#18 Siren call: share repurchases

#18 Siren call: share repurchases

CEOs always refer to these programs as giving money back to shareholders. But what if it comes at a high cost?

Last week JPMorgan “temporarily” suspended share buybacks arguing they needed to quickly meet higher capital requirements and “allow them maximum flexibility to best serve customers, clients and community through a broad range of economic environments” (Levitt, 2022). This decision happened after the stock price fell 33% in the last year.

Does anyone check the returns on buyback programs? Maybe we should.

In this article we will analyze how most share buyback programs destroy value. How these programs go hand to hand with economic cycles and, many times, are driven by unaligned management incentives. Finally, we will assess the convenience of these programs to assess better capital allocation skills. In the end, their decisions will eventually be the drivers for the company's performance in the long term.

Welcome to Edelweiss Capital Research! If you are new here, join us to receive investment analyses in 10 slides, economic pills, and investing frameworks by subscribing below:

Investors love buyback programs. Most prefer them blindly to dividends. “They are giving money back to shareholders without the tax burden”. Sounds good, but is this right?

Investors assume that buybacks automatically add value. But surprise, most of the time it is not the case. The key question before embracing these programs is whether companies truly believe they are paying less than intrinsic value for the stock and adding value for the remaining shareholders? If not, maybe they should be spending less on buybacks and paying out more in dividends (dividends should always be the last option. Never stop compounding).

Therefore, if most share repurchases destroy value (believe me for some paragraphs, I will demonstrate you later) and companies “miss” this cash from their balance, why do they do it? Always seek the incentives.

The main driver behind many share buyback programs (Zion et al,2012) may simply be an attempt by companies to offset the earnings per share dilution from their stock based compensation plans. But there is still economic dilution!

Some companies may take it a step further and use buybacks to try and drive EPS growth by reducing the share count. Many times management bonuses come associated with this metric, but just because something is accretive to earnings doesn’t necessarily mean that it’s creating value for shareholders!

Buybacks are also viewed as a more flexible way to return capital to shareholders than dividends especially if there is “excess cash” since buybacks can more easily be adjusted up or down and some shareholders are addicted to dividends and won’t allow a temporary cancellation.

Or finally, in some extraordinary cases, management just might think that the market has undervalued its stock and a buyback is simply a good investment compared to the other uses of capital. Only this, and nothing more, is a good reason for a share buyback program. Let’s see why.

Value-creating share buybacks are simple math

Let's start from a basic assumption, and at the same time, a reckless one. The CEO of a company knows, or should know, better than anyone the intrinsic value of the company he leads. Let's think about it, he knows better than anyone what is the strategy in the upcoming years, he should be able to predict better than anyone what the financial results will be in the future and what are the possibilities to get there. Then he may or may not be wrong, but he clearly has an edge over any investor, just because he has more quality information.

At this point, and if this were true, making capital allocation decisions would be simply math. Let's see it with a simple example.

Let’s say my company Metavision has $500 in cash, and the present value of my future cash flows are $2000. Who else better than me (the CEO) to have a fair value of the expected cash flows? Since we have 250 shares outstanding, my intrinsic value per share is $10.

We can repurchase our shares under three scenarios: the stock is undervalued, overvalued or at fair value. If the company were to use all of its $500 in cash to buy back shares you can see how the intrinsic value per share would be affected under each scenario all else equal. Not all company share repurchases create value.

Now the company faces the capital allocation decision in a simpler and rational way. Here below 3 different scenarios. (Bear in mind that later capital allocation decisions are not that easy and there are infinite scenarios to consider. However, the framework to make decisions SHOULD be the same).

If allocation of capital is simple and logical, why is capital so poorly allocated? If management stands to gain wisdom and credibility by facing mistakes, why do annual reports trumpet only success? The answer, according to Buffett, is the unseen force called the institutional imperative—the lemming-like tendency of corporate management to imitate the behavior of other managers, no matter how silly or irrational it may be. Thinking independently and charting a course based on rationality and logic are more likely to maximize the profits of the company than a strategy that can best be described as ''follow the leader" (Hagstrom, 2000).

