The Swedish serial acquirer dilemma

The Swedish serial acquirer dilemma

Goodwill vs Intangibles: implications in the short & long term

Serial acquirers consistently captivate the attention of investors, and when these firms are Swedish, their allure only intensifies due to the impressive track records many such companies have established in this Nordic nation. Recently, an interview with a former CFO of Teqnion has surfaced, delving into a range of pivotal issues that are critical for any investor to consider. Today we discuss about the accounting practices that underpin the operations of some of these companies and its consequences.

Welcome to Edelweiss Capital Research! If you are new here, join us to receive investment analyses, economic pills, and investing frameworks by subscribing below:

In today's financial world, where the dynamics of corporate acquisitions are scrutinized, the story of Teqnion, a Swedish company that has captured the attention of both retail investors and prominent figures in the industry, emerges as a fascinating case study. This discussion stems from a recent interview with a former CFO of Teqnion, published on InPractise, which sheds light on the challenges and strategies followed by many of the new serial acquirers.

Teqnion is a Swedish company that operates primarily in the industrial sector, specializing in the acquisition and management of companies that manufacture and distribute a variety of industrial and technological products. Their portfolio includes businesses ranging from heavy machinery manufacturers to electronic component suppliers.

Teqnion is not just another company in the market; its appeal has been magnified due to the interest and investment by Christopher Mayer, author of the book "100 Baggers" and recently elected as a current board member. Mayer, whose investments signify a potential for long-term growth, sees in Teqnion the ability to multiply its value many times over. This perception has been one of the reasons why the company has become a focal point for investors looking for the next big stock market success.

Moreover, Teqnion's performance has been notably positive, having achieved a 4.5x return in its 5 years as a public company, which adds a layer of legitimacy to its promise as a future investment. However, not everything in the company is stable; Teqnion has seen considerable turnover in its CFO position, having four different CFOs in a few years. Currently, the company has decided not to immediately fill this position, instead opting to develop a junior member of the team to eventually take on the role.

With this situation introduced, let's move on to the key points of the interview.

Interview Insights on Swedish Serial Acquirers

I want to thank Adria for providing me with the interview that inspired this article. I highly recommend their newsletter (Spanish only) for more valuable insights: Turtle Capital by Adrià Rivero

The interview revolves around how the small Swedish acquires are accounting for their acquisitions. Some notes:

Junior vs matured serial acquires intangible accounting

Former CFO at Teqnion: When your business model revolves around acquiring numerous companies to turn a profit, you can't afford to invest a lot of time and money on consultants, lawyers, and so forth. It's particularly important for junior serial acquirers to have an efficient process and not overspend on advisors. Also, the companies they acquire often don't have IFRS to start with. It's common that the acquired company doesn't have a competent accountant who can answer IFRS-related questions. So, it's partly due to the time aspect and, of course, a certain degree of laziness. Why do extra work when you can allocate everything to goodwill? No one has raised an issue before. But when they start to consider a more diligent PPA, they realize that it can significantly impact earnings. If they allocate 50% of the value to customer agreements, for instance, they have to write it down over eight to 10 years, which directly affects earnings. I also think that auditors don't push for a proper PPA as much as they should, but this is likely to change given the current economic climate.

Companies like Lifco, Lagercrantz, and Bergman & Beving tend to allocate 50% to intangibles and 50% to goodwill. If you look at it over time, as I did a few years ago, it seems more like a fixed model rather than an individual assessment. That's my impression. It appears that the percentage they allocate to customer relations remains relatively fixed over the years. It seems more like a standardized model rather than a completely individual assessment for each company.

Q: However, allocating everything to goodwill could result in higher taxes, as you're not amortizing your assets and therefore end up paying a higher tax rate?

Former CFO at Teqnion: I'm not entirely sure how it impacts taxes, so I'd rather not comment on that

It is quite surprising to hear this response from a CFO, or from anyone who has given even minimal thought to their business model or how to create long-term value.

