that it was time to invest in Amazon. He argued that he had changed a bit, but Amazon had changed too. Mr. Smith recognized that the increased relevance of AWS, 3rd party e-commerce, prime, and the Ads business made Amazon far more attractive. He justified that these businesses had higher returns on capital and therefore, made Amazon much more attractive. In addition, the company's price had remained flat over the past year, making it an attractive entry point.

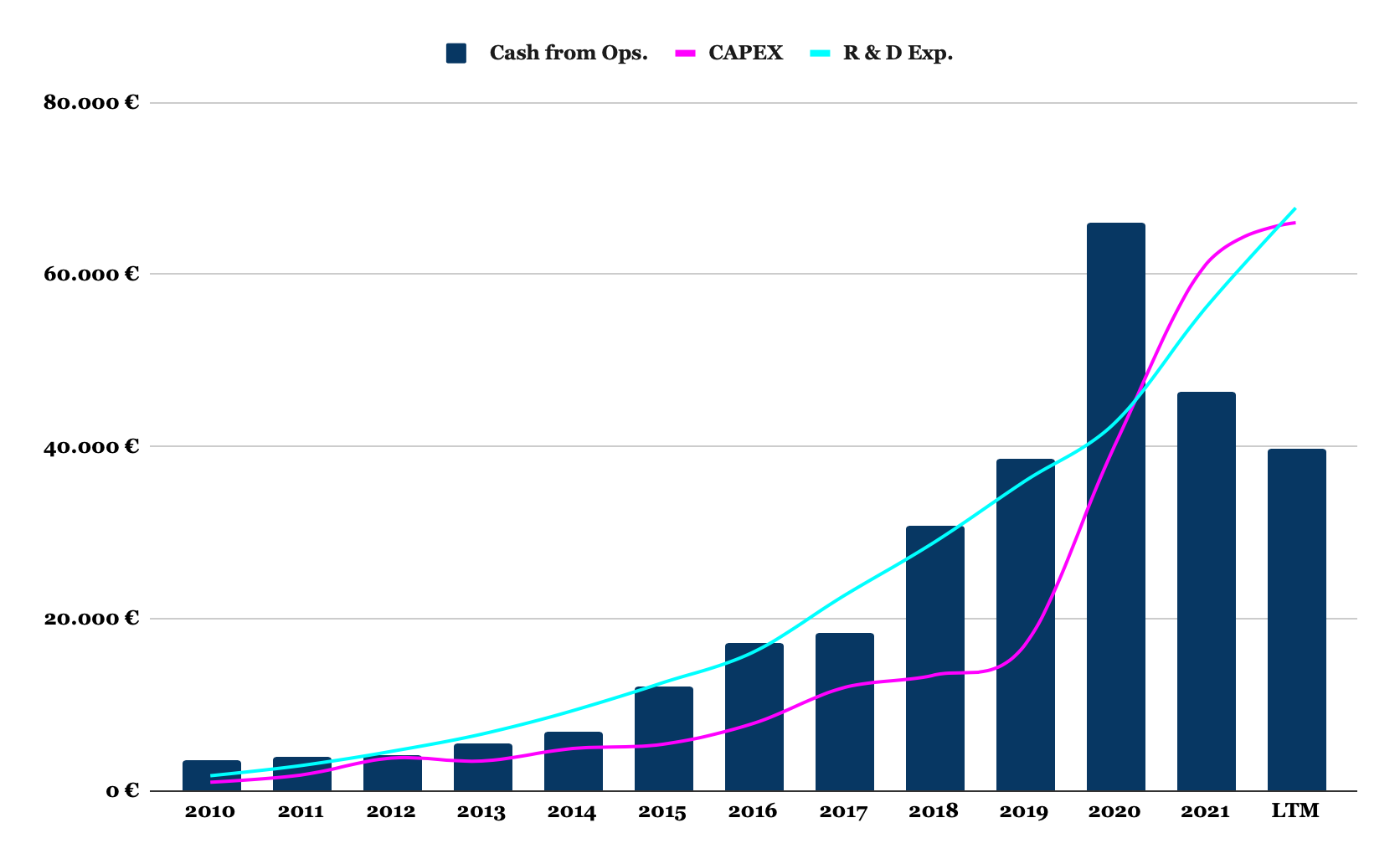

Since then, Amazon's stock has fallen more than 40%. Reasons? Three years with a never-before-seen CAPEX, a result of the need to increase the company's operating capacity after the COVID boom. It's ironic how many of the companies that succeeded in the pandemic are in trouble now. Nevertheless, all this has led the company to achieve record sales, but also to burn more cash than ever: -40 billion FCF in the last 2 years.