The advantage we have as investors facing a buyback program is that we can, according to our subjective valuations, determine whether the program will create value or not. It is comparably way easier than with CAPEX allocation or with minor private acquisitions. So it is our duty to scrutinize these programs and act accordingly.

The crude reality of the share buyback programs

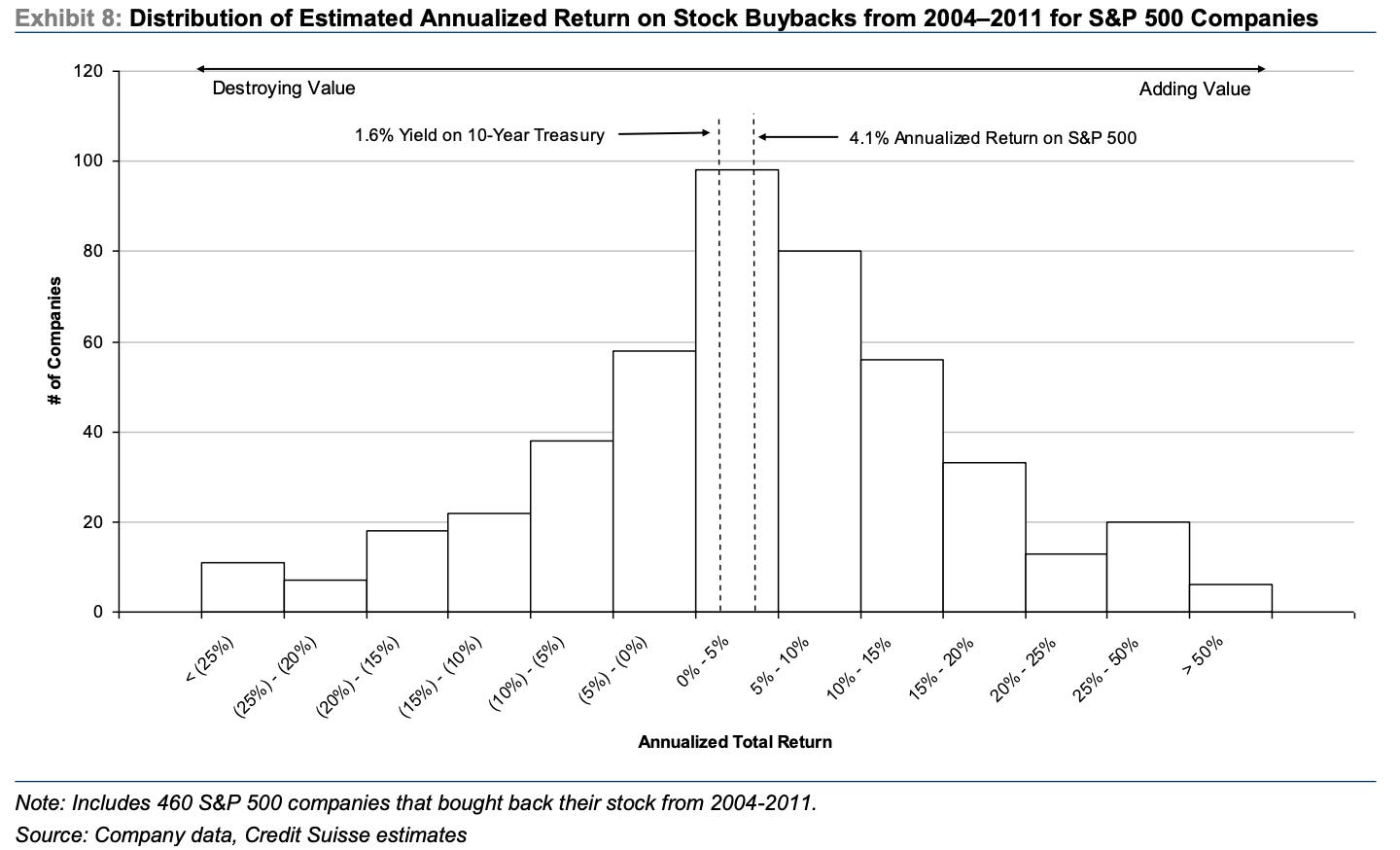

Mauboussin (2006) and Zion et al. (2012) did an extraordinary job a decade ago analysing the returns of the buyback programs. You can find the link to both reports below in the references.