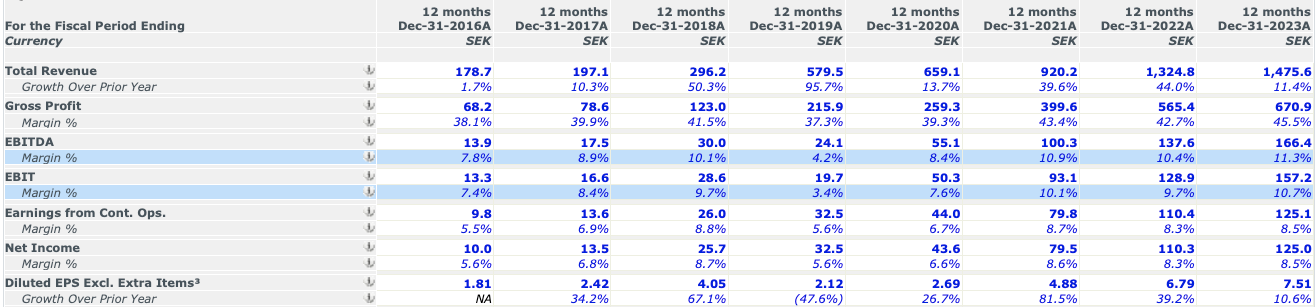

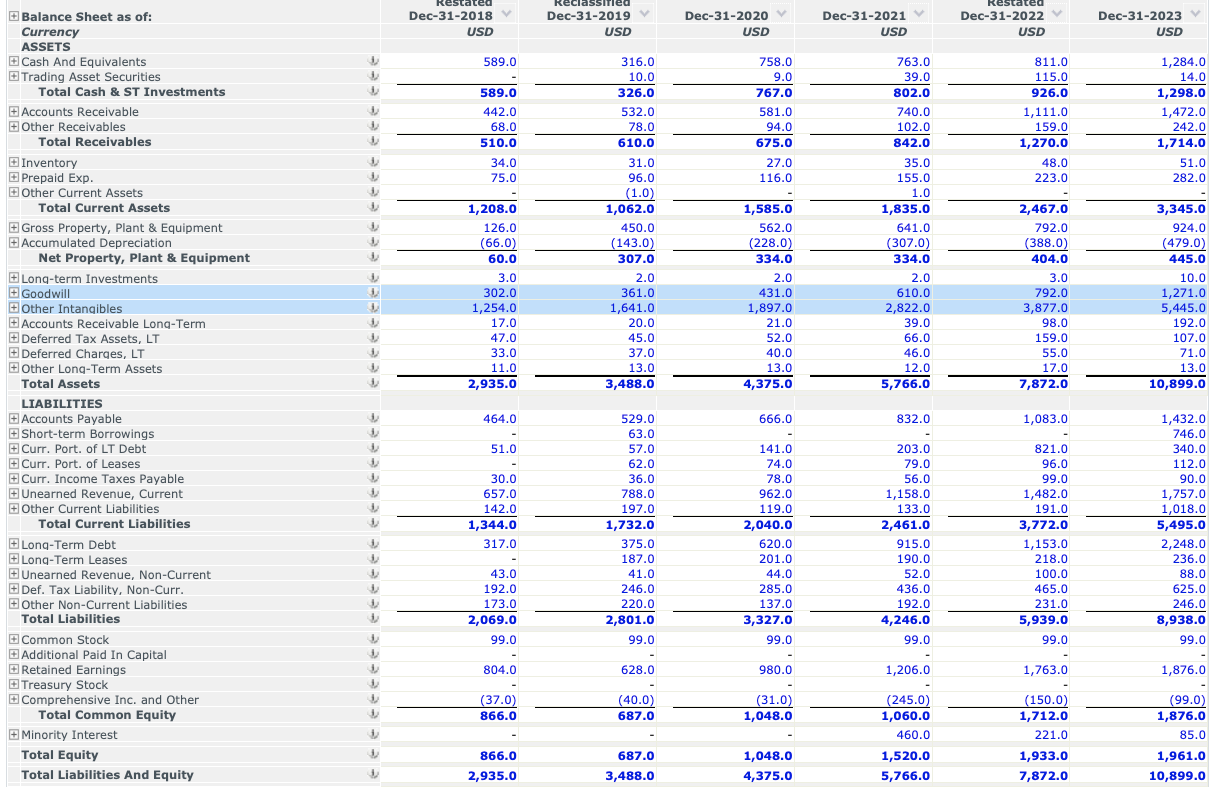

However, let's see how this holds true by looking at the balance sheets of Teqnion and Lifco:

What implications does this have? Lifco can amortize those intangibles over the years, reducing its short-term accounting profit, but also its taxable base. However, this has a positive impact on cash generation as it results in lower tax payments (and amortization as such is a non-cash expense).

Then, Teqnion's income statement might look better, but Lifco's reduces tax payments and therefore improves cash generation.

Auditors & goodwill

Q: When you acquire a small business, what exactly does the auditor ask for when you assign everything to goodwill?

Former CFO at Teqnion: In my experience with these types of companies and other acquisitions, you typically provide the auditor with a net present value model. You present the estimated cash flow for the company, and with your assumptions for the discount rate, WACC and so on, you arrive at a valuation. You can then demonstrate that it's more than 20% plus or minus the goodwill you have booked.

Q: How rigorous is this process? How closely do auditors examine this?

Former CFO at Teqnion: Generally, my experience is that the dialogue tends to focus more on your WACC and similar assumptions, rather than the operational forecast and its realism. However, during good economic years, this hasn't been much of a challenge as everything has been going well.