We believe that Amazon is a company misunderstood by the market. Its culture and way of doing things always reward customer satisfaction in the short term, even if it means shifting long-term shareholder value further in the future. But these are just words. Let us explain why we think this way.

Amazon is capital intensive, but…

Amazon's core businesses are asset-heavy, in contrast with the current trend and investors’ love for asset-light models. Amazon decided many years ago to have a vertical integration structure and avoid many 3rd party dependencies. They invested heavily, and they keep doing it now even more, in warehouses, fulfillment centers, data centers, servers, plus a long list.

However, their business model has a big advantage shared with some of the best SaaS, and even at a higher scale. Amazon charges for the products it sells before it has even bought them. What's more, it is able to pay for them long after they have been shipped. This creates a virtuous cycle that allows Amazon to finance its growth for free.

But it doesn't end there. Amazon was always criticized, especially pre-AWS, for the operating margins it had. That would be like criticizing Costco because its margins are lower than Walmart's!

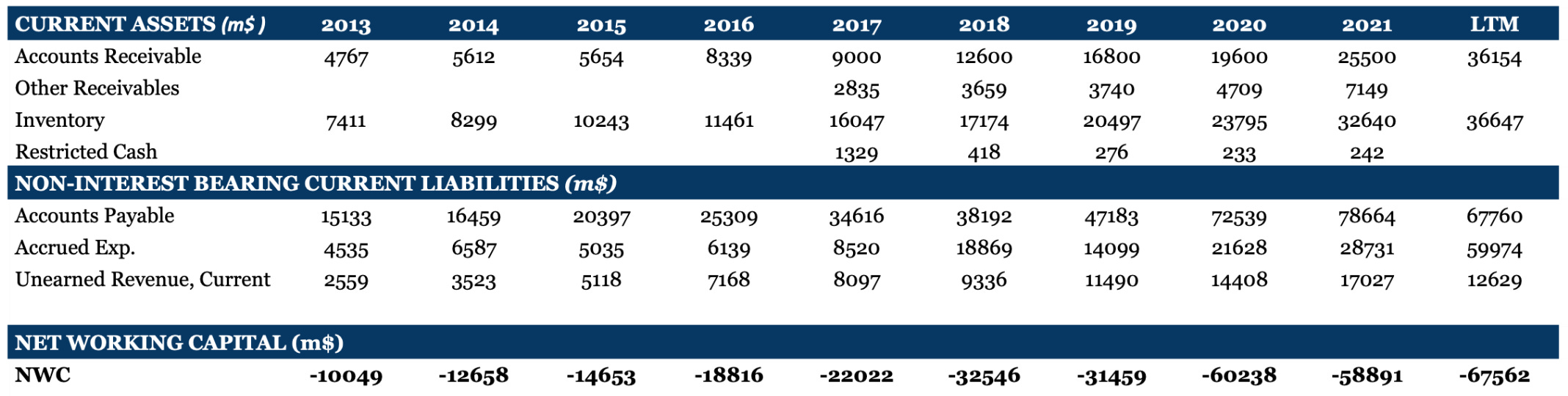

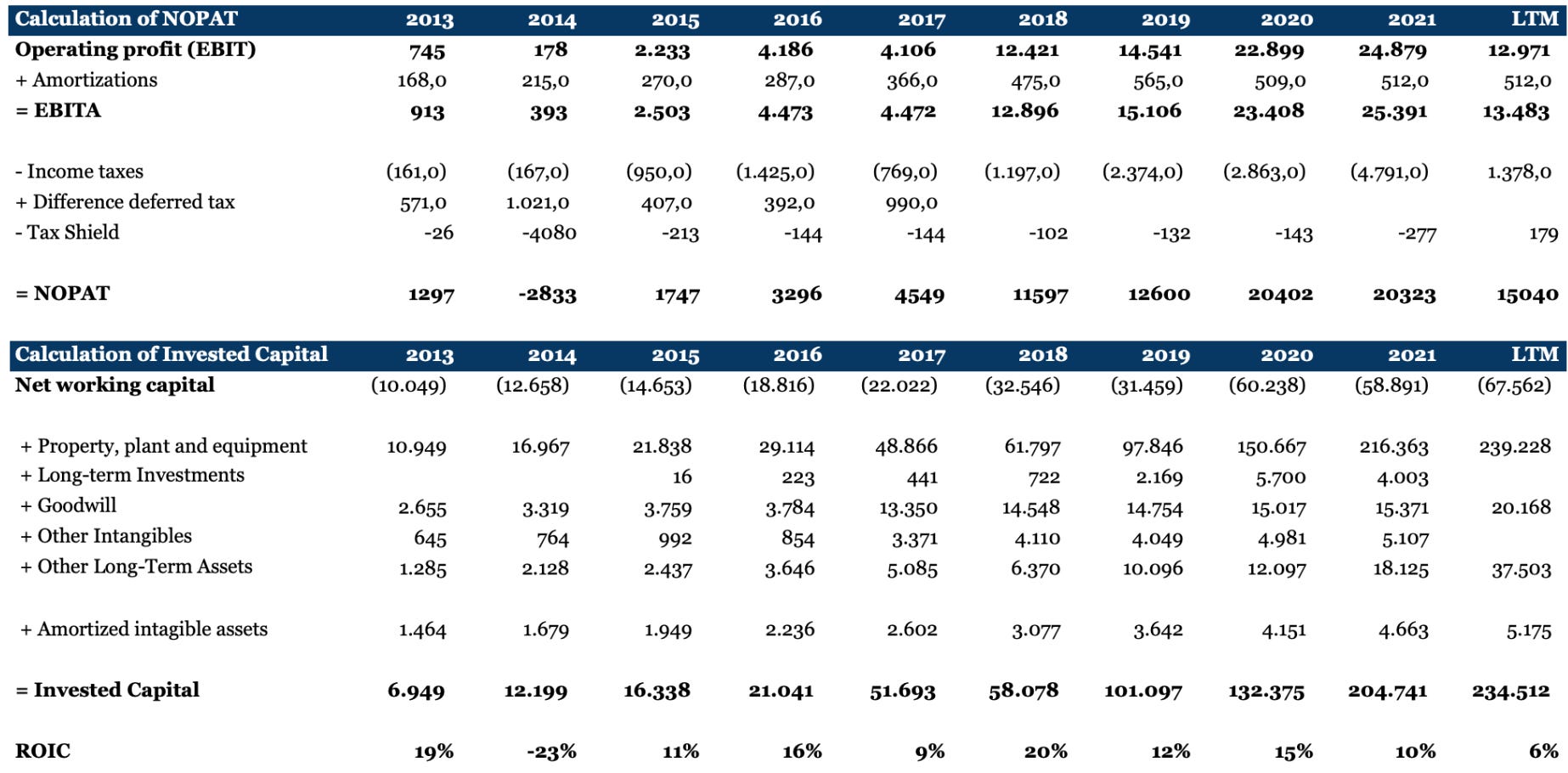

This huge negative working capital makes the capital tied up by Amazon relatively low, offering some decent and considerable returns on invested capital.

We won't say that Amazon is a business with high returns on capital because it is not. But ROIC is not the only metric that indicates value creation. The value of Amazon lies in its capacity for an unusually high reinvestment rate.