Their study shows that out of the 500 companies in the SP500, only 180 (36%) beat the benchmark against a cost of equity of 7%. Results are even worse if we try to find companies whose share buybacks returned more than a 15% annualized. Only 70 achieved it. As a result it looks like most of the buybacks for the S&P 500 between 2004 and 2011 did destroy value for the shareholders.

The problem for many companies was bad timing. It appeared share buybacks ramped up when things were going well and stock prices were higher (when companies have “excess cash” and there’s more dilution from stock based compensation), and are dialed down when times were tough and stock prices were lower. Does it sound familiar? Of course, that’s the exact opposite of what companies should be doing.

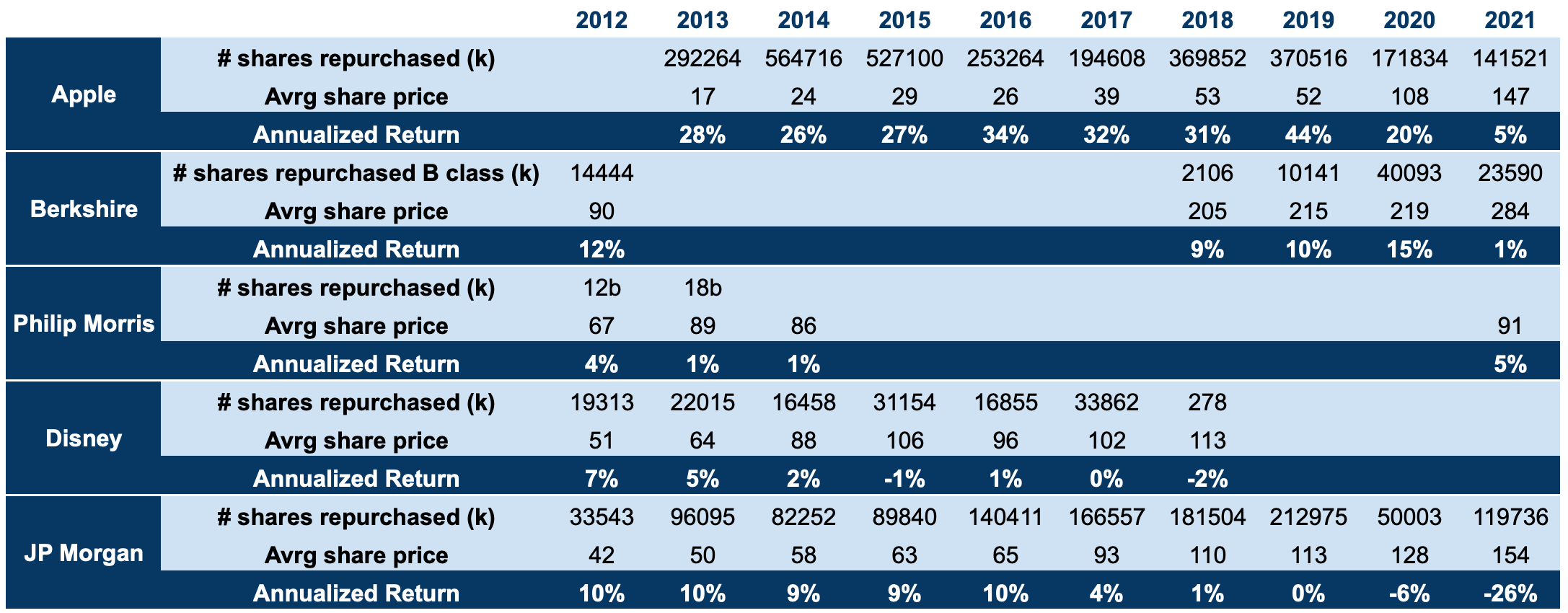

What has happened in the last decade? Have the companies learned the lesson? I am afraid to say it doesn’t seem to. I have analyzed the returns of each share buyback program from 2012 to 2021 of some well known and quality companies.