Impairment test & auditors

Q: If you buy a business for two million euros, for example, and it's worth one million euros, you have one million of goodwill. If the economy declines, you do your DCF again with the declining revenue and the value is now one million, you then have to mark down goodwill?

Former CFO at Teqnion: Just because there are one or two years of a tougher economy, it's not always necessary to do a write-down. You should have a robust model and be able to do some risk testing. For example, what happens if the interest rate goes up by a certain percentage? You need to play around with some assumptions and ensure that the value is not just the same as the goodwill. You need to have quite a margin, I think around 20%. Auditors typically look at how it was the previous year. If you've changed a lot of assumptions to avoid a write-down, they will probably notice. They often go back to the previous year and ask, "How did you present this at that time? What has changed? If you're close to it, why don't you want to write it down? What's your argument?"

Q: In that situation, what could a company argue as to why they're not going to write it down?

Former CFO at Teqnion: Regarding your forecast for this particular company, maybe they have recently acquired a new customer. Based on my experience, auditors tend to give the company quite a bit of flexibility in terms of operational arguments. However, this does not apply to how you calculate the WACC.

Our view on this topic is quite critical overall, to the point of being a real embarrassment what many auditors and companies do regarding goodwill impairment tests, but we have already discussed this previously here:

However, the crux of the matter is that many companies have relative discretion to convince auditors to allocate more or less goodwill or intangibles when formalizing an acquisition. Therefore, it is up to the management's discretion to assign these intangibles to the category they deem appropriate.

This reminds me of a tweet I read a while ago that has somehow disappeared. It went something like this:

From the outside looking in, it sure looks like KPMG lets $CSU.TO disproportionately write-up its definite life Intangible Assets using DCF soulmath to avoid allocating more of the Purchase Consideration to Goodwill.

The accounting strategy of predominantly allocating to goodwill rather than tangible assets may improve a company's profit and loss (P&L) and earnings per share (EPS) in the short term. This practice, while artificially boosting reported earnings, can result in higher tax burdens due to the lack of amortization of these intangible assets. Conversely, a greater allocation towards intangibles allows for their amortization over time, reducing annual taxable profit. It’s crucial to reiterate that the problem is not inherently in how acquisitions are accounted for. Ultimately, it's all about the capital invested in the business and the cash returns it generates.

The choice of how to distribute the purchase price between goodwill and intangibles is not only a technical accounting decision—it has tangible effects on a company's cash flows due to different tax treatments. Amortizing intangibles decreases the taxable base, potentially offering long-term fiscal benefits, despite perhaps initially adversely affecting reported earnings.

Yet, it is observed that many investors, particularly in retail, focus predominantly on P&L and EPS metrics, often overlooking the integral health of the balance sheet. Firms like Constellation Software (CSU) have adeptly managed to allocate a substantial part of their intangibles to amortizable assets, which prioritizes the long-term robustness of their financials over the fleeting cosmetic enhancement of profit statements. It's commonplace in investor circles to hear assertions like "a company with 20% margins is superior to one with 10%," indicating a widespread neglect for the balance sheet’s significance, which is equally critical as the P&L.

In our M&A article series (articles #42 #43 #44,we've delved into the complexities of creating value through acquisitions, frequently stymied by the information asymmetry between the buying and selling parties. Generally, sellers are not inclined to significantly undervalue their enterprises. Many investors are drawn to the notion of multiple arbitrage—where a firm trading at 20x EBITDA acquires another at 10x EBITDA, and the market subsequently re-evaluates the acquired EBITDA at 20x, ostensibly creating immediate value. Advocates of this strategy argue that it brings diversification and thereby adds more value by consolidating a group of companies.

Nonetheless, I advocate for investments in companies that inherently create value through their acquisitions, whether it be through direct financial returns—combining the acquisition yield with prospective organic business growth and the enduring intrinsic quality (and terminal value) — or via strategic gains such as access to new distribution channels or substantive cost reductions. Ideally, all these advantages should be clearly reflected in the company’s financial statements, independent of how the market whimsically assigns a 20 to 30 times profit valuation to industrial and cyclical firms with substantial capital needs.

If you enjoyed this piece, please give it a like and share!

Thanks for reading Edelweiss Capital Research! Subscribe for free to receive new posts and support our work.

If you want to stay in touch with more frequent economic/investing-related content, give us a follow on Twitter @Edelweiss_Cap. We are happy to receive suggestions on how we can improve our work.

Great article! Haven’t read this interview, so this insight was rather new. Really odd to see these frequent changes in their CFO position, hopefully they’re able to find someone soon that works with the duo of Daniel and Johan harmoniously and sustainably…

Thank you for sharing!

Edel with the Sunday Special ... thank you! TEQ is a very interesting case ... .