Building high walls

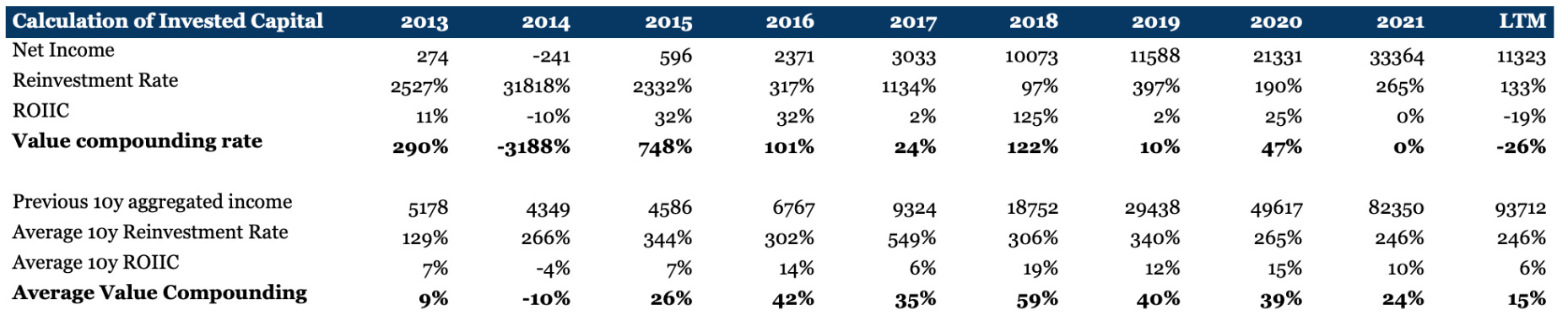

What has always differentiated Amazon is its capacity for innovation and reinvestment. Theoretically, a company can generate value for its shareholders by reinvesting its profits at returns on capital that are higher than its cost of capital. So basically there are two levers. Either increase returns on invested capital or reinvest a lot of capital with a lower return (although always above the cost of capital). Few people put a value on this, but the reinvestment capacity that Amazon has demonstrated over the last 25 years has been, simply and strikingly, spectacular.

How many companies do we know of that have been able to consistently reinvest much, much, much more than their profits at those ROIIC rates?

This causes fearful markets to constantly doubt the company's ability to generate value, especially when we see something like this:

It's really scary! But it seems the markets have forgotten Amazon's history and value creation model. It is quite clear that there have been overcapacity errors in both CAPEX and OPEX (acknowledged by management), coupled with general macro headwinds and other impacts. However, as investors, we tend to tear our hair out claiming that we want managers who invest heavily in down cycles to come out stronger in the recovery. But when it happens, most cringe.

Amazon has invested $66b in CAPEX in the last 12 months. The same as Microsoft ($24b), Apple ($11b), and Google ($31b) combined. Not a guarantee of anything, of course. But it is a declaration of intent.

To be or not to be

We cannot look at all companies and business models with the same eyes. We must avoid dogmatism and look for exceptional companies. Apple is a company that sells products, and increasingly services, with incredible returns on capital. And yet, CAPEX is ridiculous for its volume. Moreover, it uses a large part of its FCF in share buybacks, "independently" of the price, something that we generally criticize. Despite this, the company has managed to generate lots of value. By this, we mean that we should not be dogmatic. Not all companies can be analyzed in the same way.

Amazon has had negative FCF for two years now, but this is not the first time. If we look at it with perspective, we will see that Amazon has generated an aggregated 61b of FCF in 25 years, yet its market value is over 1T. Actually, during the 3 years between 2018 and 2020, it generated 64b, meaning the aggregated other 22 years it has burnt cash. But that is its model: achieving scale no matter what.

There was a time when the market didn't understand it. They looked at the PE ratio and did not get how a company with such a large amount of assets could trade at those multiples. But then came the FCF "explosion" in the 2018-2020 period and the market saw it clearly. If Amazon ever would reduce its growth CAPEX, the company would be capable of generating massive amounts of FCF!

That narrative no longer applies in the current investment cycle, and the share price has been severely impacted. But Amazon keeps growing and reinvesting. Getting even more scale and eventually, increasing the operating cash flows.

Today is day one

Nothing has changed. Bezos’ first letter to shareholders is a piece to be kept in a museum of how a clear strategy shall lead company operations for good.

We believe that a fundamental measure of our success will be the shareholder value we create over the long term

We will continue to focus relentlessly on our customers.

We will share our strategic thought processes with you when we make bold choices

(to the extent competitive pressures allow), so that you may evaluate for yourselves

whether we are making rational long-term leadership investments.

We will work hard to spend wisely and maintain our lean culture. We understand the

importance of continually reinforcing a cost-conscious culture, particularly in a

business incurring net losses.

We will continue to focus on hiring and retaining versatile and talented employees,

and continue to weight their compensation to stock options rather than cash. We know our success will be largely affected by our ability to attract and retain a motivated employee base, each of whom must think like, and therefore must actually be, an owner.

Almost 25 years later, Amazon has not only been able to revolutionize the way we buy and generate new wealth for different stakeholders, but they also have kept innovating and shifting the company towards new business models.

A picture we believe exemplifies Amazon’s innovation culture is how they gradually turned all of its major costs into sources of revenue:

We don't know what lies ahead. But so long as the culture of innovation and entrepreneurship remains present in its obsession to satisfy the customer, reinvesting everything and more, today will still be day one.

If you enjoyed this piece, please give it a like and share!

Thanks for reading Edelweiss Capital Research! Subscribe for free to receive new posts and support our work.

If you want to stay in touch with more frequent economic/investing-related content, give us a follow on Twitter @Edelweiss_Cap. We are happy to receive suggestions on how we can improve our work.

Great take, very interesting, thank you! Complementary AWS expectations I just saw: https://twitter.com/Quartr_App/status/1587132626103635972