Apple: the share buyback king. Apple has run the largest program ever and the results have been… awesome. I have always been concerned and reluctant with Apple buying back shares “so expensive”. Furthermore, Apple repurchase program in 2012 had the primary objective of neutralizing the impact of dilution. What a red flag for poor capital allocation. However, and up to this day, I have always been mistaken.

Berkshire Hathaway: if anyone should know about intrinsic value, this one is Warren Buffett. He has always been deliberately cautious about these kinds of programs. And we can see here why. Results so far have not been exceptional. At least if we look at their repurchases in 2012. Buffett decided to buy back Berkshire shares again in 2018. I think it is fair to say it is too soon still to achieve conclusions on the results.

Philip Morris: one of the dividend kings ran also some programs some years ago. I am happy to see that they gave up and focused on dividends given the results.

Disney: a quality company with a big brand moat missed to allocate capital efficiently.

JP Morgan: their “temporarily” suspension of share buybacks comes after years of big programs at higher share prices. If last year they thought their share price was undervalued and spent so much money in buybacks, how come this year with the price -30% they are not allocating a single penny on them?

Past doesn't repeat but rhymes. Share buyback programs, similar to any investment, need time to see the results. In these cases, past actions can tell us what we can expect in the future.

The golden rule

Capital allocation is the main duty of any CEO. If allocation is poorly done and returns are below our opportunity costs, value is being destroyed.

Rebel capital allocators know (in a range) what is the intrinsic value of their companies and act consequently. Bruce Flatt has expressed in his letters what is his fair value of Brookfield. Mark Leonard has never said it but because he is incentivised to keep the share price in line with the fair value so all the employees buying the stock in the open market do it at the fair price. Buffett has repeated several times their criteria for repurchases: anytime Berkshire is below 1,2x book value.

Terry Smith (2020) is also very prudent and cautious in regards to share buybacks. Among others, he proposed the following: a) Management should be required to justify share buybacks by reference to the price paid and the implied return and compare this with alternative uses for the cash. b) Investors and commentators should analyze share buybacks on exactly the same basis as they would if the company bought shares in another company; c) Share buybacks need to be viewed with more than average skepticism when done by companies whose management are incentivised by growth in EPS.

Never forget: in repurchase decisions, price is all-important. Value is destroyed when purchases are made above intrinsic value.

A company should repurchase its shares only when its stock is trading below its expected value and when no better investment opportunities are available.

If you enjoyed this piece, please give it a like and share!

Thanks for reading Edelweiss Capital Research! Subscribe for free to receive new posts and support our work.

If you want to stay in touch with more frequent economic/investing-related content, give us a follow on Twitter @Edelweiss_Cap. We are happy to receive suggestions on how we can improve our work.

References

Levitt, H. (2022). JPMorgan Halts Share Buybacks as Earnings Miss Estimates. Bloomberg 14 July. Link to article

Hagstrom, R. (2000). The Warren Buffett Portfolio: Mastering the Power of the Focus Investment Strategy. Wiley.

Mauboussin, J. (2006). Clear Thinking about Share Repurchase. Legg Mason Capital Management. Link to report

Sloan, J. (2022). Apple Buybacks Show How Tim Cook's Buyback Policy Differs From Warren Buffett's. Seeking Alpha 5 March. Link to article

Smith, T. (2020). Investing for Growth: How to make money by only buying the best companies in the world – An anthology of investment writing, 2010–20. Harriman House.

Zion, D., Varshney, A. , Burnap, N. (2012). Stock Buybacks: Adding Value or Destroying Value? Credit Suisse. Equity Research. Link to report